Enterprise Products Partners (NYSE:EPD | EPD Price Prediction) is built for decade-long ownership because it sits on irreplaceable midstream infrastructure that collects fee-based tolls regardless of where crude or natural gas trades on any given morning. For an investor in their 50s or 60s who has been chewed up chasing momentum, the EPD profile fits a register-for-distribution-reinvestment, leave-it-alone holding.

Pillar One: Durability That Cannot Be Replicated

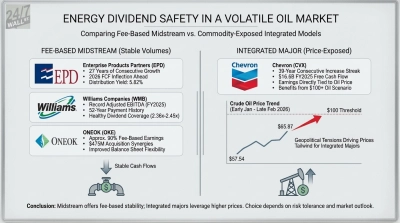

Enterprise operates over 50,000 miles of pipelines, along with 300+ million barrels of storage capacity and Gulf Coast export terminals that no new entrant can realistically replicate. The economics are tollbooth simple: roughly 80% or more of operating cash flow comes from fixed-fee, long-term take-or-pay contracts, and nearly 90% of long-term contracts include inflation-adjustment provisions. Producers pay Enterprise to move volumes whether NGL prices sit at $0.57 a gallon or $0.67 a gallon. Q1 2026 set 12 new operational records, including natural gas processing inlet volumes of 8.3 Bcf/d and NGL fractionation of 1.9 MMBPD, up 16% year over year.

Pillar Two: Income That Compounds Without Heroics

The current quarterly distribution sits at $0.55 per common unit, or $2.20 annualized, producing a yield of roughly 5.88% at the recent unit price of $36.52. Management is now on track for its 28th consecutive year of distribution growth, the longest streak among US midstream companies. Distribution coverage in Q1 2026 was 1.8 times, and the trailing 12-month payout was just 57% of adjusted cash flow from operations. Since its 1998 IPO, Enterprise has returned over $63 billion through distributions and buybacks. That is the engine: reliable cash collection, modest annual raises, and a coverage cushion that survives shocks.

Pillar Three: It Survives Cycles

Operating cash flow has stayed above $4 billion every year for the last decade and reached $8.585 billion in 2025. Even in 2020, coverage of the distribution held at 1.51x. The debt load of $34.2 billion is structured for endurance, with a weighted average life of about 17 years, a 4.7% weighted average cost, and 95% fixed-rate. With a beta of 0.469, the units do not whipsaw with the broader market. Growth is already funded, with $5.3 billion in major projects under construction and Permian natural gas and NGL production projected to grow at 1.6 times the rate of crude.

Where It Underperforms, and Why It Does Not Matter

During commodity bull cycles, when E&P drillers run higher on spot prices, Enterprise lags. Revenue actually fell to $14.386 billion in Q1 2026 from $15.42 billion a year earlier on lower NGL prices, and the quarter included $98 million in mark-to-market derivative losses. None of that changes the forever thesis. A 20-year holder is paid in tollbooth cash flow that keeps arriving when drillers blow up, when oil drops to $55.44, and when it surges to $114.58.

Enterprise Products Partners is built for long-term ownership rather than short-term trading.