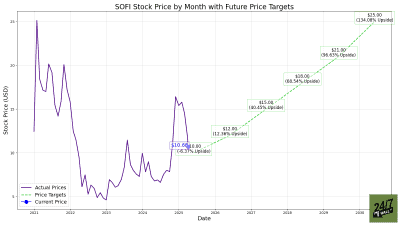

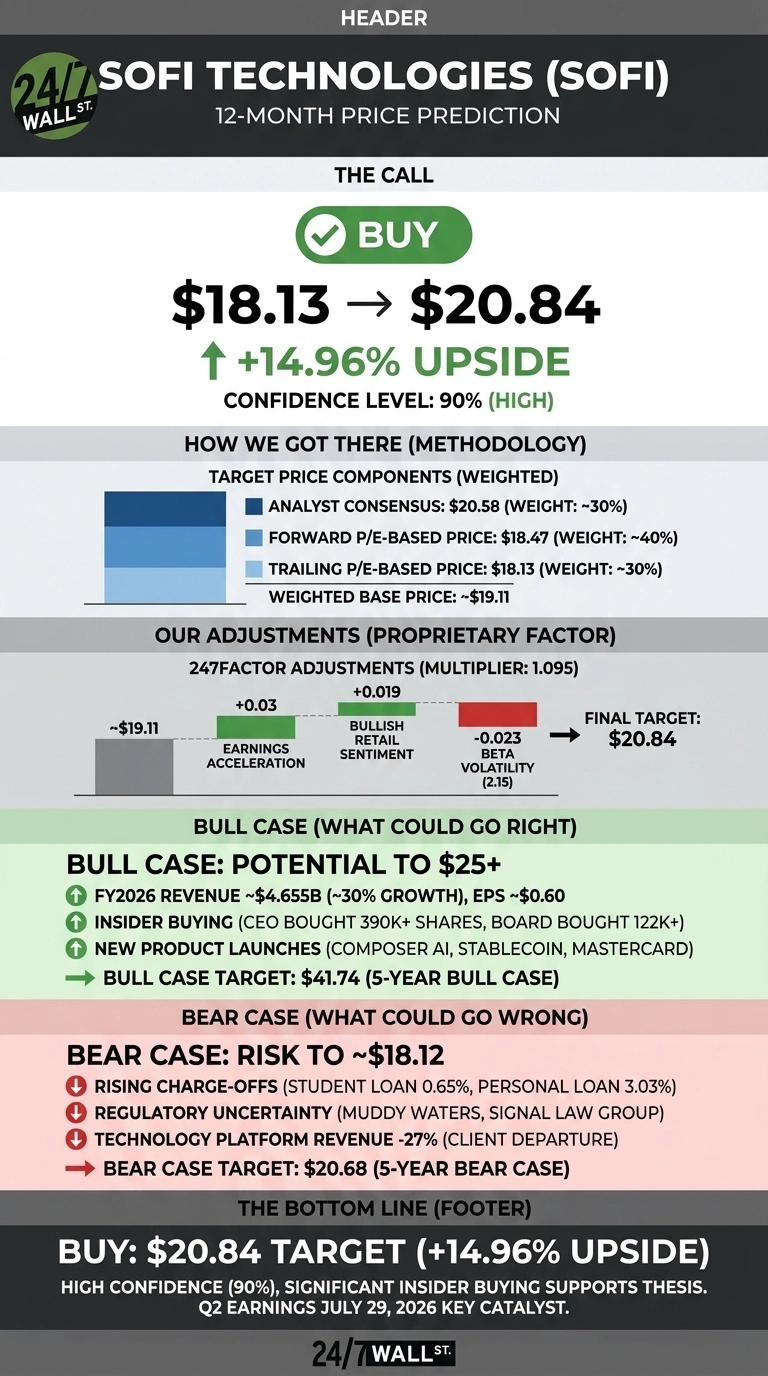

SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) has been one of the loudest post-election casualties in fintech. Shares closed at $18.13 on July 13, 2026, down 30.75% year to date from the December 31 close of $26.18. Our 24/7 Wall St. price target for SoFi is $20.84, implying 14.96% upside over the next twelve months. The recommendation is buy, with confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $18.13 |

| 24/7 Wall St. Price Target | $20.84 |

| Upside | 14.96% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $28 to $18: What Actually Broke

The stock topped out near $28.03 in October 2025, cratered to $15.61 in May 2026, and has clawed back 9.35% over the past month. The 52-week range is $14.92 to $32.73.

Q1 2026 delivered record loan originations of $12.18 billion, up 68% YoY, revenue of $1.10 billion, and net income of $166.73 million, up 134% YoY. The selloff stemmed from Muddy Waters accounting allegations from March 2026, a 27% Technology Platform revenue decline from a client departure, and rising personal loan charge-offs at 3.03%. CEO Anthony Noto said, “We had an excellent Q1 delivering another quarter of durable growth and strong returns.”

The Case for $25+

Management guided FY2026 adjusted net revenue to $4.655 billion (~30% growth), adjusted EBITDA of $1.6 billion at a 34% margin, and adjusted EPS of $0.60. The plan calls for adjusted EPS CAGR of 38% to 42% through 2028.

Product launches are stacking fast: Composer AI investing platform, small business loans up to $250,000, the SoFiUSD stablecoin, and Mastercard settlement rails. Cathie Wood’s ARK has been adding, and a TIKR mid-case model values the stock at $48 by December 2030.

Insider buying signals conviction: the CEO acquired 390,874 shares during the drawdown, and the board bought a coordinated 122,238 shares on June 9, 2026.

What Could Go Wrong

The bear case runs to $18.12 over twelve months, essentially flat. Credit is the pressure point. Student loan charge-offs rose to 0.65% from 0.47%, and personal loan charge-offs climbed to 3.03% from 2.80% sequentially. NIM compressed 63 basis points.

The Technology Platform segment’s 27% revenue decline reflects a large client departure, with $3.6 billion in new Loan Platform Business commitments replacing the lost volume.

Regulatory overhang from the Muddy Waters allegations and a Signal Law Group VRS bulletin is real. Analyst consensus remains a “Hold” across 25 analysts, and beta at 2.15 means macro shocks hurt disproportionately.

How SoFi Stacks Up Against Robinhood and Ally

Robinhood (NASDAQ:HOOD) is the direct fintech growth comp. Robinhood carries a market cap of roughly $86.9 billion against FY2025 EPS of $2.05, trading at a far richer multiple than SoFi’s forward P/E of 31. Q1 2026 revenue missed by 6.07% at Robinhood as crypto revenue collapsed 47%. SoFi’s 4.87% revenue beat and diversified engine look underpriced.

Ally Financial (NYSE:ALLY) is the incumbent digital bank comparison. Ally posted Q1 2026 adjusted EPS of $1.11, beating consensus by 17.93%, and pays a $0.30 quarterly dividend, but its top line contracted 38.7% YoY after the credit card divestiture. SoFi is compounding revenue at 30%+ while Ally is optimizing. Against this peer set, our $20.84 target looks reasonable to conservative.

The Buy-the-Dip Setup, With Guardrails

The 24/7 Wall St. price target is $20.84, the call is buy, and confidence is 90%. What tips the scale is the insider tape: the CEO, CFO, CTO, and six directors bought together while the stock was in the $15 to $17 range.

For readers thinking about fintech inside a broader AI-driven portfolio, our 7 Stocks Powering the AI Boom research frames the sector’s setup.

The setup strengthens if credit metrics stabilize at Q2 earnings on July 29, 2026. The thesis weakens if personal loan charge-offs push above 3.25% or the Muddy Waters allegations escalate.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $20.84 |

| 2027 | $23.50 |

| 2028 | $26.10 |

| 2029 | $28.60 |

| 2030 | $28.60 base / $41.74 bull |

These projections assume SoFi hits its 30%+ revenue CAGR and 38% to 42% EPS CAGR through 2028. Meaningful upside or downside could come from stablecoin adoption, credit cycle turns, or the Q2 earnings report on July 29.

Contact [email protected] for any questions or corrections.