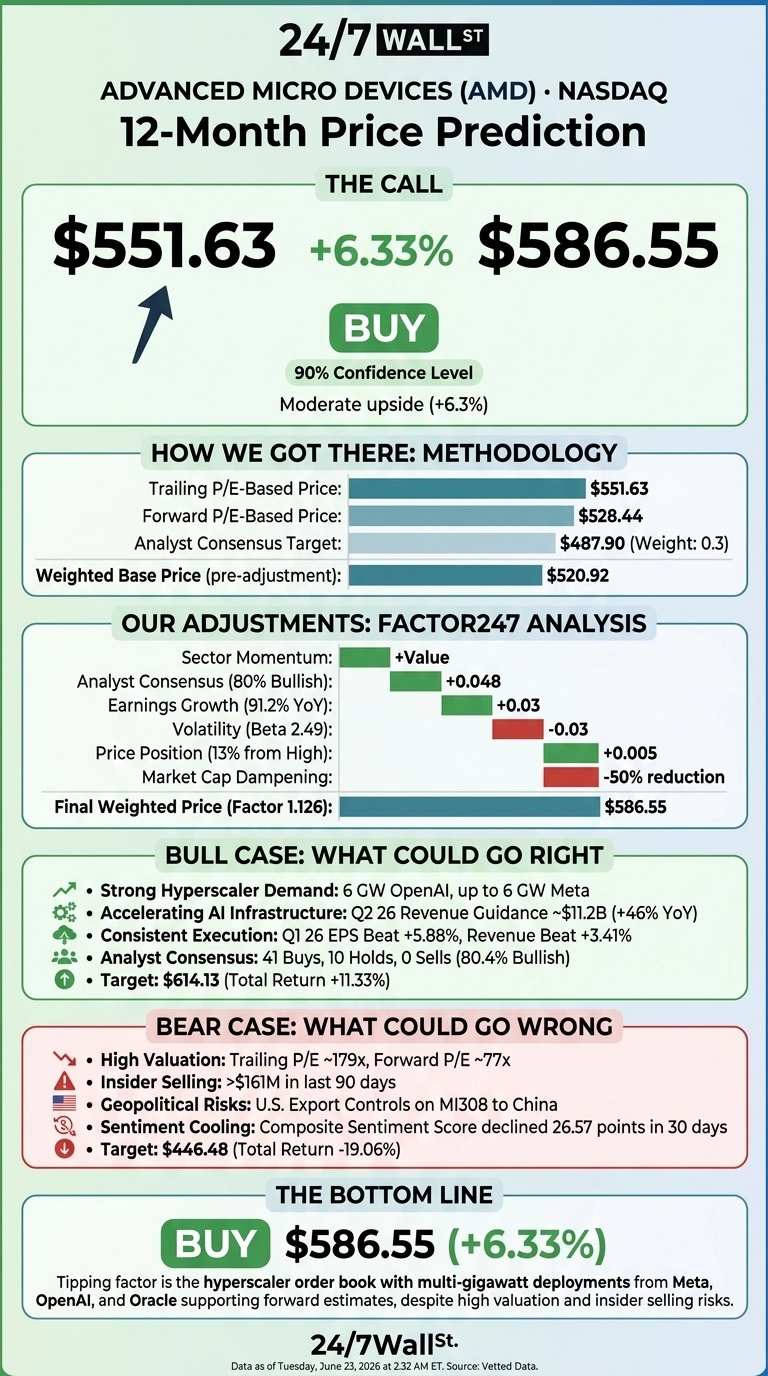

I’m opening with the headline number. Our 24/7 Wall St. price target for Advanced Micro Devices (NASDAQ:AMD | AMD Price Prediction) is $586.55 over the next 12 months, against a current quote of $551.63. That implies 6.33% of upside and a buy recommendation, with our model registering 90% confidence.

The setup is unusual: a stock that has already run hard, yet still sits below where our proprietary blend and an 80% bullish analyst wall converge.

| Metric | Value |

|---|---|

| Current Price | $551.63 |

| 24/7 Wall St. Price Target | $586.55 |

| Upside | 6.33% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $128 to $551 in 12 Months

AMD has been one of the defining trades of 2026. Shares are up 17.99% over the past month, 157.58% year to date, and 330.15% over the past year from a starting price of $128.24. AMD trades 13% below the 52-week high of $562.99.

The catalyst is fundamental. Q1 2026 revenue hit $10.253 billion, up 37.9% YoY, beating expectations by 3.41%, while non-GAAP EPS of $1.37 beat by 5.88%. Data Center revenue grew 57% YoY to $5.77 billion. Recent news of a 30 MW Rackspace deployment and the MEXT memory-optimization acquisition extended the AI infrastructure narrative.

The Case for $614 and Higher

Bulls anchor on the customer book. Lisa Su told investors “Customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.” The OpenAI agreement covers 6 GW of GPU deployment, Meta committed to up to 6 GW of Instinct GPUs and named AMD lead supplier for 6th Gen EPYC Venice/Verano, and Oracle is standing up a 50,000-GPU Helios supercluster in Q3 2026.

Q2 2026 guidance of $11.2 billion implies 46% YoY growth with non-GAAP gross margin expanding to 56%. Of 51 analysts, 5 rate Strong Buy, 36 Buy, 10 Hold, and zero Sell. Our bull-case path takes AMD to $614.13, an 11.33% total return.

What Could Go Wrong

AMD trades at a trailing P/E of 179 and forward P/E of 77. That is priced for flawless execution. U.S. export controls on MI308 GPUs already triggered $800 million in Q2 2025 inventory charges, and any escalation in China policy could repeat the hit.

Insider activity is also a yellow flag: insider transactions over the last 90 days exceeded $161 million in selling, including the CEO. Reddit sentiment has cooled, with the composite score sliding 26.57 points over 30 days.

The counterfactual matters. Heavy insider sales after a 330.15% run are partly diversification, not a thesis change, and the elevated P/E reflects depressed trailing earnings that the forward number normalizes. Still, our bear-case milestone is $446.48, a 19.06% drawdown if AI capex pauses.

AMD Price Prediction 2026-2030

Our 24/7 Wall St. price target of $586.55 is a buy at 90% confidence. The tipping factor is the hyperscaler order book: when Meta, OpenAI, and Oracle all anchor multi-gigawatt deployments on the same roadmap, the forward EPS estimate has real support.

I’d be a buyer here if MI450 ramp commentary stays positive through Q3 2026. I’d stay on the sidelines if China export policy tightens further or hyperscaler capex guidance softens.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $586.55 |

| 2027 | $631 |

| 2028 | $668 |

| 2029 | $697 |

| 2030 | $724.81 |

These projections assume AMD continues executing on its MI450 and EPYC roadmap with hyperscaler capex sustained through the decade. Significant upside or downside could result from custom-silicon competition, China export policy, or a step-change in inference economics.

Contact [email protected] for any questions or corrections.