Eli Lilly (NYSE: LLY | LLY Price Prediction) and Pfizer (NYSE: PFE) just delivered Q1 2026 results that read like two different chapters of the same drug industry.

Lilly is sprinting through an obesity gold rush. Pfizer is rebuilding after COVID and buying its way into the same race. Both beat estimates, but the businesses underneath could not feel more different.

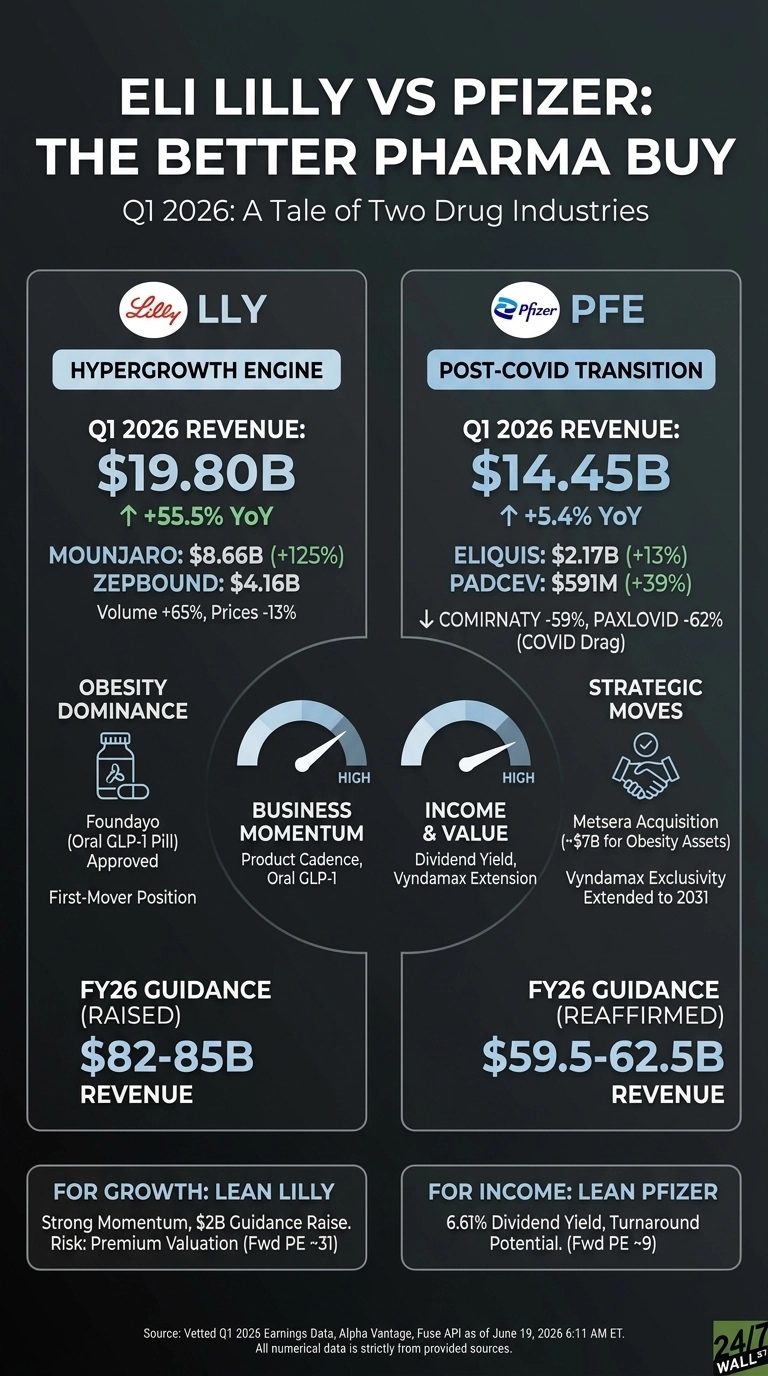

GLP-1 Volume Carries Lilly. Eliquis and Oncology Carry Pfizer.

Lilly posted $19.80B in revenue, up 55.5%, with Mounjaro alone contributing $8.66B on a 125% jump. Zepbound added another $4.16B. Volume rose 65% while realized prices fell 13%, a trade Lilly is clearly willing to make to grab share before rivals arrive.

Pfizer pulled $14.45B in revenue, up 5.4%, with Eliquis at $2.17B (+13%) and Padcev surging 39%. The COVID drag is real: Comirnaty fell 59% and Paxlovid dropped 62%. CEO Albert Bourla called it a “defining period for Pfizer,” which is a polite way of saying every launch matters.

| Business Driver | Lilly | Pfizer |

| Main growth engine | Mounjaro, Zepbound | Eliquis, oncology, Vyndaqel |

| Q1 revenue growth | 55.5% | 5.4% |

| FY26 guidance | Raised to $82B to $85B | Reaffirmed $59.5B to $62.5B |

One Owns Obesity Today. The Other Just Paid To Enter.

Lilly extended its lead with FDA approval of Foundayo, the first oral GLP-1 pill with no food or water restrictions. CEO David Ricks framed it bluntly: “2026 is off to a strong start…A key milestone was the U.S. FDA approval of Foundayo.”

Pfizer’s answer was a checkbook. The roughly $7B Metsera deal brings ultra-long-acting obesity assets into a 2026 pipeline featuring around 20 pivotal study starts. The Vyndamax patent settlement pushing US exclusivity to June 2031 matters more than the headlines suggest, since it softens the loss-of-exclusivity cliff Pfizer has been bracing investors for.

Valuation tells the same story. Lilly trades at a forward PE near 31, with analysts targeting $1,215.79. Pfizer sits at a forward PE around 9, with a 6.61% dividend yield doing most of the heavy lifting for shareholders.

What I Want To See Next From Both

For Lilly, the watch item is whether oral Foundayo can hold pricing as supply scales and Medicare negotiations close in. Shares already cooled 5.37% in the past week despite a 40.92% one-year gain, hinting that expectations are stretched.

For Pfizer, I want proof Metsera can deliver Phase 3 data that justifies the spend, plus confirmation that Padcev’s August 17, 2026 MIBC decision goes through cleanly.

Why I Lean Lilly For Growth and Pfizer For Income

If I had to pick one for the next three years on business momentum alone, I lean Lilly. The product cadence, the $2 billion guidance raise, and the oral GLP-1 first-mover position are hard to argue with. The valuation remains a key risk factor for new entrants at current levels.

Pfizer fits a different investor entirely. The 6.61% yield, the Vyndamax extension, and CEO Bourla’s steady personal buying of phantom stock units through the spring suggest a credible turnaround setup. The two stocks serve distinct portfolio roles, and the next pricing update will be a key signal for assessing how durable that 55% growth really is.

Contact [email protected] for any questions or corrections.