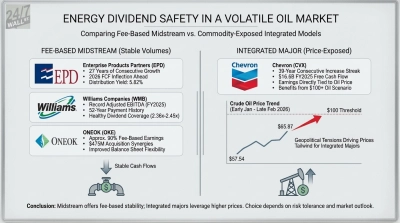

The midstream MLP space rarely makes headlines, but a fractured global energy supply chain has turned Enterprise Products Partners (NYSE:EPD | EPD Price Prediction) into a magnet for income capital. Units are up 21.79% year to date, outpacing the S&P 500’s 6.38%, as Strait of Hormuz disruptions push international buyers toward U.S. NGL, LPG, and ethane logistics. The question for retirees: is the distribution safe?

Distribution Snapshot

| Metric | Value |

|---|---|

| Annualized Distribution | $2.20 |

| Yield | 5.79% |

| Consecutive Years of Growth | 27 |

| Most Recent Increase | 2.8% (April 2026) |

| Aristocrat/King Status | Shadow King (MLP, not S&P member) |

The Payout Math Has a Wrinkle Worth Understanding

Enterprise paid $4.678 billion in distributions in 2025 against $8.585 billion in operating cash flow and $2.965 billion in free cash flow. FY 2025 EPS of $2.66 against a $2.18 calendar distribution puts the earnings payout near 82%, normal for an MLP given heavy depreciation add-backs.

| Metric | Value | Assessment |

|---|---|---|

| Earnings Payout | ~82% | Normal for MLP |

| FCF Payout (FY25) | 0.63x cover | Elevated (growth capex) |

| OCF Coverage | 1.83x | Strong |

| DCF Coverage (Q2 25) | 1.6x | Healthy |

The FCF gap reflects a $5.3 billion growth project backlog, not distribution stress. 2026 growth capex drops to $2.3 to $2.6 billion from $4.5 billion, the FCF inflection management has telegraphed.

Debt Is Heavy but Well-Termed

| Metric | Value |

|---|---|

| Total Debt | $34.2B |

| EBITDA (TTM) | $9.79B |

| Net Debt/EBITDA | ~3.5x (manageable for IG midstream) |

| Beta | 0.469 |

27 Years, No Cuts, and Buybacks on Top

| Year | Annual Distribution |

|---|---|

| 2026 (run rate) | $2.20 |

| 2025 | $2.17 |

| 2024 | $2.09 |

| 2023 | $1.99 |

| 2022 | $1.89 |

The streak held through 2020 at $0.445 quarterly. Co-CEO AJ Teague also bought 2,665 units at $37.55 in March 2026.

Management Is Pointing at the Cash Inflection

Co-CEO Jim Teague on the Q1 2026 call: “Our DCF for the quarter supported a 2.8 percent increase in our cash distribution rate to common unitholders and allowed us to retain $1.5 billion of DCF to reinvest… and fund $116 million of buybacks.” On the macro setup: “As a result of the recent disruption of exports from the Middle East, we are seeing strong demand for the security and reliability of U.S. energy exports.”

Verdict: Very Safe

Dividend Safety Rating: Very Safe. DCF coverage of 1.6x, OCF coverage of 1.83x, a 27-year streak, and a winding-down capex cycle give me high confidence in the payout. The bull case for Enterprise rests on record 1.9 MMBPD fractionation volumes and growing LPG export demand. The key risk is NGL prices collapsing below $0.50/gallon and forcing marketing margin compression deeper than 2026 guidance assumes. For retirees, this is one of the cleanest 5.79% yields in the energy complex.

Contact [email protected] for any questions or corrections.