ServiceNow (NYSE:NOW | NOW Price Prediction) grew revenue 20.88% for the full year with CEO Bill McDermott promising to build “the AI control tower for business reinvention.” Yet shares sit at $95.04, down 37.96% YTD despite Q4 cRPO growth of 25% YoY and Now Assist ACV more than doubled.

McDermott calls it “the AI-defining enterprise software company in the 21st century.” The market disagrees. Can ServiceNow reach $350 by 2027? Here is the analysis.

What’s Holding ServiceNow Back

The selling has been relentless. ServiceNow is down 7.8% over the past week, 6.67% over the past month, and 51.61% over the past year.

Competition from AI-native solutions is breaking the stock. Columbia Global Technology Growth Fund flagged concerns about ServiceNow’s traditional licensing model facing headwinds from the growing adoption of AI-native solutions.

Salesforce (NYSE:CRM) faces similar pressure, signaling sector repricing rather than a NOW-specific issue. With a beta of 0.927, this reflects fundamental skepticism. Layoffs of 63 employees in San Diego contradicted McDermott’s no-layoffs pledge. Shares now trade below both the $99.24 50-day and $136.78 200-day moving averages.

Wall Street Sees 49% Upside. Our Model Sees 220%

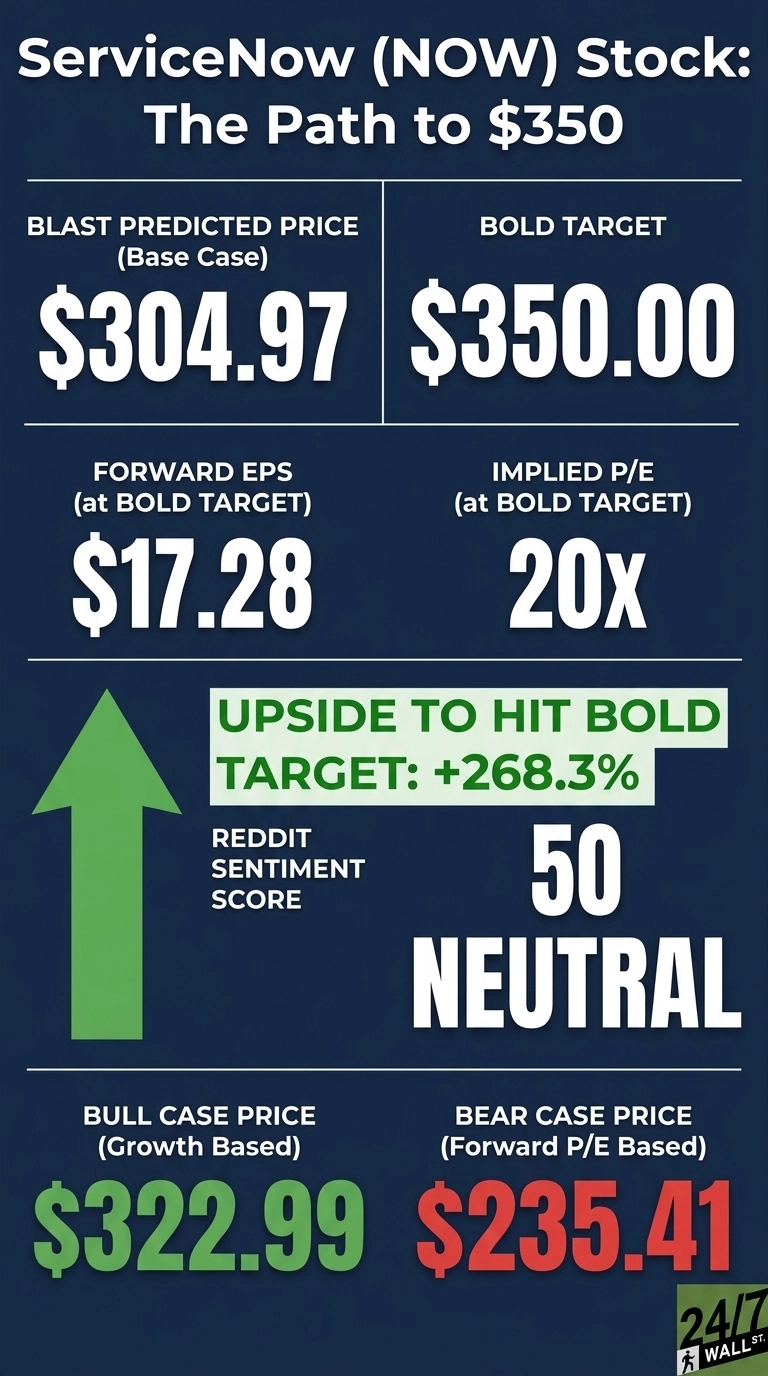

Analysts are bullish. 48 analysts cover NOW with an average target of $141.98, broken down as 9 strong buys, 34 buys, 4 holds, and 1 sell. Our base case for June 2027 is $304.97, implying 220.89% upside with 90% confidence.

Bull case: $322.99. Bear case: $235.41. Analysts appear anchored to post-correction prices and underestimate the earnings ramp. With 90% bullish analyst sentiment and forward EPS materially higher than today’s run-rate, consensus looks conservative.

The Path to $350 Per Share

Reaching $350 from $95.04 requires a gain of 268.3%.

With forward EPS of $17.28, a $350 price implies a forward P/E of 20x. Our base case of $304.97 implies 7x, so the bold target requires roughly 13x additional multiple expansion against forward earnings.

Three factors support that expansion. First, the 1.184 247Factor adjustment reflects a 1.15x tech sector multiplier and 90% bullish analyst consensus. Second, Now Assist’s 2026 target was raised from $1 billion to $1.5 billion, with deals containing 3+ Now Assist products growing nearly 70% YoY.

Third, McDermott told investors “there’s a perfect correlation between enterprise AI from any source and ServiceNow’s expansion.” If half proves true, the multiple closes the gap. Primary risk: consumption-based AI-native rivals erode seat-based pricing before Now Assist scales.

ServiceNow’s Current Valuation vs Earnings Power

NOW trades at a forward P/E of around 6x using our model or 23x on Alpha Vantage consensus. Both look cheap for a business guiding 20.5% to 21% subscription growth and a 32% operating margin.

The stock sits between its $211.48 52-week high and $81.24 low, much closer to the floor. The 10-year return is still 554.55%. The compounding is real, despite the ugly past year.

Is $350 Realistic?

$350 requires a 268.3% gain from $95.04. That is a stretch, not a layup, even with our 220% base case.

For it to happen, Now Assist must keep doubling, Armis must deliver promised security cross-sell, and software multiples must recover as rate-cut momentum returns. A renewed decline in enterprise software multiples would derail it. We’ve outlined the blueprint for how ServiceNow could reach $350 in 2027.

Contact [email protected] for any questions or corrections.