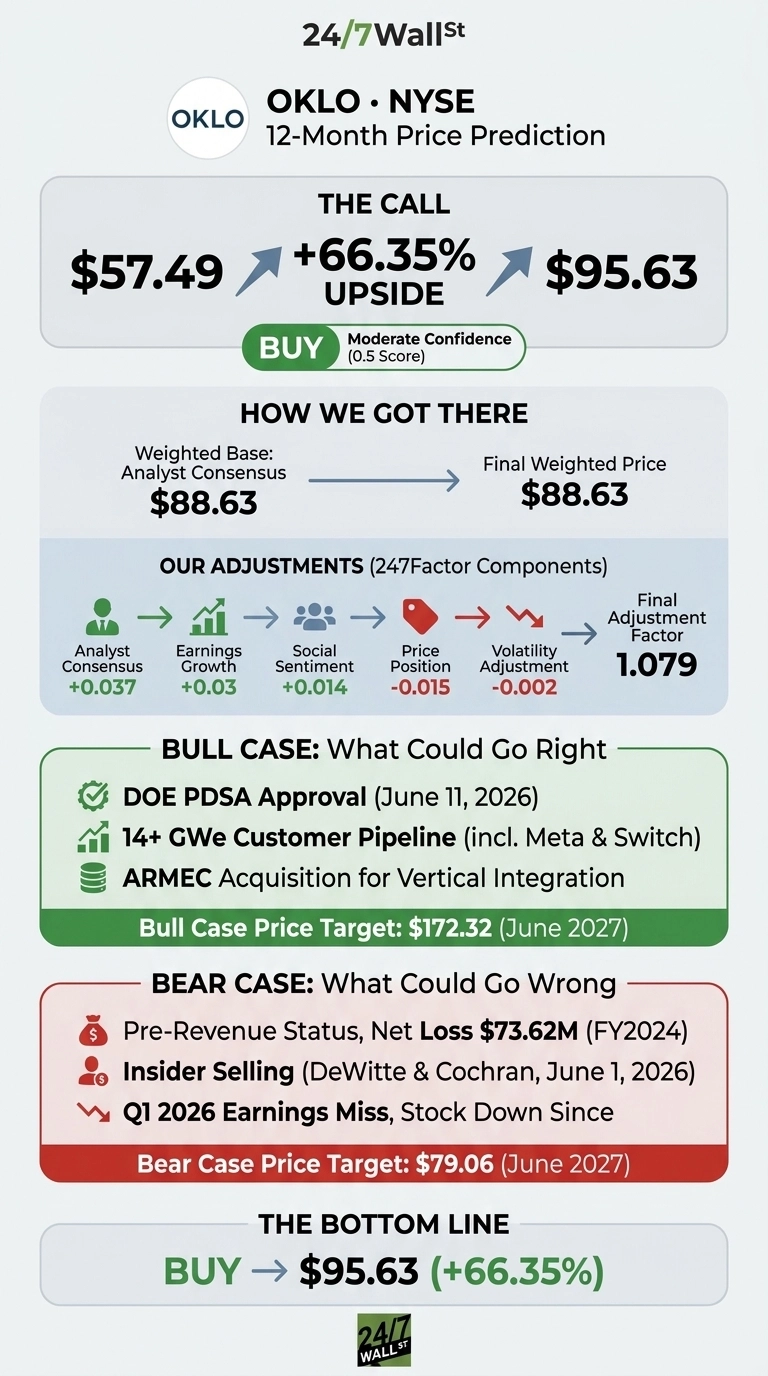

I’ll cut to the chase. Oklo (NYSE:OKLO | OKLO Price Prediction) trades at $57.49, well off its 52-week high of $193.84, and our proprietary model still sees real upside from here.

Our 24/7 Wall St. price target for Oklo is $95.63 over the next 12 months, implying 66.35% upside. The recommendation is buy, with moderate confidence reflecting the pre-revenue execution risk attached to any advanced nuclear name.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $57.49 |

| 24/7 Wall St. Price Target | $95.63 |

| Upside | 66.35% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Brutal Pullback From The October Peak

The story behind the chart is simple: euphoria, then digestion. Oklo touched $162.14 in October 2025 before unwinding sharply. Shares are down 17.47% over the past month and 19.89% year to date, with the stock sitting 54% below the 52-week high. The catalyst stack remains strong.

The U.S. Department of Energy approved Oklo’s Preliminary Documented Safety Analysis for the Aurora Powerhouse at Idaho National Laboratory on June 11, 2026, the third of four steps toward DOE construction authorization. Oklo was also selected for advanced negotiations under the Surplus Plutonium Utilization Program, and closed the ARMEC acquisition on June 4, 2026 to vertically integrate manufacturing.

Offsetting that, co-founders Jacob DeWitte and Caroline Cochran each sold 200,000 shares on June 1, 2026 at $64.99 to $70.45 under pre-arranged 10b5-1 plans.

Why Bulls See A Path To $170

The bull case is anchored in pipeline and policy. Oklo has 14+ GWe under non-binding letters, including a 1.2 GWe binding power agreement with Meta Platforms (NASDAQ:META) and a 12 GW partnership with Switch. The company holds $2.5 billion in cash and marketable securities, giving it runway to deploy commercial power by late 2027 without distress financing.

Canaccord Genuity reiterated Buy with a $125 price target, while Wedbush reaffirmed Outperform at $110. Our internal bull scenario projects $172.32 by June 2027, a 199.74% return if licensing momentum and hyperscaler demand converge.

The Risks Worth Watching

Oklo remains pre-revenue with a FY2024 net loss of $73.62M and forward EPS of -$0.88. The customer pipeline is overwhelmingly non-binding LOIs, not firm contracts. Insider selling near $65 to $70 invites skepticism, though both transactions ran through pre-arranged plans adopted long before recent regulatory wins.

Bears would argue the widening loss reflects necessary R&D and public-company buildout costs ahead of 2027 commercialization, not deteriorating fundamentals. Still, our bear scenario lands at $79.06 over 12 months, with the most relevant tail risk being NRC licensing delay or a HALEU fuel access disruption.

Oklo Price Prediction 2026-2030

The 24/7 Wall St. price target of $95.63 reflects a buy rating at moderate confidence. The tipping factor for me is the regulatory de-risking: PDSA approval, NRC accelerated approval of the Principal Design Criteria, and DOE plutonium program selection have all hit within five weeks.

The constructive case rests on Aurora reaching criticality on schedule and the Switch and META agreements converting to binding offtake. The cautious case applies if NRC licensing slips past 2027 or if Oklo raises equity at a discount to fund first-of-a-kind construction.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $75.41 |

| 2027 | $113.04 |

| 2028 | $153.68 |

| 2029 | $186.72 |

| 2030 | $218.14 |

These projections assume Oklo executes on its 2027 to 2028 Aurora deployment timeline and converts pipeline LOIs into binding contracts. Material upside or downside could come from NRC licensing speed, HALEU fuel availability, or hyperscaler demand for behind-the-meter nuclear.