I keep buying Alphabet (NASDAQ:GOOG | GOOG Price Prediction) because every quarter it hands me a new reason to. This is the one AI position where the receipts arrive on schedule, the moat is visible in the numbers, and the price still lets me add without holding my nose. I am compounding into a business that is now printing cash on a scale most companies will never approach.

Google owns the front door to the internet and is turning that traffic into an AI toll road while the rest of the industry is still building on-ramps.

When Sundar Pichai said on the Q1 call, “We are genuinely differentiated. We’re unique in the market because of our vertically optimized AI stack”, I read it as a description of the income statement. Custom TPUs, Gemini models, Cloud, Search, YouTube, Android, Waymo. One company, one stack, one cash engine.

The numbers that keep my finger on the buy button

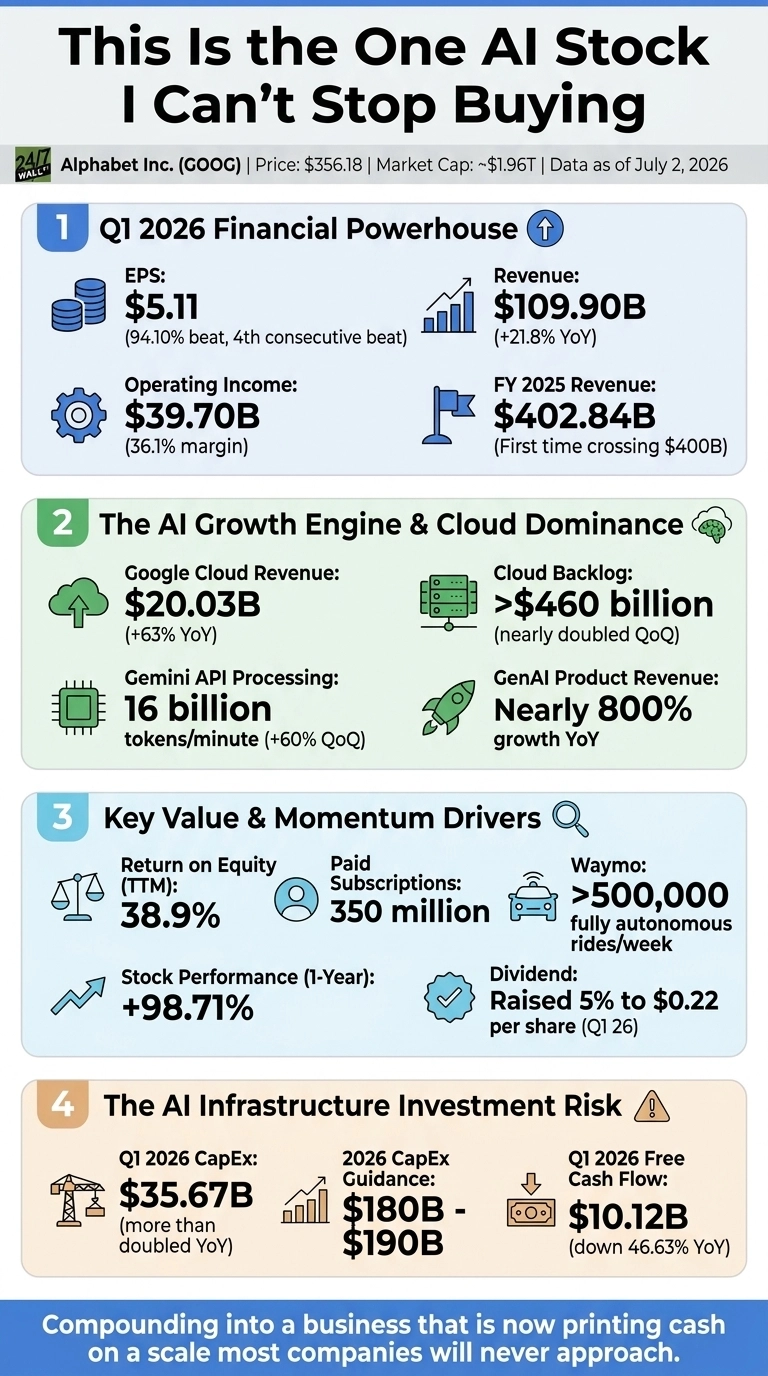

Q1 2026 EPS came in at $5.11 against a $2.63 consensus, a 94.10% beat and the fourth consecutive EPS beat. Revenue hit $109.90 billion, up 21.8% year over year, with operating income at $39.70 billion and a 36.1% operating margin. Full year 2025 revenue crossed $402.84 billion for the first time. Return on equity sits at 38.9%.

Google Cloud revenue grew 63% year over year to $20.03 billion, and backlog nearly doubled quarter on quarter to over $460 billion. Cloud operating margin expanded from 17.8% a year ago to 32.9%.

Gemini is running at 16 billion tokens per minute through the API, up from 10 billion the prior quarter, and GenAI product revenue grew nearly 800% year over year. This is enterprise money landing.

Alphabet raised its quarterly dividend 5% to $0.22 per share, sits on $38.06 billion in cash against $478.75 billion in shareholders’ equity, and trades at a trailing P/E of 27 and a forward P/E of 25. Fifty-eight buy ratings, zero sells.

The stock is up 98.71% over the past year and 13.65% year to date, and I am still adding.

The risk I am not glossing over

The real concern is capital intensity. CapEx more than doubled year over year to $35.67 billion in Q1, and management now guides 2026 CapEx to $180 billion to $190 billion, with 2027 expected to increase further. Free cash flow fell 46.63% year over year to $10.12 billion. If AI demand cools before those data centers are paid for, the return on that spend gets ugly.

That $460 billion Cloud backlog is a signed answer to the demand question. CFO Anat Ashkenazi called it “unprecedented internal and external demand for AI compute resources”, and Pichai flatly said the company is “compute constrained”. When customers are lined up and you cannot ship fast enough, spending is a moat.

Search revenue still grew 19% to $60.40 billion, paid subscriptions crossed 350 million, and Waymo is doing over 500,000 fully autonomous rides per week. I own a search company, a cloud company, an AI lab, a video platform, and a robotaxi operator inside one ticker at a market multiple. That is why I cannot stop buying.

Contact [email protected] for any questions or corrections.