Caterpillar (NYSE:CAT | CAT Price Prediction) has been one of the most surprising large-cap winners of 2026. The world’s largest construction and mining equipment maker has ridden an AI-driven power generation boom, a record backlog, and aggressive buybacks to a 59.63% year-to-date gain and a 155% one-year run. The question now is how much rally is left.

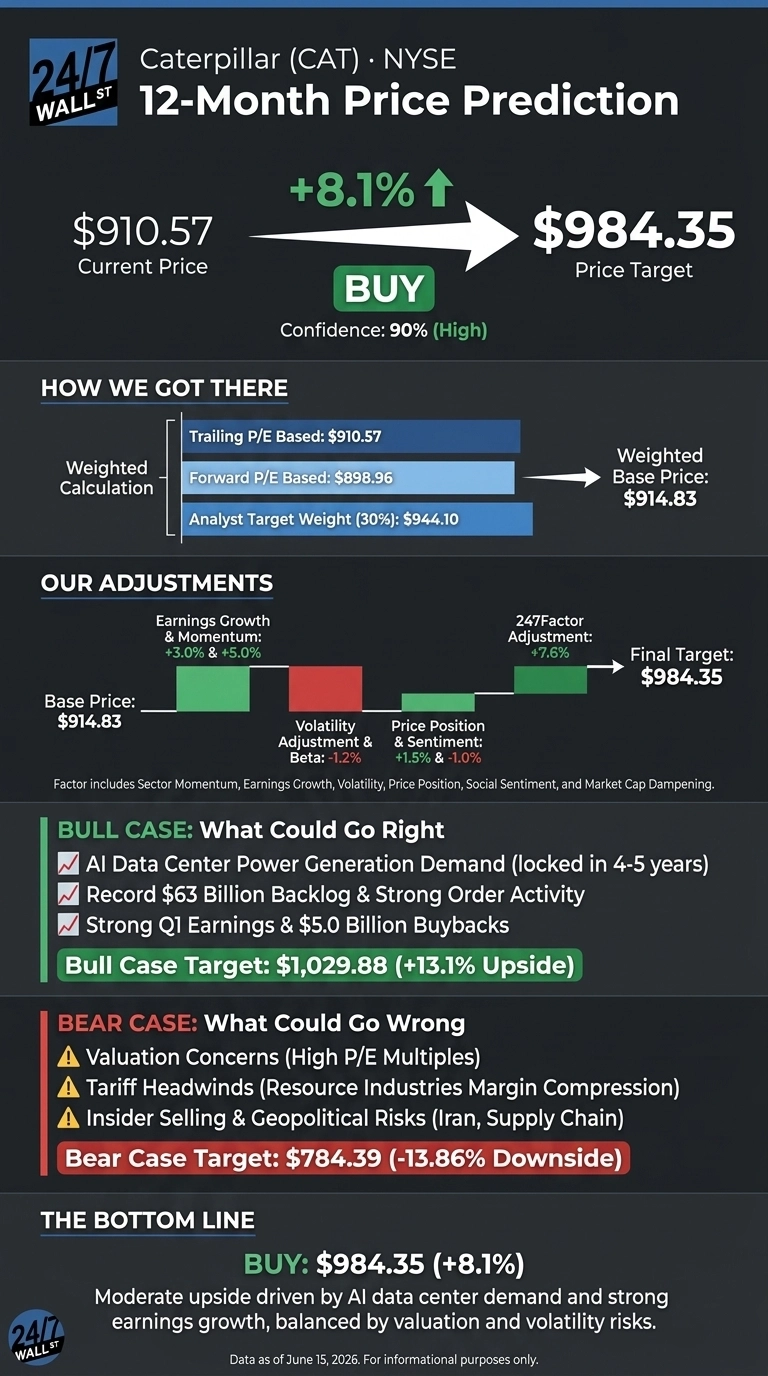

Our 24/7 Wall St. price target for Caterpillar is $984.35, implying 8.1% upside from $910.57. We rate it a buy with a 90% confidence level, the high end of our scale.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $910.57 |

| 24/7 Wall St. Price Target | $984.35 |

| Upside | 8.1% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Data Center Tailwind Reshapes the Story

Caterpillar is trading near its $946.83 52-week high after climbing from a $353.14 low.

The catalyst has been Q1 2026 results released April 30. Revenue jumped 22.22% year over year to $17.4 billion, EPS came in at $5.54 versus a $4.6439 estimate, and Power Generation revenue surged 41% on AI data center demand for large reciprocating engines and turbines. Construction Industries also reaccelerated, with revenue up 38%.

CEO Joe Creed framed it bluntly: “A record backlog provides a strong foundation for continued positive momentum.” That backlog reached $63 billion. Management also raised 2026 sales guidance to low double digits and hiked the dividend 8% to $1.63 per share, the 32nd consecutive year of dividend growth.

The Case for $1,030 and Beyond

Our bull case price target sits at $1,029.88, a 13.1% return. The bull thesis is straightforward. Independent research from PineBridge and MetLife Investment Management argues data center equipment demand is essentially locked in for the next four to five years, with constraints producing around 25% annually in equipment growth. Caterpillar sits squarely in that pipeline through its turbine and reciprocating engine business.

Add a $63 billion backlog, $5 billion in Q1 buybacks, and a Zacks Rank #1 momentum classification, and the path to a re-rating is visible. Analyst consensus sits at $944.10 with 14 Buy and 1 Strong Buy ratings.

The Risks Worth Watching

Our bear case target is $784.39, a 13.86% drawdown. The setup is rich. Caterpillar trades at a 45x trailing P/E and 38x forward, well above its historical range. UBS already downgraded the stock on valuation. Resource Industries segment profit dropped 39% year over year on tariff-driven manufacturing costs, with 7 points of margin compression.

Bulls would counter that the margin hit is concentrated in one segment and largely tariff-mechanical rather than demand-driven, and that dealer inventory builds reflect genuine restocking. Still, with insider activity skewing toward selling and Iran-related supply chain risks rising, a multiple compression toward the high 30s is plausible if 2026 EPS misses.

Caterpillar Price Prediction 2026-2030

The 24/7 Wall St. price target of $984.35 reflects a buy at 90% confidence. The tipping factor is the data center exposure inside Power Generation, which gives Caterpillar a secular growth lane its industrial peers cannot match.

The setup favors investors who can stomach a 1.6 beta and a forward multiple in the high 30s. The thesis weakens if AI capex guidance from hyperscalers cools or if tariff pressure spreads beyond Resource Industries.

Looking further out, here is where our model projects Caterpillar could trade, assuming current growth trajectories and AI infrastructure demand hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $984.35 |

| 2027 | $1,045 |

| 2028 | $1,115 |

| 2029 | $1,180 |

| 2030 | $1,243.25 |

These projections assume Caterpillar continues capturing data center power generation demand and managing tariff costs. Significant upside or downside could come from AI capex cycle shifts or a sustained commodity downturn.