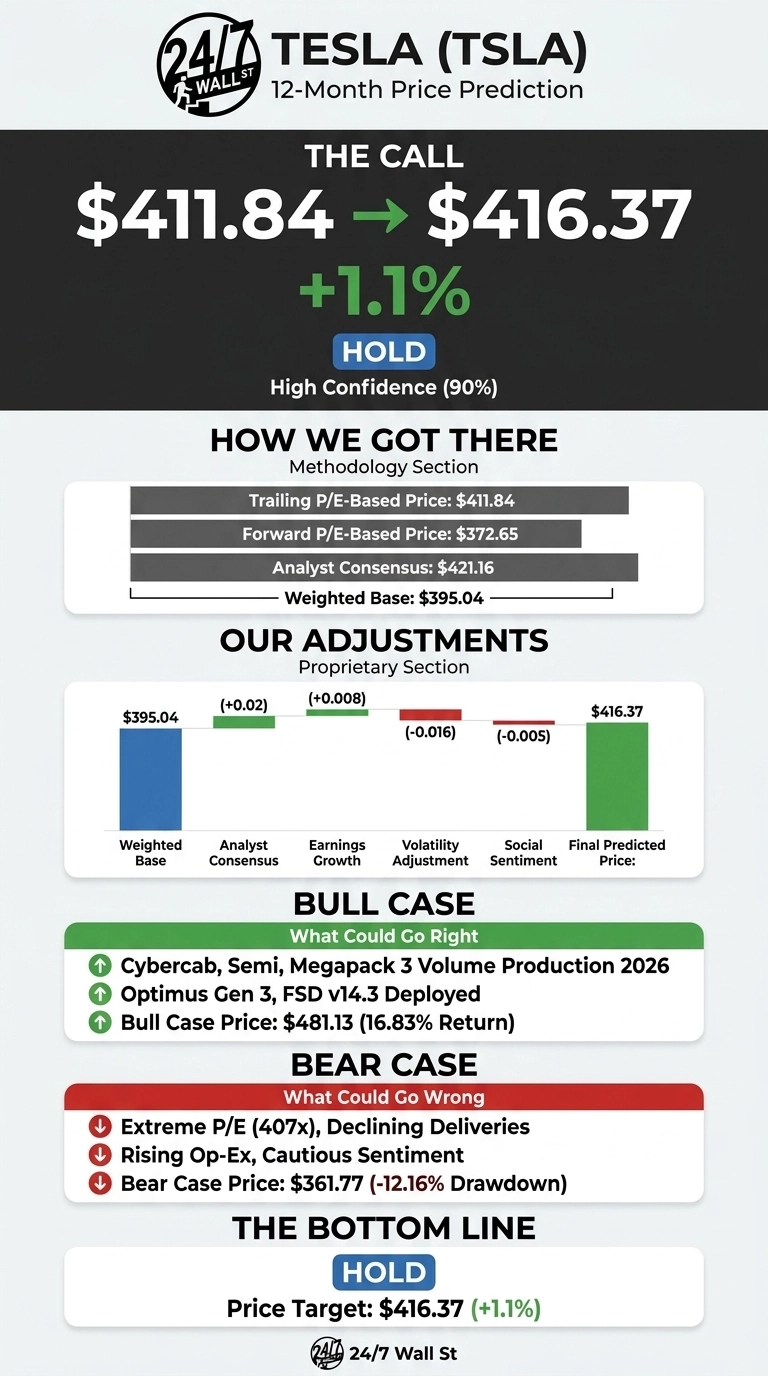

Our 24/7 Wall St. price target for Tesla (NASDAQ:TSLA | TSLA Price Prediction) is $416.37, modestly above where the stock trades today. With shares at $411.84, the implied move is roughly 1.1% over the next 12 months. That puts Tesla in hold territory by our model, with a confidence level of 90%. The setup is measured: after a year that included a 27.26% one-year gain, near-term reward looks balanced against risk.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $411.84 |

| 24/7 Wall St. Price Target | $416.37 |

| Upside | 1.1% |

| Recommendation | HOLD |

| Confidence Level | 90% |

A Choppy First Half Sets the Stage

Tesla is down 8.42% year to date and 5.5% over the past month, though shares popped 8.46% on June 29 alone. The stock sits roughly 16% below its 52-week high of $498.83 and well above the $288.77 low.

Q1 2026 was a real turn: revenue of $22.39B grew 15.8% YoY, non-GAAP EPS came in at $0.41 versus a $0.36 estimate, and auto gross margin expanded to 21.1% from 16.2%. Services revenue grew 42% and free cash flow more than doubled to $1.44B. That reset the narrative after a soft FY2025, when revenue fell 2.93% and net income dropped 46.79%.

The Case for $480+

Bulls have a real shot to break the model. Our internal bull-case scenario points to $481.13 over 12 months, a 16.83% return.

The catalysts are concrete: Cybercab, Tesla Semi, and Megapack 3 all targeting 2026 volume production; Optimus Gen 3 unveiling in Q1 with stated capacity of 1M robots per year at Fremont and 10M at the Texas Gigafactory; FSD v14.3 deployed in April; and Robotaxi expansion to Dallas and Houston with unsupervised rides.

The $2B SpaceX equity tie-up and the chip-fab partnership at Gigafactory Texas add a strategic kicker. The Street’s average target sits at $421.16, with 23 Buy ratings.

The Risks Worth Watching

The bear scenario takes Tesla to $361.77, a 12.16% drawdown. Valuation is the headline risk at 407x earnings against a 4.59% operating margin. FY2025 vehicle deliveries fell 9%, Q4 deliveries dropped 16%, and inventory days rose to 27 from 22.

Operating expenses jumped 37-50% YoY on AI R&D and the CEO award. Bulls would argue that op-ex surge reflects investment in Optimus, Dojo 3, and AI5 that should pay off over multiple years, and that the Q1 26 margin recovery suggests the auto cycle has turned.

Still, 7 Sell ratings exist, insider activity skews to net selling, and prediction-market sentiment turned down 18.58 points in seven days.

Hold for Now

The 24/7 Wall St. price target of $416.37 implies hold at 90% confidence. The factor tipping the scale is the gap between fundamentals and price: Q1 momentum is real, but valuation already prices in flawless execution on robotaxi, Optimus, and energy.

The bull case strengthens if FSD wins regulatory clearance in China or the EU at scale and Q2 deliveries clear 475,000 units. The thesis weakens if auto margins compress again or Optimus slips past Q4 2026.

Tesla Price Prediction 2026-2030

Extending our model with current growth trajectories and reasonable multiple compression on the AI/robotaxi optionality, here is where the 24/7 Wall St. price target points over five years.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $416 |

| 2027 | $432 |

| 2028 | $449 |

| 2029 | $465 |

| 2030 | $482 |

These projections assume Tesla keeps executing on Cybercab, Optimus, and energy storage. A material acceleration in robotaxi monetization could push the 2030 path toward the $629.88 bull case, while a stalled FSD rollout could drag toward the $374.15 bear path.

Contact [email protected] for any questions or corrections.