Altria has become a magnet for income-focused capital this year, with the stock climbing 32.55% year-to-date as retirees hunt for inflation hedges while the Fed has cut its target rate to 3.75%. Altria (NYSE:MO | MO Price Prediction) sells Marlboro, Copenhagen, Skoal, on! nicotine pouches and NJOY e-vapor, and its smokeable engine just posted a 65.1% operating margin. The question is whether the dividend is actually as bulletproof as the bulls claim.

Dividend Snapshot

| Metric | Value |

|---|---|

| Annual Dividend | $4.24 per share |

| Dividend Yield | 5.73% |

| Consecutive Years of Increases | 60 increases in 56 years |

| Most Recent Increase | 3.9% (August 2025) |

| Aristocrat-Class Status | Yes (commonly recognized) |

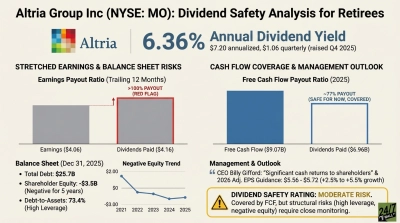

Payout Ratios Leave Real Room Despite Volume Drag

Altria earned $5.42 in adjusted diluted EPS for 2025 and pays $4.24 annually, putting the earnings payout ratio at 78.2%. That is elevated by general standards but normal for a mature tobacco operator. Cash coverage is what matters here. The company paid $7.0 billion in dividends in 2025 against operating income of $9.899 billion, with capex of only $175 to $225 million.

| Metric | TTM Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | 78.2% | Elevated but Manageable |

| FCF Payout Ratio (est.) | ~76% | Healthy |

| 2026 EPS Guidance | $5.56 to $5.72 | Lowers Payout Further |

Negative Equity Reflects Buybacks, Not Distress Signals

Altria carries negative shareholders’ equity of $3.211 billion, a function of years of aggressive buybacks. EBITDA of $15.79 billion against the debt load keeps leverage manageable, and cash sits at $3.531 billion. The smokeable margin expansion to 65.1% confirms pricing power is offsetting the 5% industry volume decline.

20 Years of Increases and Counting

| Year | Annual Dividend |

|---|---|

| 2026 (run rate) | $4.24 |

| 2025 | $4.16 |

| 2024 | $4.08 |

| 2023 | $3.92 |

| 2022 | $3.68 |

| 2021 | $3.52 |

The 5-year dividend CAGR runs roughly 3.8%, in line with management’s mid-single-digit growth target through 2028.

Management’s Tone: Confident, Not Hedging

CEO Billy Gifford told investors on the Q1 2026 call: “We delivered a strong start to the year, growing adjusted diluted EPS by 7.3% in the first quarter. Our highly cash-generative businesses supported significant returns to shareholders through dividends and share repurchases.” On the prior call, he noted the company “returned $8 billion to shareholders through dividends and share repurchases combined” in 2025. That tone reflects confidence.

Verdict: Safe, With Pricing Power Doing the Heavy Lifting

Dividend Safety Rating: Safe. The 78% earnings payout is the only number I would flag, but 2026 guidance of $5.56 to $5.72 mechanically eases it. I would be comfortable owning Altria for income if you accept that pricing power drives the thesis. I would be cautious if Marlboro share losses accelerate past current declines or if regulators target menthol and nicotine caps more aggressively. For now, the dividend looks intact.

Contact [email protected] for any questions or corrections.