Taiwan Semiconductor Manufacturing (NYSE:TSM | TSM Price Prediction) just put the rest of the chip sector on notice. Monthly revenue for May 2026 hit NT$416.98 billion, up 30.1% year over year, and CEO C.C. Wei is telling investors the company will “grow by above 30% in U.S. dollar terms” for full-year 2026.

Shares are already up 44.32% year to date, closing at $436.39 after a 6.69% single-day pullback. Can TSM print $500 before 2026 is over?

What’s Holding TSMC Back Right Now

TSM is up 109.73% over the past year and trades just 1% from its 52-week high of $476.31. The 8.12% one-month gain ran headfirst into valuation fatigue, and the most recent session lopped off 6.69% in a single day.

Wei flagged caution on the call, citing “the impact of rising component prices” and Middle East macro risks. With a beta of 1.25, this stock amplifies tech-sector wobbles. Add a patent infringement complaint at the U.S. ITC and persistent NT-dollar FX pressure, and traders have hit pause near $440.

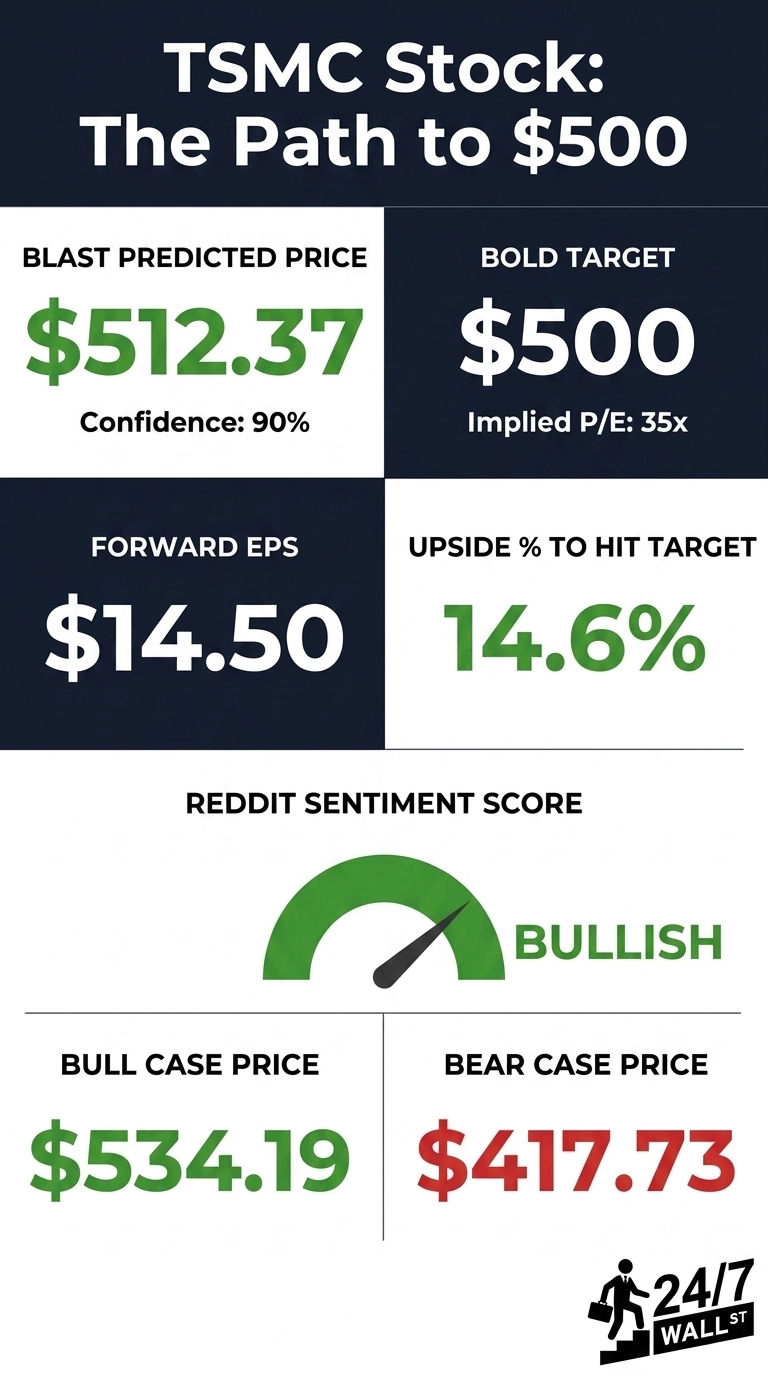

Wall Street Sees 8.5% Upside. Our Model Says More

Sell-side analysts carry an average target of $473.40, backed by 5 Strong Buys, 12 Buys, 2 Holds, and zero sell ratings. Our internal model anchors on a base case of $512.37 with a bull case of $534.19 and a bear case of $417.73. Confidence is rated at 90%.

With 89% of the bullish/bearish coverage tilted bullish and quarterly earnings growth running at 58.4% year over year, the Street is anchoring to old EPS assumptions. $500 sits between consensus and our base case, the most reachable round number on the board. BofA raised the firm’s price target on TSMC to $590 from $490 and keeps a Buy rating on the shares.

The Path to $500 Per Share

Reaching $500 from today’s price of $436.39 requires a gain of 14.6%. With forward EPS of $14.50, a price of $500 implies a forward P/E of 35x. Our base case of $512.37 already implies 36x, so $500 actually demands slightly less multiple expansion than where our model already sits.

Earnings do the heavy lifting. Q1 2026 net income jumped 43.82% YoY, and Q2 guidance implies USD $39.0 billion to $40.2 billion in revenue, a 32% YoY increase at the midpoint. Wei said “AI-related demand continues to be extremely robust” and that the shift to agentic AI is driving “higher 50s of CAGR” in AI accelerator demand.

Add the 35% Arizona investment tax credit effective January 1, 2026 and a $52-56 billion CapEx envelope, and the forward multiple compresses naturally as EPS catches up. The primary risk is a Taiwan geopolitical shock that re-rates the entire foundry complex lower.

Where TSMC Trades Today vs Its Earnings Power

At $436.39 against forward EPS of $14.50, TSM trades at a forward P/E of roughly 30x. That is reasonable for a business compounding earnings near 50%. Shares sit in the upper third of the 52-week range of $218.79 to $476.31, and the 10-year return is 2,086.07%. When a company owns the leading-edge node and prints 58% earnings growth, paying 30x forward is the bull case.

Is $500 Realistic?

Reaching $500 requires a 14.6% gain from here. That is realistic before year-end 2026.

Three things need to go right: Q2 results hit the upper end of Wei’s $40.2 billion guide, gross margins land above 66%, and the AI accelerator order book stays at the higher 50s CAGR Wei flagged. What derails it is a Taiwan Strait headline or a meaningful customer capex pause. We’ve outlined the blueprint for how Taiwan Semiconductor Manufacturing could reach $500 in 2026.

Contact [email protected] for any questions or corrections.