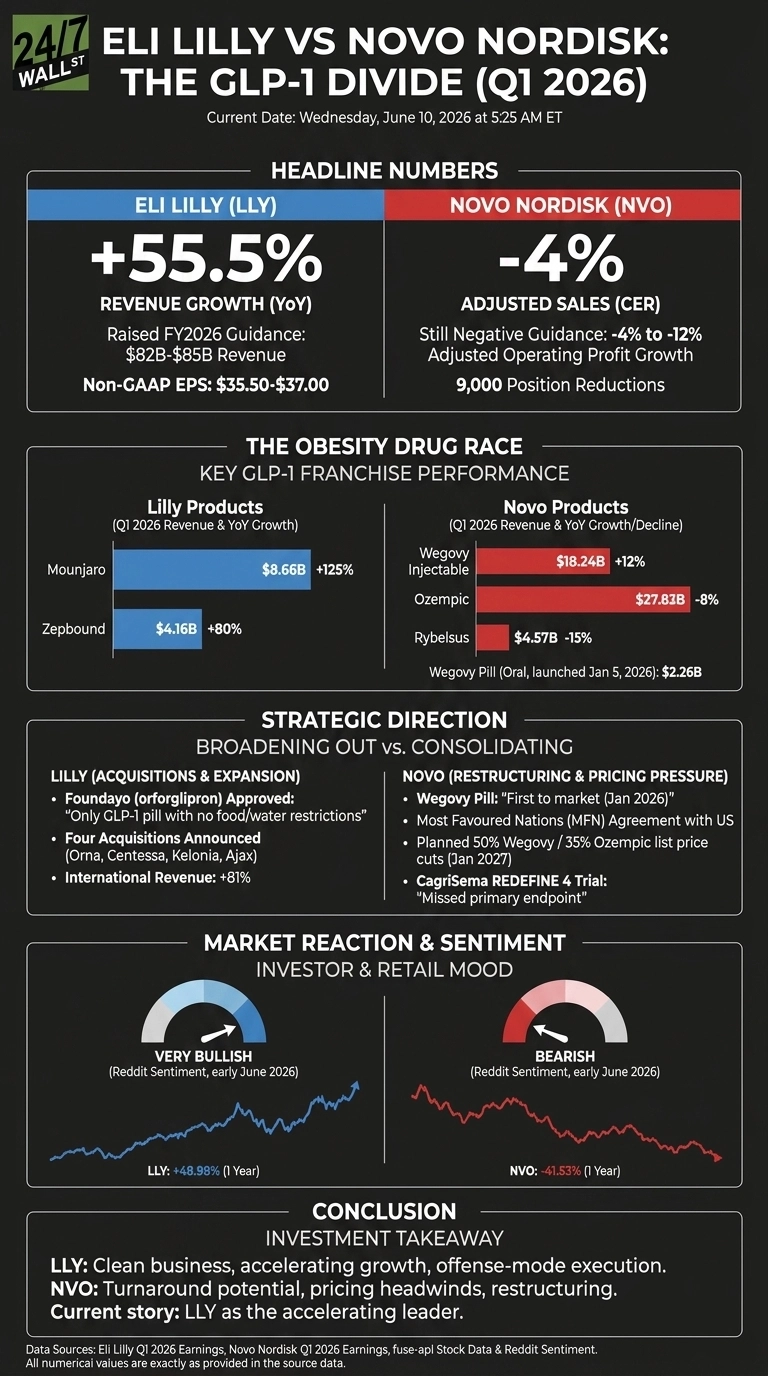

Eli Lilly (NYSE: LLY | LLY Price Prediction) and Novo Nordisk (NYSE: NVO) reported Q1 2026 results that pulled the GLP-1 duopoly apart. Lilly grew revenue 55.5% and raised guidance.

Novo posted a 4% adjusted sales decline at constant currency and is cutting 9,000 jobs. Both call obesity the prize, but their quarters tell very different stories about who is winning it.

Mounjaro Roars. Wegovy Holds The Line.

Lilly’s quarter was carried by tirzepatide. Mounjaro brought in $8.66 billion, up 125% year over year, helped by international launches and China’s NRDL inclusion. Zepbound added $4.16 billion, up 80%.

Volume jumped 65% while realized prices fell 13%, a deliberate trade per CEO David Ricks. The FDA approved Foundayo (orforglipron), the only GLP-1 pill with no food or water restrictions.

| Q1 2026 Driver | Eli Lilly | Novo Nordisk |

| Revenue trajectory | +55.5% YoY | -4% adjusted at CER |

| Lead obesity product | Zepbound, +80% | Wegovy injectable, +12% |

| Oral GLP-1 entry | Foundayo, no food/water rules | Wegovy pill, first to market |

| 2026 guidance move | Raised to $82B-$85B | Still -4% to -12% CER |

Novo’s franchise is splitting. Wegovy injectable grew 12% to $18.24 billion, and the new Wegovy pill, launched January 5, 2026, booked $2.26 billion with over 1 million patients. Ozempic slid 8%, Rybelsus dropped 15%, and US sales fell 11%. CEO Mike Doustdar leaned on the pill story because the rest of the portfolio is shrinking.

Broadening Out vs. Battening Down

Lilly is buying growth in four directions, announcing acquisitions of Orna, Centessa, Kelonia, and Ajax across cell therapy, sleep-wake biology, in vivo CAR-T, and myelofibrosis. Ebglyss jumped 141% and Jaypirka rose 79%. International revenue climbed 81%, suggesting the global ramp is only starting.

Novo is consolidating around semaglutide and cagrilintide, restructuring costs, and absorbing the Most Favoured Nations pricing deal. The CagriSema REDEFINE 4 trial missed its primary endpoint, even with 23% weight loss, dents the next-generation thesis. A planned 50% Wegovy list price cut in January 2027 will pressure margins.

What I Want To See Next

I will watch how quickly Foundayo scales relative to Novo’s oral semaglutide, since the pill war is now the obesity story. Lilly’s retatrutide Phase 3 readouts and the Taltz plus Zepbound psoriasis combo could open new categories.

For Novo, the question is whether Medicare Part D coverage starting July 1, 2026 can offset price cuts coming six months later. Retail mood reflects the split: LLY sentiment turned very bullish on Reddit in early June, while NVO drifted to bearish.

Why I Lean Toward Lilly, But Won’t Write Off Novo

Lilly is the cleaner business. Revenue growth of 55.5%, a guidance raise to $35.5-$37 in non-GAAP EPS, and a stock up 48.98% over the past year reflect offense-mode execution. The valuation prices in a lot, so any Foundayo stumble would sting.

Novo interests me as a turnaround. Shares are down 41.53% over a year and 14.22% year to date, the Wegovy pill is working, and gross margin sits at 81%. Investors weighing the name will need to weigh 2027 price cuts and patent expirations against the turnaround setup. For now, the accelerating franchise looks like the cleaner story, with Novo worth revisiting once the MFN pricing math is digested.

Contact [email protected] for any questions or corrections.