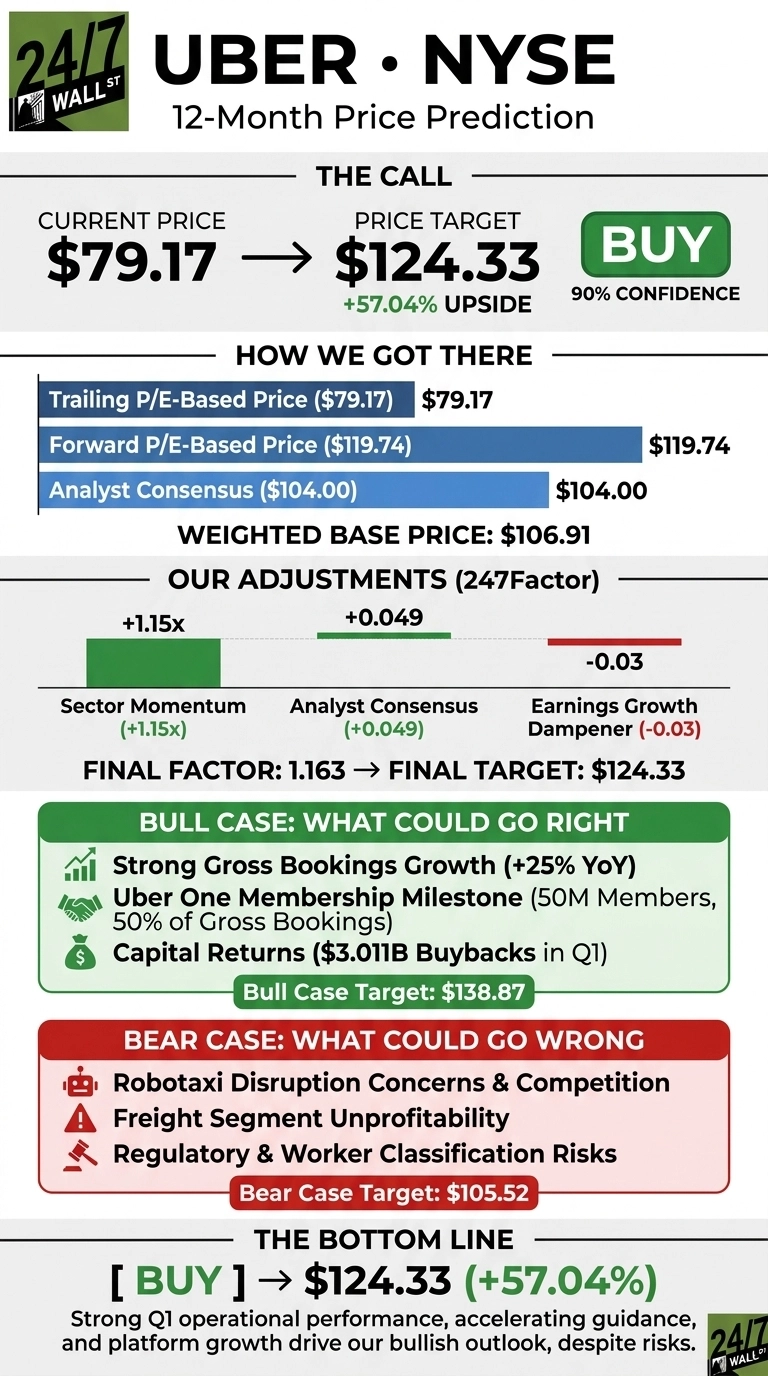

Uber (NYSE:UBER | UBER Price Prediction) just delivered a quarter that crystallizes the bull thesis. The company reported Gross Bookings of $53.72 billion, up 25% YoY, and guided Q2 well above consensus. The stock jumped 8.53% on the earnings report to $79.17, but our model says the move is far from over.

Our 24/7 Wall St. price target for Uber is $124.33, implying 57.04% upside over the next 12 months. We rate Uber a buy with 90% confidence, the high end of our framework.

| Metric | Value |

|---|---|

| Current Price | $79.17 |

| 24/7 Wall St. Price Target | $124.33 |

| Upside | 57.04% |

| Recommendation | BUY |

| Confidence | 90% |

A Guidance Beat That Rewrites the Setup

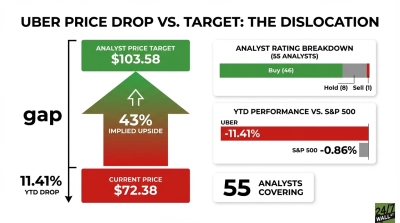

Uber is up 6.31% over the past week and 9.7% over the past month, though still down 7.76% over the past year and 3.11% YTD. Shares trade 2% below the 52-week high of $101.99, having bounced off the $68.46 low.

Q1 EPS came in at $0.72 versus $0.71 expected, with revenue of $13.20 billion narrowly missing estimates. The standout was Q2 guidance: Non-GAAP EPS of $0.78 to $0.82, growth of 31% to 38% YoY, and Adjusted EBITDA of $2.7 to $2.8 billion. Delivery revenue grew 34% YoY, and Uber One hit 50 million members, driving half of Gross Bookings.

The Case for $138 and Higher

Operating income surged 56.6% YoY to $1.92 billion, free cash flow hit $2.286 billion, and Uber repurchased $3.011 billion of stock in the quarter alone. CEO Dara Khosrowshahi framed the platform thesis directly: “Reaching 50 million Uber One members is an exciting milestone as we execute against our platform strategy, with members now driving half of our Gross Bookings across Mobility and Delivery.”

Wall Street is aligned: 10 Strong Buy and 36 Buy ratings against just 1 Sell, with a consensus target of $104. Our bull-case path projects $138.87 by May 2027, a 75% return, if AV monetization accelerates and Uber One compounds. Goldman Sachs lowered the firm’s price target on Uber to $115 from $125 and keeps a Buy rating on the shares while Piper Sandler analyst Thomas Champion raised the firm’s price target on Uber to $105 from $100 and keeps an Overweight rating on the shares.

What Could Go Wrong

The bear case starts with robotaxi disruption. GAAP net income fell 85.19% YoY to $263 million, though bulls would correctly note this reflects a $1.50 billion pre-tax equity revaluation headwind tied to accounting while operations held up. Non-GAAP EPS still grew 44% YoY.

Other risks: the Freight segment remains unprofitable, Beta of 1.158 implies above-market volatility, and worker classification rulings remain a wild card. Our bear-case path lands at $105.52, still 33% above today.

Where the Risk/Reward Sits

Our price target of $124.33 with 90% confidence reflects a rare alignment: accelerating bookings, expanding margins, an aggressive buyback, and a forward P/E that still looks reasonable for a platform compounder. The setup looks constructive if Uber sustains 20%+ Gross Bookings growth and converts AV partnerships into revenue. The thesis weakens if regulators reclassify drivers in a major market or AV competitors bypass the platform entirely. On balance, the risk/reward skews favorable at current levels.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $124.33 |

| 2027 | $155 |

| 2028 | $190 |

| 2029 | $230 |

| 2030 | $272.21 |

These projections assume Uber compounds Gross Bookings in the high teens and converts AV partnerships into a profitable third leg. Significant upside or downside could result from robotaxi economics or driver-classification rulings.

Contact [email protected] for any questions or corrections.