Marvell Technology (NASDAQ:MRVL | MRVL Price Prediction) and Micron Technology (NASDAQ:MU) both just delivered AI-fueled earnings reports, yet they sit on opposite sides of the data center stack.

Marvell sells the custom silicon and optics that stitch AI clusters together. Micron sells the memory those clusters cannot run without. Their latest results show how AI spending is rewarding very different business models.

Custom Silicon Carries Marvell. HBM Carries Micron.

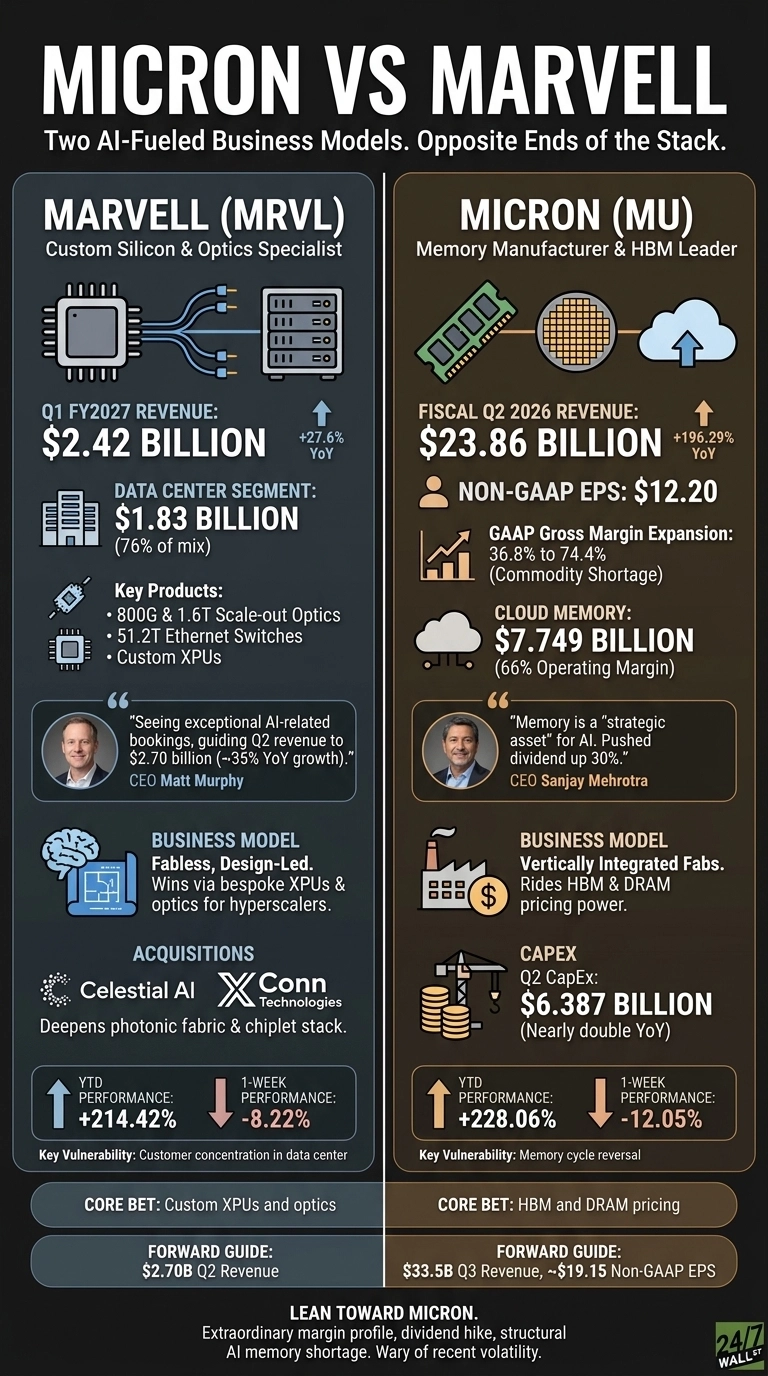

Marvell posted Q1 FY2027 revenue of $2.42 billion, up 27.6% year over year, with the Data Center segment hitting $1.83 billion, roughly 76% of the mix.

That number tells you everything: this is a data center company now, powered by 800G and 1.6T scale-out optics, 51.2T Ethernet switches, and custom XPU programs. CEO Matt Murphy framed the moment plainly, saying Marvell is seeing “exceptional AI-related bookings” and guided Q2 revenue to $2.70 billion at the midpoint, roughly 35% YoY growth.

Micron’s fiscal Q2 2026 was a different animal. Revenue jumped to $23.86 billion, up 196.29%, and non-GAAP EPS landed at $12.20. GAAP gross margin expanded to 74.4% from 36.8% a year earlier, which is the kind of move you only see when a commodity flips into shortage.

Cloud Memory alone delivered $7.749 billion at a 66% operating margin. CEO Sanjay Mehrotra called memory a “strategic asset” and pushed the dividend up 30%.

Designer of Bespoke Chips vs. Manufacturer of a Scarce Commodity

Marvell is fabless and design-led. It wins by being the chosen partner for hyperscalers building bespoke XPUs, and it just closed Celestial AI and XConn Technologies to deepen its photonic fabric and chiplet stack.

Micron owns fabs, runs heavy capex, and rides DRAM and HBM pricing. CapEx hit $6.387 billion in the quarter, nearly double a year ago.

| Lens | Marvell | Micron |

| Core Bet | Custom XPUs and optics | HBM and DRAM pricing |

| Model | Fabless, design wins | Vertically integrated fabs |

| Key Vulnerability | Customer concentration in data center | Memory cycle reversal |

| Forward Guide | $2.70B Q2 revenue | $33.5B Q3 revenue |

The market is not exactly relaxed about either name. MRVL fell 8.22% over the past week, and MU dropped 12.05%. Both still sit far above where they began the year, with MU up 228.06% YTD and MRVL up 214.42%.

What Decides the Next Leg

For Marvell, I want to see custom XPU ramps actually convert design wins into recurring shipments, and I want optics to stay ahead of in-house hyperscaler programs. The June 17 custom AI investor event should sharpen that picture.

For Micron, the next test is whether HBM pricing holds as SK Hynix and Samsung add capacity. The Q3 guide of $19.15 non-GAAP EPS at 81% gross margin sets a high bar. Keep an eye on the stock around that report.

Why I Lean Toward Micron, With Eyes Open

If I had to pick one today, I would lean Micron. The margin profile is extraordinary, the dividend hike signals real conviction, and AI memory shortage looks structural through fiscal 2026. That said, I am wary. Reddit traders are already “fading” vol on MU with condors, and the stock just sold off hard from a $1,064 peak.

Marvell is the better fit if you prefer a narrower, design-driven AI bet and can stomach customer concentration risk. I would wait for one more clean quarter from each before sizing up.

Contact [email protected] for any questions or corrections.