I keep buying NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) because every quarter the company reports, the math behind my thesis gets stronger. That is the whole confession. I have been adding on every pullback this year, including the 4.13% drop on June 23 that pushed shares back to $200.04, and I plan to keep doing it through the back half of 2026. Here is why.

The core thesis in human terms

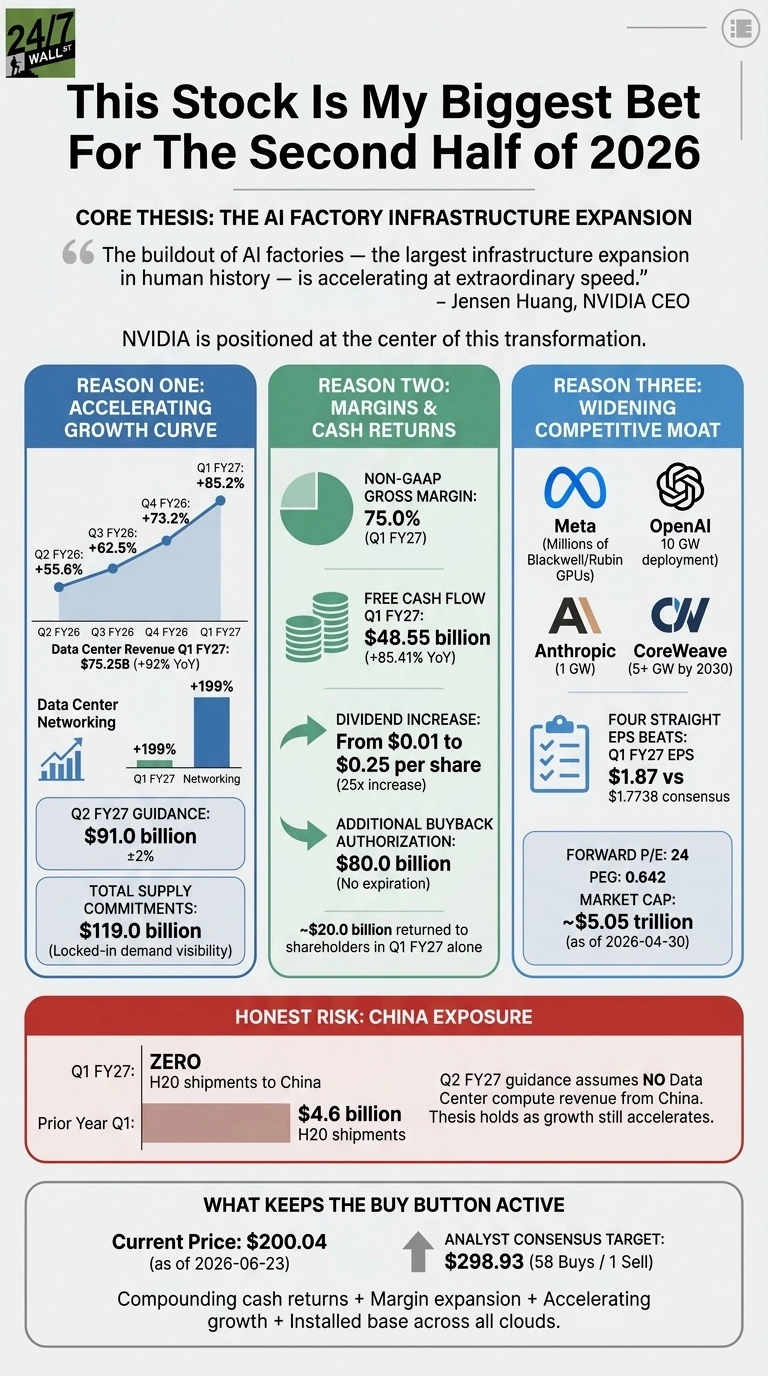

Jensen Huang calls what is happening right now “the largest infrastructure expansion in human history.” I think he is right, and I think NVIDIA sits at the toll booth. Every hyperscaler, sovereign, neocloud, and enterprise that wants to train or serve a frontier model has to come through this company’s stack. That is a structural position I want to own for the next decade.

Three reasons the thesis holds

Reason one: the growth curve is accelerating. Revenue growth has gone +55.6% in Q2, +62.5% in Q3, +73.2% in Q4, and +85.2% in Q1 FY27. Data Center revenue hit $75.25 billion last quarter, up 92% year over year, with networking inside that segment growing 199%.

Management guided Q2 FY27 to $91 billion, and they have beaten the prior two guides by billions. Total supply commitments now sit at $119 billion. That is locked-in demand visibility.

Reason two: margins and cash returns are doing the work. Non-GAAP gross margin printed at 75%. Free cash flow last quarter was $48.55 billion, up 85.41%. The board raised the dividend from $0.01 to $0.25 per share and authorized an additional $80 billion buyback on top of $38.5 billion still available.

Roughly $20 billion came back to shareholders in a single quarter. That is a capital return program I want compounding alongside my position.

Reason three: the moat keeps widening. The customer list reads like the entire AI economy: Meta committing to millions of Blackwell and Rubin GPUs, OpenAI on 10 gigawatts, Anthropic on 1 gigawatt, CoreWeave on 5+ gigawatts by 2030.

Four straight EPS beats, with last quarter at $1.87 against a $1.7738 consensus. And the valuation looks reasonable for this growth rate: forward P/E of 24, PEG of 0.642, against a market cap near $5.05 trillion.

The real risk

China. NVIDIA shipped zero H20 compute products to China last quarter, against $4.6 billion in the year-ago quarter. The Q2 FY27 guide assumes no Data Center compute revenue from China at all. That is a real hole in the business that export restrictions could keep open indefinitely.

What keeps me buying anyway: the company guided to $91 billion with that revenue already zeroed out, and growth is still accelerating. The thesis holds even with China taken to zero.

What keeps the buy button active

Wall Street consensus target sits at $298.93 from 58 buys against 1 sell. Forward P/E of 24. A dividend that just jumped 25x. A buyback authorization with no expiration. An installed base running every cloud and every frontier model.

I own NVIDIA because the AI factory buildout is a multi-year story and the company collecting the toll is also returning cash and compounding margins while it grows. I will keep buying for as long as the receipts say I should.

Contact [email protected] for any questions or corrections.