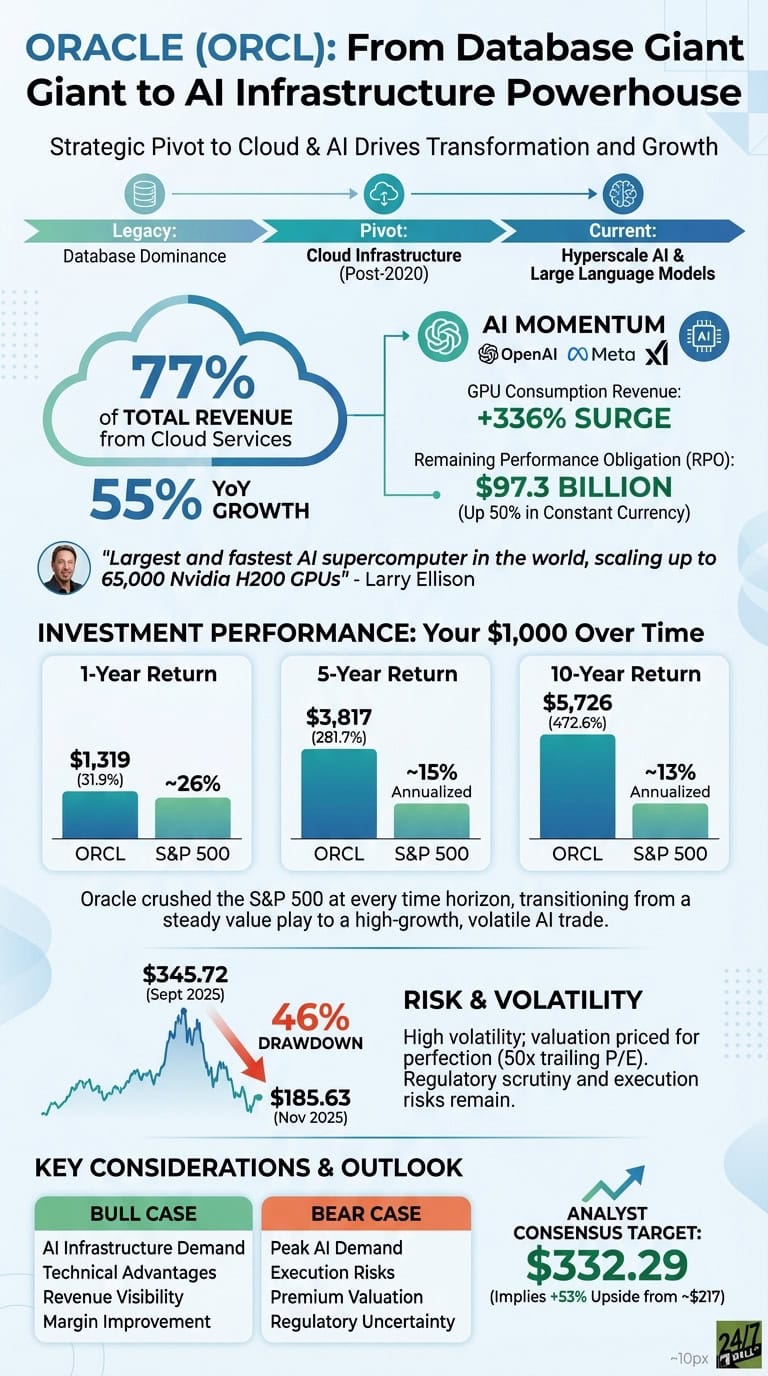

Oracle Corporation (NYSE: ORCL | ORCL Price Prediction) spent two decades as a database giant before pivoting hard into cloud infrastructure. That shift accelerated dramatically after 2020, when hyperscale AI workloads became the company’s defining growth engine. Oracle built modular data centers, signed partnerships with OpenAI and Meta, and positioned itself as the fastest, cheapest option for training large language models. The strategy worked. Cloud services now represent 77% of total revenue and grew 55% year-over-year in the most recent quarter.

The company’s remaining performance obligation hit $97.3 billion in Q2 FY2025, up 50% in constant currency. CEO Safra Catz noted that “our cloud RPO grew nearly 80% and now represents nearly three-fourths of total RPO.” Oracle’s GPU consumption revenue surged 336% as demand from AI customers outstripped supply. Chairman Larry Ellison emphasized the company’s technical edge: “We just extended our AI performance advantage by delivering the largest and fastest AI supercomputer in the world, scaling up to 65,000 Nvidia H200 GPUs.”

The stock reflected this transformation. Oracle went from a steady, dividend-paying value play to a volatile AI trade with extreme price swings in 2025.

Your $1,000 Became $5,726 Over a Decade

1-Year Return

- Initial Investment: $1,000

- Current Value: $1,319

- Total Return: 31.9%

- S&P 500 (same period): Approximately 26%

5-Year Return

- Initial Investment: $1,000

- Current Value: $3,817

- Total Return: 281.7%

- Annualized Return: 30.7%

- S&P 500 (same period): Approximately 15% annualized

10-Year Return

- Initial Investment: $1,000

- Current Value: $5,726

- Total Return: 472.6%

- Annualized Return: 19.0%

- S&P 500 (same period): Approximately 13% annualized

Oracle crushed the S&P 500 at every time horizon, but the ride required conviction. The stock hit $345.72 in September 2025 before collapsing to $185.63 two months later, a 46% drawdown. Timing mattered enormously. Investors who bought at the peak are down 37% despite strong fundamentals.

Returns were driven by Oracle’s cloud transformation and AI positioning. Revenue growth accelerated from mid-single digits to double digits as cloud infrastructure took over. Management expects cloud revenue to reach $25 billion this fiscal year, up from near zero a decade ago.

Key Investment Considerations

Investors considering Oracle should evaluate whether AI infrastructure spending will stay elevated for the next three to five years. The company has real technical advantages in network speed and modular deployment. Major customers like OpenAI, Meta, and xAI validate the product. The $97.3 billion RPO provides revenue visibility, and margins are improving with scale. Analysts have a consensus target of $332.29, implying 53% upside from current levels around $217.

Potential risks include the possibility that AI infrastructure demand has peaked or that Oracle’s execution could slip. The stock trades at 50x trailing earnings and 42x forward earnings, pricing in perfection. Three of the last four quarters missed earnings estimates. The recent 46% drawdown shows how quickly sentiment can turn. Regulatory scrutiny around data center power contracts adds uncertainty.

The bull case centers on patient investors willing to ride volatility. The cloud migration is still early, and Oracle’s unique multi-cloud partnerships give it optionality competitors lack. However, the stock carries significant risk given premium valuations and the need for sustained AI infrastructure demand.

Contact [email protected] for any questions or corrections.