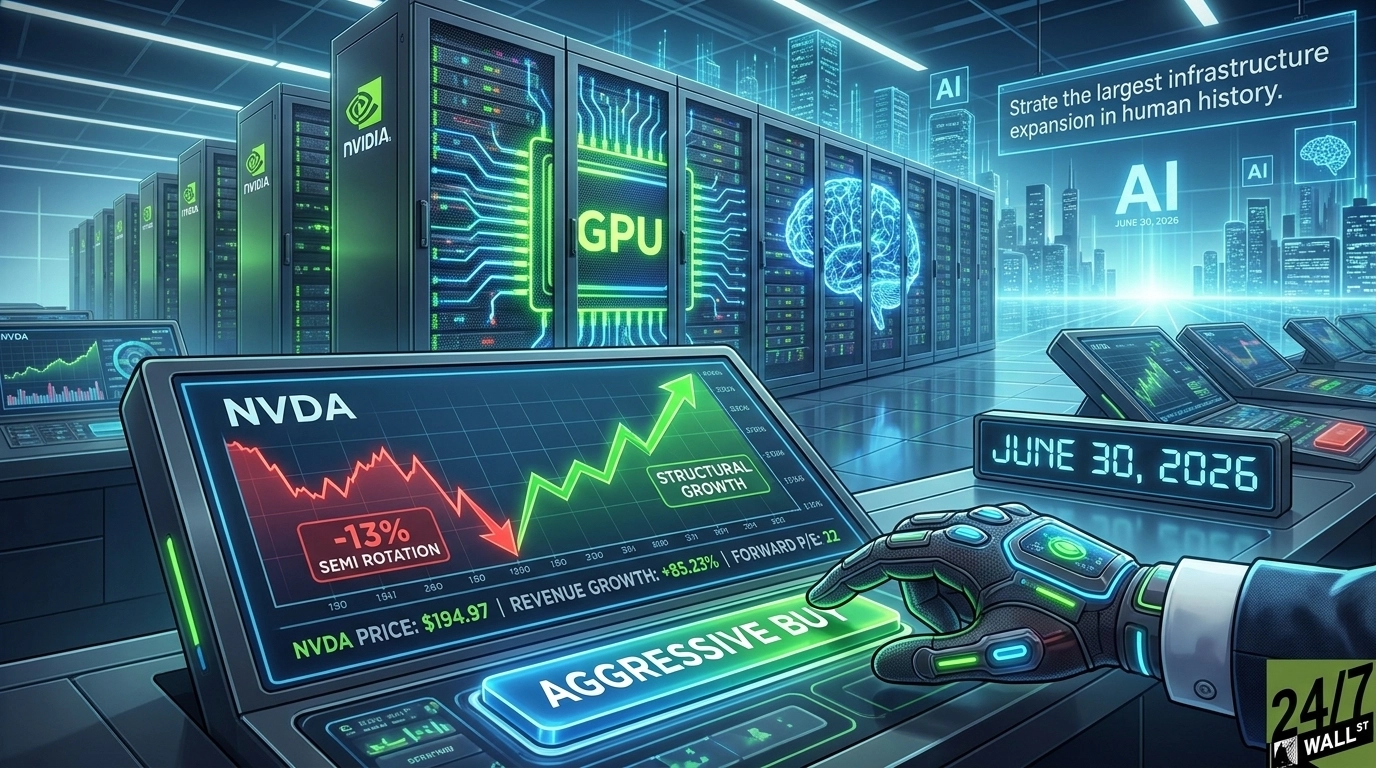

I bought NVIDIA again last Friday, and I plan to buy it again this week if the selloff holds. That makes five additions in eight weeks for me, and the case for the next one has only gotten stronger. NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) is down 13% in June and 7.55% over the past month, sitting at $194.97 while the company is printing the strongest fundamentals it has ever produced. That gap is why my finger keeps finding the buy button.

The thesis is simple. I am buying the only company selling the picks and shovels for what Jensen Huang calls “the largest infrastructure expansion in human history.” The institutional rotation out of semiconductors leaves NVIDIA’s business intact while lowering the price I pay to own it.

The Numbers That Keep Me Adding

Start with Q1 FY2027. Revenue came in at $81.615 billion, up 85.23% year over year, beating consensus by 3.16%. Non-GAAP EPS landed at $1.87 versus the $1.7738 estimate, the fourth consecutive earnings beat. Net income grew 210.63% YoY to $58.321 billion. Free cash flow hit $48.554 billion, up 85.41%. Non-GAAP gross margin held at 75.0%, versus 60.8% a year ago. Those are platform margins, and they are widening.

Growth is accelerating. Quarterly revenue growth moved from 55.6% to 62.5% to 73.2% to 85.2% across the last four quarters. Forward guidance calls for $91.0 billion in Q2 revenue, and that number assumes zero Data Center compute revenue from China.

Then there is the capital return. The board raised the quarterly dividend from $0.01 to $0.25 per share and approved an additional $80.0 billion buyback authorization on top of $38.5 billion still outstanding. NVIDIA returned roughly $20.0 billion to shareholders in Q1 alone. At a forward P/E of 22 with revenue compounding above 80%, that math works for me.

The Moat I Cannot Find Anywhere Else

NVIDIA has Meta committed to millions of Blackwell and Rubin GPUs, OpenAI signed up for at least 10 gigawatts of NVIDIA systems, Anthropic at 1 gigawatt, and CoreWeave building 5+ gigawatts of AI factories by 2030. Data Center networking revenue grew 199% YoY, proof that the full-stack platform is being adopted alongside the GPUs. The $119.0 billion in supply commitments tells me management sees demand years out.

The Risk I Refuse to Ignore

China is gone from the Q2 outlook. Zero Data Center compute revenue assumed, against $4.6 billion in H20 shipments in the year-ago quarter. Insiders also sold heavily in June, including coordinated dispositions by CEO Jensen Huang, CFO Colette Kress, and three other executives at $207.41 on June 17. I sat with both facts. The China hole is real, and the company guided to $91 billion anyway. The insider sales follow pre-set 10b5-1 plans at prices above where I am buying today. The thesis holds.

Why the Buy Button Stays Active

The five-year return on NVIDIA is 878.06%. The ten-year is 16,943.1%. Those are history. I am buying the cash flows underneath them at a forward multiple of 22, with a 25x dividend hike fresh in the account and an $80 billion buyback at my back. The rotation handed me a price. I intend to use every dollar of it.

Contact [email protected] for any questions or corrections.