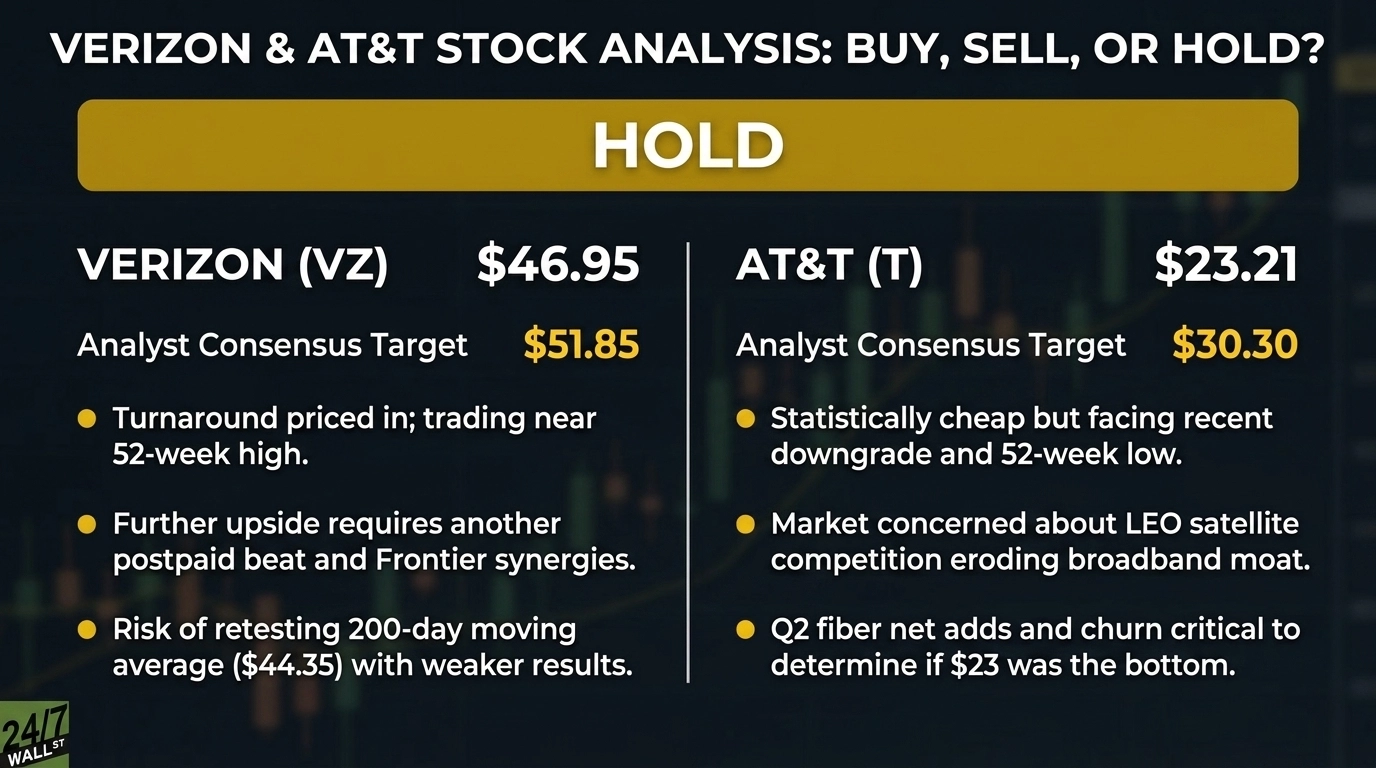

At $46.95 for Verizon (NYSE:VZ | VZ Price Prediction) and $23.21 for AT&T (NYSE:T), both telecom giants screen as range-bound. VZ sits just below its $50.91 52-week high, while T actually trades closer to its $22.32 52-week low after a recent downgrade.

Both companies are mid-execution on aggressive fiber rollouts. Verizon closed its Frontier deal in January 2026 and now serves approximately 16.8 million broadband connections under new CEO Dan Schulman.

AT&T closed its Lumen Mass Markets fiber acquisition in February 2026, lifting its footprint to over 37 million fiber locations with a target of 60 million by 2030. Same playbook, very different stock reactions.

The Bull Case: Convergence Is Working

Verizon raised 2026 adjusted EPS guidance to $4.95 to $4.99 and posted its first positive Q1 postpaid phone net additions since 2013. Free cash flow guidance of $21.5 billion or more funds a $3.0 billion buyback and the dividend.

AT&T trades at a forward multiple of 10x against guided EPS of $2.25 to $2.35 with a double-digit three-year CAGR. Management is targeting $45 billion in shareholder returns through 2028 and an $8 billion repurchase in 2026 alone. Advanced home internet revenue jumped 27.3%.

The Bear Case: Debt, Downgrades, and Soft Performance

Verizon carries $172.5 billion in total debt post-Frontier, with interest expense up 18.9% YoY. Postpaid ARPA slipped 1.9% and churn ticked to 0.97%.

AT&T was just downgraded by Oppenheimer from Outperform to Perform on low-earth-orbit satellite competition concerns, with the stock hitting a fresh 52-week low. Net leverage is expected to peak near 3.2x post-EchoStar, and legacy revenues are guided to fall 20%+ in 2026.

The Case for Patience

Verizon’s turnaround is real but already priced. AT&T’s discount is real but the downgrade narrative needs to clear. Investors collecting Verizon’s 6.08% yield and AT&T’s 4.93% yield are paid to wait for the next two earnings reports to resolve the divergence.

What the Data Shows

Verizon is up 19.07% year to date against an analyst target of $51.85 from 25 covering analysts (3 Strong Buy, 8 Buy, 14 Hold, 0 Sell), implying roughly 10% upside on a trailing P/E of 11x.

AT&T is down 4.48% YTD, trades at a trailing P/E of 7x, and carries an analyst target of $30.30 (3 Strong Buy, 12 Buy, 10 Hold, 0 Sell) for implied upside near 31%. For context, the S&P 500 is up roughly 7% year to date, so Verizon is meaningfully ahead of the index while AT&T is trailing it. Analyst targets are one input among many.

The Verdict: Hold Both Until the Next Earnings Report

At $46.95 for Verizon and $23.21 for AT&T, both stocks look range-bound. Here is why.

Verizon has done the work, but at 11x earnings near a 52-week high, the easy money from the Schulman turnaround narrative is already in the price. The path to $55 runs through another postpaid beat and visible Frontier synergies. Anything less and the stock retests the 200-day at $44.35.

AT&T looks statistically cheap, but the Oppenheimer downgrade and fresh 52-week low signal the market wants proof that LEO satellite migration is not eroding the broadband moat. Q2 fiber net adds and churn will decide whether $23 was the bottom or a waypoint.

Shareholders are paid handsomely to wait through one more quarter before reassessing positioning at these prices.

Contact [email protected] for any questions or corrections.