SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) minted its own stablecoin on a public blockchain and signed Mastercard to settle it globally. Yet shares are down 40.07% year to date and trading at $15.69.

The Q1 earnings report showed $12.18 billion in loan originations, up 68% year over year, and management is guiding to $4.655 billion in adjusted net revenue for 2026. Can this stock realistically print $50 by 2030?

The Real Reason SoFi Is Down 40% This Year

The selloff stems from two things investors hate: multiple compression and a credit scare. Technology Platform revenue fell 27% year over year after a large client departed, and personal loan annualized charge-offs ticked up sequentially from 2.80% to 3.03%.

Student loan charge-offs rose to 0.65% from 0.47%. Add a beta of 2.126 to a rate-sensitive lender and you get violent moves. Shares are down 19.54% over the past month even though they bounced 2.48% last week. The stock sits 36% below its 52-week high of $32.73. The market is punishing noise and ignoring the signal.

Wall Street Sees 34% Upside. Our Model Says More.

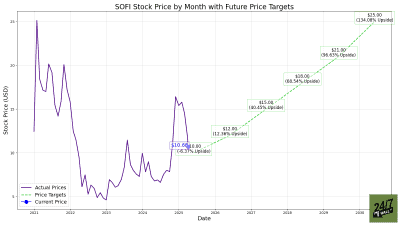

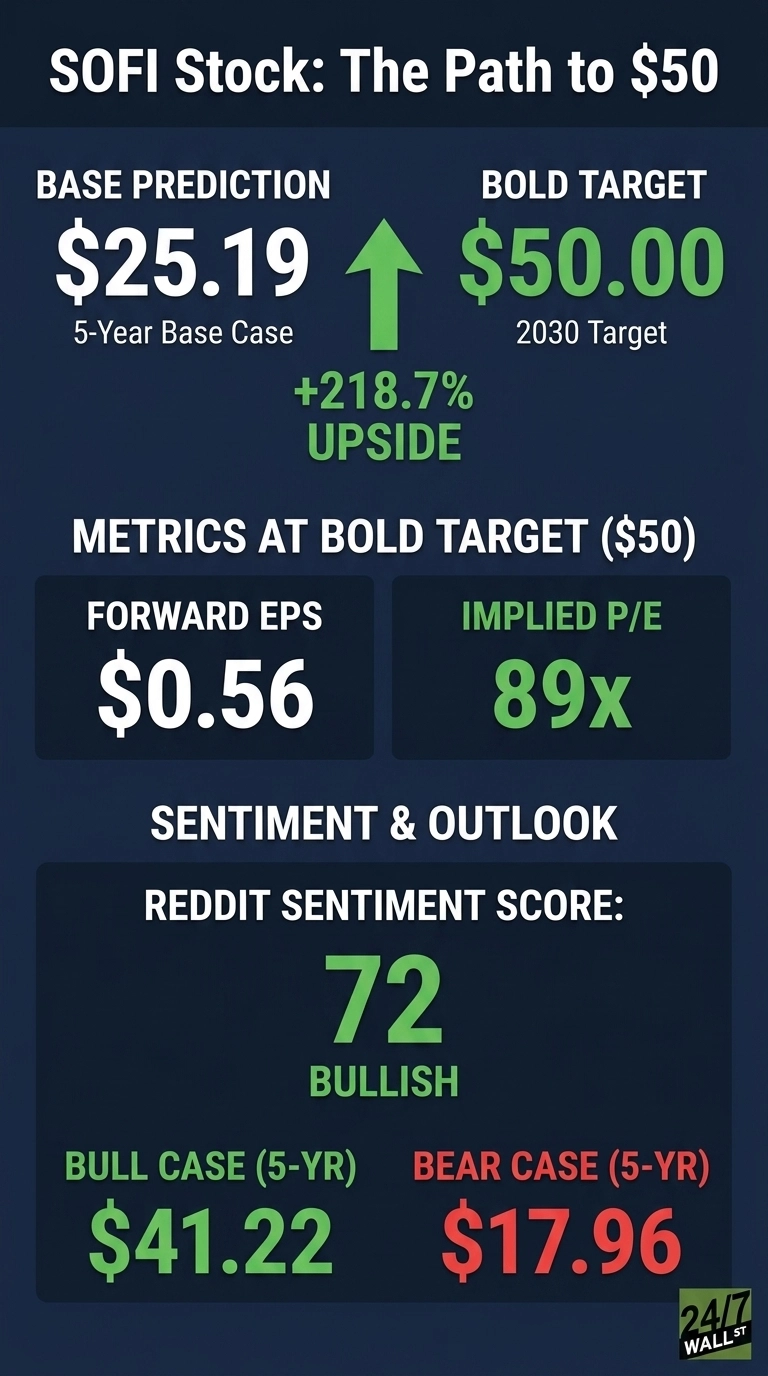

The consensus is lukewarm. 3 strong buys, 5 buys, 12 holds, 2 sells, and 2 strong sells, with an average target of $21.10. Our base case predicted price is $25.19 with a high confidence score of 90%, with a conservative case of $17.96 and an optimistic 2030 target of $41.22.

Analysts appear anchored to recent credit results. Only 33% are bullish, yet management is guiding to a 38% to 42% adjusted EPS CAGR through 2028. That gap between sentiment and earnings power is where 5-year winners get made.

The Path to $50 Per Share

Reaching $50 from today’s price of $15.69 would require a gain of 218.7%. With forward EPS of $0.56, a price of $50 implies a forward P/E of 89x. Our base case of $25.19 already implies 36x means the bold target requires 54x of additional multiple expansion on today’s earnings.

That sounds extreme until you compound the EPS line. At the midpoint of management’s 38% to 42% adjusted EPS CAGR off a 2026 base of $0.60, EPS lands near $2.30 by 2030. On that number, $50 is roughly 22x forward, in line with growth fintech peers.

The catalysts are real: SoFiUSD stablecoin minting with Mastercard settlement, Big Business Banking launched in April 2026, and $3.6 billion in new Loan Platform commitments across three partners including a top-five private asset manager.

Anthony Noto put it simply: “Our strategic entry into new areas like digital assets alongside the strong growth in our existing businesses are strengthening and diversifying our platform.” The primary risk is a recession that spikes charge-offs and forces SoFi to shrink the loan book.

Where SoFi Trades Today vs Its Earnings Power

At $15.69 against forward EPS of $0.56, shares trade at 28x forward, which is rich on absolute terms but cheap against a 40%-plus EPS growth profile (PEG well below 1).

Shares sit between a 52-week low of $12.74 and high of $32.73, and the 10-year return of 49.71% badly understates how the bank has transformed. If EPS compounds in the high 30s, today’s price looks like a gift in five years.

Can SoFi Really Hit $50? My Verdict

$50 by 2030 requires a 218.7% gain. It is a stretch goal that sits well above my base case. My base case is closer to the model’s $25.19.

To reach $50, three things need to break right: EPS compounds at the high end of guidance toward $2.00-plus; SoFiUSD and Big Business Banking scale into real revenue lines; and credit behaves as the cycle turns. A deep consumer credit downturn derails it. We’ve outlined the blueprint for how SoFi Technologies could reach $50 in 2030.

Contact [email protected] for any questions or corrections.