Headlines are once again celebrating Uber (NYSE:UBER | UBER Price Prediction) for its 50 million Uber One members and a robotaxi roadmap CEO Dara Khosrowshahi calls “a clear path to becoming the largest facilitator of AV trips in the world.”

The underlying numbers tell a more complicated story.

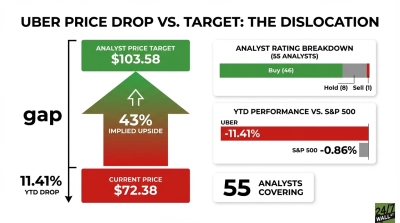

The Hot Trade Is Quietly Cracking

Uber’s Q1 2026 numbers, filed May 6, 2026, look strong on a slide. Underneath, the structure is fraying. Revenue of $13.203 billion missed the $13.263 billion consensus, and GAAP net income collapsed to $263 million from $1.78 billion a year earlier, gutted by a $1.5 billion pre-tax headwind on equity investment revaluations. That is the second consecutive quarter of multi-billion-dollar revaluation noise, with FY25 EPS landing at $2.45 versus a $5.37 estimate.

Meanwhile, long-term debt has climbed to $10.52 billion, insurance reserves swelled from $2.75 billion to $3.39 billion, the Freight segment is still unprofitable, and management is committing $100 million-plus to AV charging infrastructure into the teeth of a crowded autonomous arms race. Reddit captured the mood when a wallstreetbets post titled “Why Uber’s latest earnings report was a major red flag for the state of the consumer” drew 609 upvotes, while sentiment scores have sat at 28 to 38 through June 13. The stock is down 19.59% over the past year. This is a saturated Western platform, throwing capital at low-margin moonshots, with a multiple no longer protected by macro tailwinds.

The Redirect: A Profitable Super-App On Sale

Grab Holdings (NASDAQ:GRAB) is the dominant Southeast Asian super-app, and it is trading near its 52-week low of $3.18 with a market cap of just $13.08 billion, roughly one-tenth of Uber’s. Three factors stand out when comparing the two platforms.

1. Profitable inflection, accelerating growth. Grab delivered its first full year of net profit in FY25 at $200 million, then opened Q1 2026 with revenue of $955 million, up 23.5% YoY, beating consensus by 3.78%. Net income jumped 400% YoY to $120 million, Adjusted EBITDA expanded 46% to $154 million, and management reiterated FY26 Adjusted EBITDA guidance of $700 million to $720 million, growth of 40% to 44%. That is a different trajectory than Uber’s GAAP whiplash.

2. A fortress balance sheet funding capital returns. Grab is sitting on $2.95 billion in cash against that $13 billion cap, with a $500 million buyback authorized in February 2026 and a $250 million ASR plus $150 million contingent forward already executed. Grab is executing buybacks from a net-cash position while its digital banking arm holds $1.6 billion in GXS and GXBank customer deposits.

3. An uncrowded, dominant footprint. Mobility grew 19%, Deliveries 23%, and Financial Services 43%, with the loan portfolio up 130% YoY to $1.438 billion. A foodpanda Taiwan acquisition closes in H2 2026, the inaugural Singapore-Johor cross-border ride-hail licence opens a new corridor, and there is no AV capex arms race weighing on the model. CEO Anthony Tan summed it up: “Our On-Demand GMV growth accelerated to 24% year-over-year… marking another quarter of record profitability.”

Wall Street’s 27 buy or strong buy ratings, zero sells, and a $5.97 target point to substantial upside from $3.30. The setup is straightforward: a high-growth Southeast Asian platform trading near a 52-week low against a Western incumbent wrestling with revaluation noise and AV capex.

For investors watching platform economics, Grab presents a different profile than Uber: profitable inflection, net-cash balance sheet, and a less crowded competitive footprint worth monitoring into the second half of 2026.