At $16.67, SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) screens as compelling at current levels. Shares have shed roughly 38.89% over the past six months as a hawkish Federal Reserve under Kevin Warsh punished high-beta fintech, and the market is now pricing a 30%-growth digital bank like a stressed subprime lender.

SoFi runs a one-stop digital banking platform with 13.7 million members and $40.24 billion in deposits that fund over 90% of liabilities. The slide from a 52-week high of $32.73 reflects rate fears, a large Technology Platform client departure, and modest credit normalization. The operating story remains intact.

A 30% Growth Story Marked Down to Distressed

Q1 2026 delivered $1.10 billion in revenue, beating consensus, and GAAP net income surged 134% YoY to $166.73 million on record $12.18 billion in loan originations. Management guided FY2026 to roughly $4.655 billion in adjusted revenue, $1.6 billion in EBITDA, and $0.60 in adjusted EPS.

At a 27x forward multiple against medium-term adjusted EPS growth of 38% to 42%, the PEG sits below 1. CEO Anthony Noto agrees the price is wrong: he made open-market purchases of 15,878 shares at $15.73 and 15,545 shares at $16.00 in May.

The Hawkish Fed and Credit Crack Risk

Bears point to Technology Platform revenue declining 27% YoY, a 63 basis point compression in average asset yields, and rising charge-offs: personal loans hit 3.03%, student loans 0.65%. With beta at 2.15, a prolonged Warsh tightening cycle could pressure shares further.

Multiple executives sold in mid-March at $17.43 to $17.76, and r/options sentiment turned firmly bearish into June, dominated by a “SOFI Bear Call Credit Spread” thread. A credit-cycle break would invalidate the cheap-growth call quickly.

Why Patience Has Real Costs Here

The hold case argues for waiting for charge-offs to stabilize and the Fed pivot to clarify. The cost of waiting is that the high-margin Financial Services segment grew 41% YoY and 43% of new products came from existing members. Cross-sell economics this strong tend to re-rate violently once macro fear lifts.

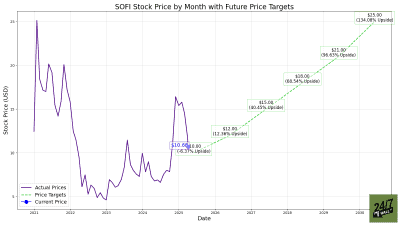

The Data Says Idiosyncratic Mispricing

Shares currently trade at $16.67 against a Wall Street consensus target of $21, implying roughly 26% upside, though that target represents a single consensus data point. Of 24 covering analysts, 8 rate it Buy or Strong Buy, 12 Hold, and 4 Sell or Strong Sell.

Year-to-date, SOFI is down 36.33% while the S&P 500 is up 8.19%, a roughly 45-point gap. Forward P/E sits at 27x, price-to-book at 2x, against ROE trending toward the mid-teens at guided 2026 profitability.

The Verdict: A Capitulation Setup

At $16.67, the setup for SoFi looks compelling on the data.

The path to appreciation runs through 2026 execution. If management hits the $0.60 adjusted EPS guide and Tech Platform stabilizes against easy comps in 2H26, the stock should re-rate toward 30x forward earnings on a $0.85 to $0.90 2027 print, putting fair value north of $25.

The entry at $16 implies the market is pricing in a credit-cycle break that quarterly data does not yet support. The CEO is buying with personal capital at this price. The thesis breaks if personal loan charge-offs push above 4% or guidance gets cut materially. Until then, this is a 30%-growth platform with a tier-one deposit base trading like a stressed regional bank.

Short-sighted retail capitulation into a hawkish Fed has created the rare chance to own a profitable, scaling fintech at a single-digit growth multiple.

Contact [email protected] for any questions or corrections.