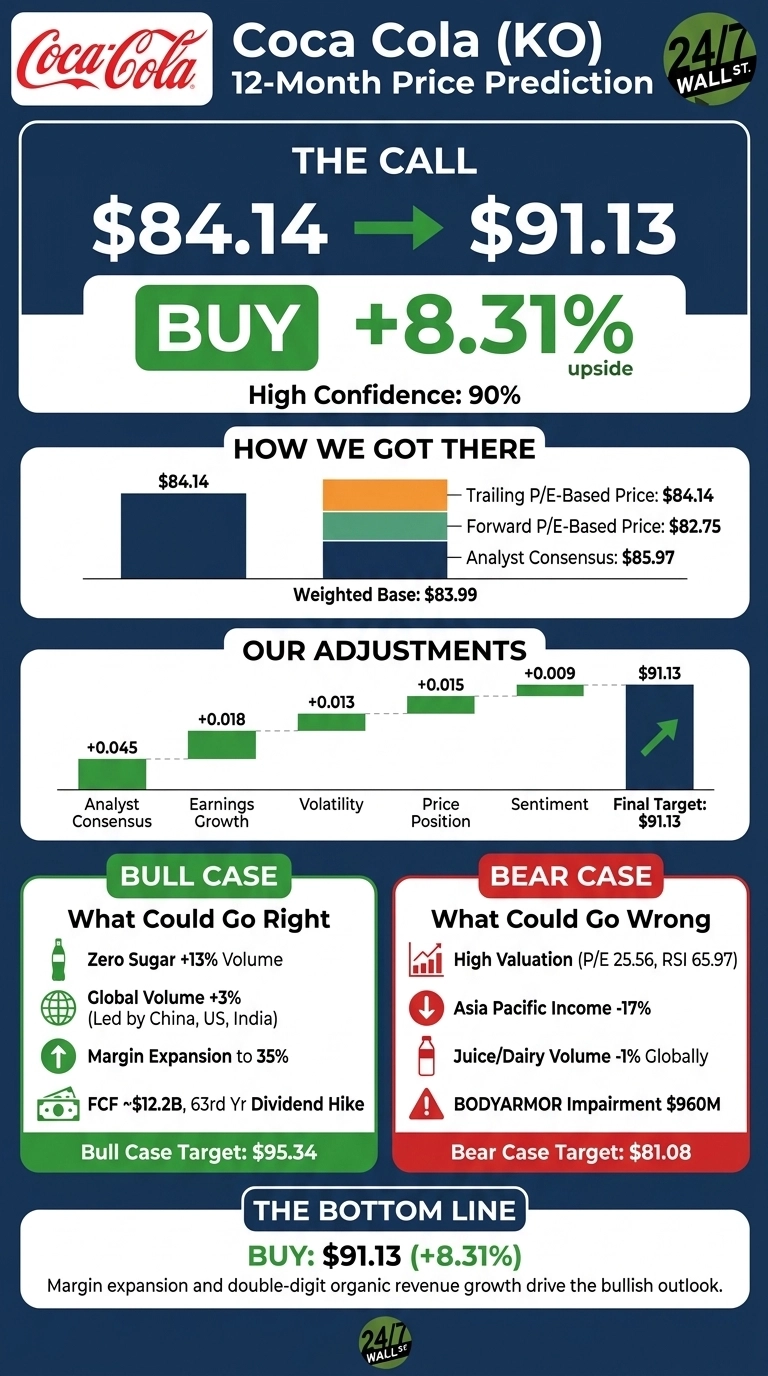

My Coca-Cola (NYSE:KO | KO Price Prediction) call is straightforward. After a 21.97% year-to-date run that has pushed shares to their 52-week high of $84.14, momentum, fundamentals, and defensive positioning all point higher. Our 24/7 Wall St. price target for Coca-Cola is $91.13, implying 8.31% upside over the next 12 months. The recommendation is buy with high confidence at 90%.

| Metric | Value |

|---|---|

| Current Price | $84.14 |

| 24/7 Wall St. Price Target | $91.13 |

| Upside | 8.31% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Momentum Run Backed by a Guidance Raise

Coca-Cola is up 4.63% in the last week, 8.01% over the past month, and 22.04% over the trailing year.

The catalyst was the Q1 2026 report on April 28, 2026, when KO delivered EPS of $0.86 against a $0.8123 estimate and revenue of $12.47B, up 12.1% YoY. Organic revenue grew 10%, operating margin expanded to 35% from 32.9%, and management raised full-year comparable EPS growth guidance to 8% to 9% off the $3 2025 base.

New CEO Henrique Braun said the quarter reflected our unwavering focus on staying close to the consumer, executing locally and managing complexity. That was the fourth consecutive EPS beat.

Why Bulls See a Breakout Above $95

The bull case rests on portfolio categories compounding. Coca-Cola Zero Sugar grew volume 13% across every geographic segment in Q1, and global unit case volume rose 3%, led by China, the US, and India. All five reporting segments grew: North America +12%, EMEA +13%, Latin America +14%, Asia Pacific +6%, and Bottling Investments +12%.

Free cash flow guidance sits at $12.2B, funding 63rd consecutive year of dividend increases and a $5.2B remaining buyback authorization.

Consumer staples demand is holding, with US food services spending climbing to $1,538.3B in May 2026. Analyst consensus sits at $85.97, and our bull case projects $95.34 if margin expansion and Zero Sugar momentum persist.

The Risks Worth Watching

The bear case starts with valuation. KO trades at a 25x trailing multiple and a weekly RSI of 65.97, elevated after February’s 78.19 overbought peak. Asia Pacific comparable currency-neutral operating income declined 17%, juice and dairy volumes fell 1% globally, and Q4 2025 absorbed a $960M BODYARMOR impairment.

Insider activity has skewed toward selling across 32 recent transactions. Bulls counter that the BODYARMOR charge is non-cash and that Q4’s operating income drop was distorted by the African bottling reclassification, a one-off geographic accounting shift. Our bear case lands at $81.08, a mild -3.63% pullback rather than a drawdown.

The Bottom Line

My 24/7 Wall St. price target for KO is $91.13, buy, with 90% confidence. The scale-tipping factor is margin expansion pairing with organic revenue growth in the double digits, a rare combination for a mega-cap staple.

The setup strengthens if Zero Sugar volume growth stays above 10% and Q2 confirms the Q1 margin trajectory. I’d stay on the sidelines if RSI pushes above 70 without a corresponding EPS revision higher, since that would signal a multiple-driven rally rather than earnings-driven upside.

Coca-Cola Price Prediction 2026 to 2030

Looking further out, here is where our model projects KO could trade, assuming mid-single-digit organic revenue growth and steady multiple support from the consumer defensive bid.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $91.13 |

| 2027 | $97 |

| 2028 | $104 |

| 2029 | $110 |

| 2030 | $115 |

These projections assume Coca-Cola continues executing on Zero Sugar, price/mix, and international volume growth. Meaningful upside or downside could come from currency swings, the IRS tax litigation outcome, or a step-change in category mix from acquisitions.

Contact [email protected] for any questions or corrections.