Super Micro Computer (NASDAQ:SMCI | SMCI Price Prediction) has whipsawed investors. The stock collapsed 29.87% in the past week alone after a $7 billion financing announcement, yet AI infrastructure demand keeps stacking up behind the scenes. I built the 24/7 Wall St. price target on this exact tension.

The 24/7 Wall St. Price Target for SMCI

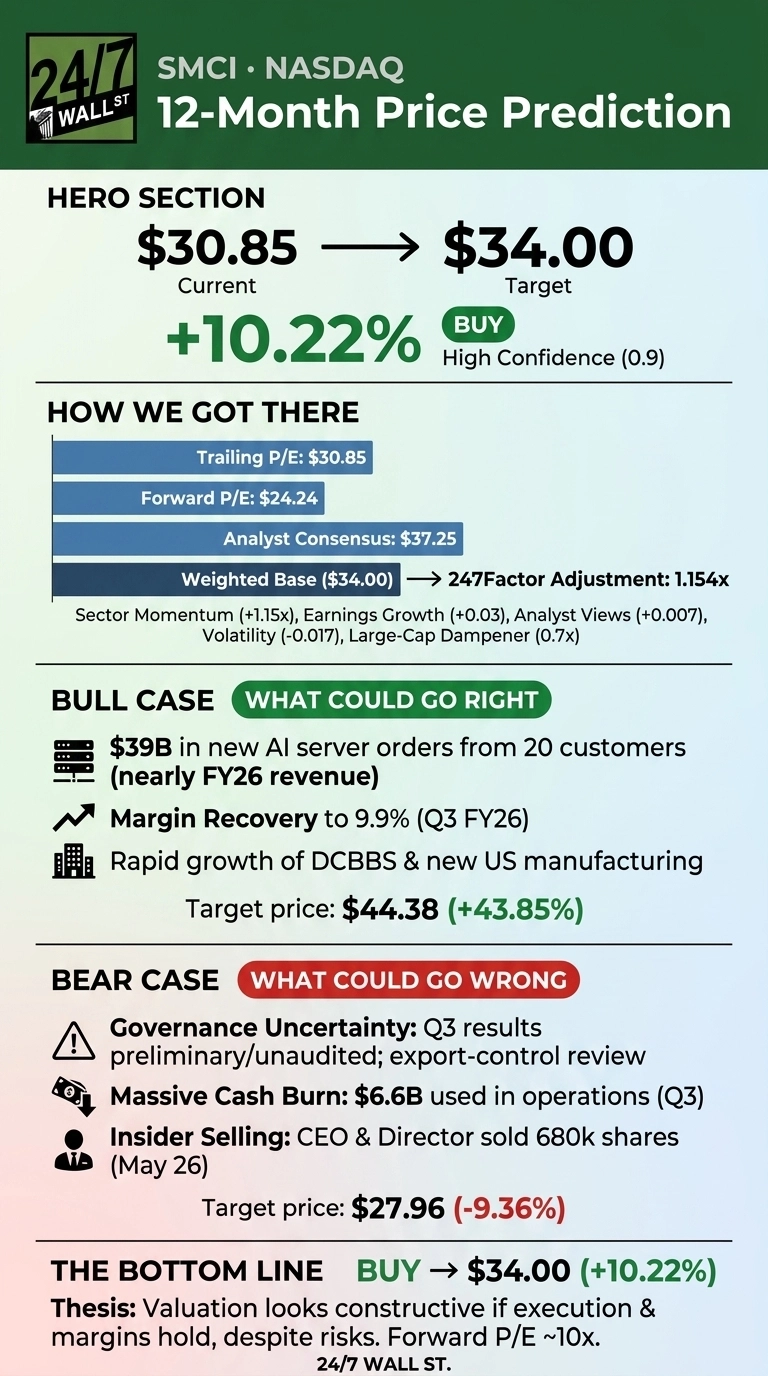

Our 24/7 Wall St. price target for Super Micro Computer (NASDAQ:SMCI) is $34, implying 10.22% upside from the current $30.85. The model rates Super Micro a buy with high confidence (90%), primarily because the post-financing selloff has reset the multiple while the order book keeps growing.

| Metric | Value |

|---|---|

| Current Price | $30.85 |

| 24/7 Wall St. Price Target | $34.00 |

| Upside | 10.22% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Brutal Week Resets the Setup

Super Micro is down 25.77% over the past year but still up 5.4% year to date, sitting roughly 40% below the 52-week high of $62.36. The catalyst for the most recent leg down: a $7 billion equity and equity-linked financing package led by JPMorgan and Goldman to fund AI server components.

Q3 FY26 results, filed May 5, 2026, told the same split story. Non-GAAP EPS of $0.84 beat consensus by 34.51%, while revenue of $10.24 billion grew 122.7% YoY but missed estimates by 17.75%. Crucially, GAAP gross margin recovered to 9.9% from 6.3% the prior quarter.

Why Bulls See $44 and Higher

The bull case is anchored in backlog. Seeking Alpha and Stone Fox Capital point to $39 billion in new AI server orders from 20 customers, nearly matching the full-year revenue target.

Super Micro also closed a $2 billion India deal with Gorilla Technology and inked a nuclear-power MOU with NANO Nuclear. CEO Charles Liang says “our margin recovery and the rapid growth of our DCBBS business demonstrate that our business remains robust.” Our bull-case price target lands at $44.38, a 43.85% return scenario.

What Could Go Wrong

The bear case starts with governance. Q3 results remain preliminary and unaudited pending a Board independent review tied to export-control matters. Wolfe Research initiated coverage at Peer Perform, and Raymond James trimmed its target to $39 from $45. CEO Liang and Director Liu each disposed of 340,000 shares on May 26, 2026, a combined 680,000-share signal investors noticed.

Cash dynamics are the other concern: $6.6 billion of cash used in operations in Q3 and $8.8 billion in total bank debt and convertibles. Bulls would counter that the cash burn reflects aggressive inventory positioning for the Blackwell Ultra ramp. Our bear-case scenario lands at $27.96.

SMCI Price Prediction 2026-2030

The 24/7 Wall St. price target of $34 reflects a buy rating at 90% confidence. The decisive factor is valuation: a forward P/E of roughly 10x on a company growing revenue triple digits already prices in significant skepticism.

The setup looks constructive if the Board review closes cleanly and margins hold above 9%. The thesis weakens if the export-control investigation widens or if Q4 EPS lands below the $0.65 guidance floor.

Looking further ahead, here is where our model projects Super Micro could trade, assuming current growth trajectories and the AI infrastructure cycle hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $34.00 |

| 2030 | $44.06 |

These projections assume Super Micro executes on its DCBBS roadmap and clears the governance overhang. Significant upside or downside could result from the export-control resolution and the pace of Blackwell Ultra deliveries.

Contact [email protected] for any questions or corrections.