Meta Platforms (NASDAQ: META | META Price Prediction) and Alphabet (NASDAQ: GOOG) both reported Q1 results on April 29, 2026, and the results frame a clear question. Both companies are pouring tens of billions into AI infrastructure, both ride enormous ad engines, yet only one is showing investors a second growth pillar already paying off.

Ads Power Meta. Cloud Powers Alphabet.

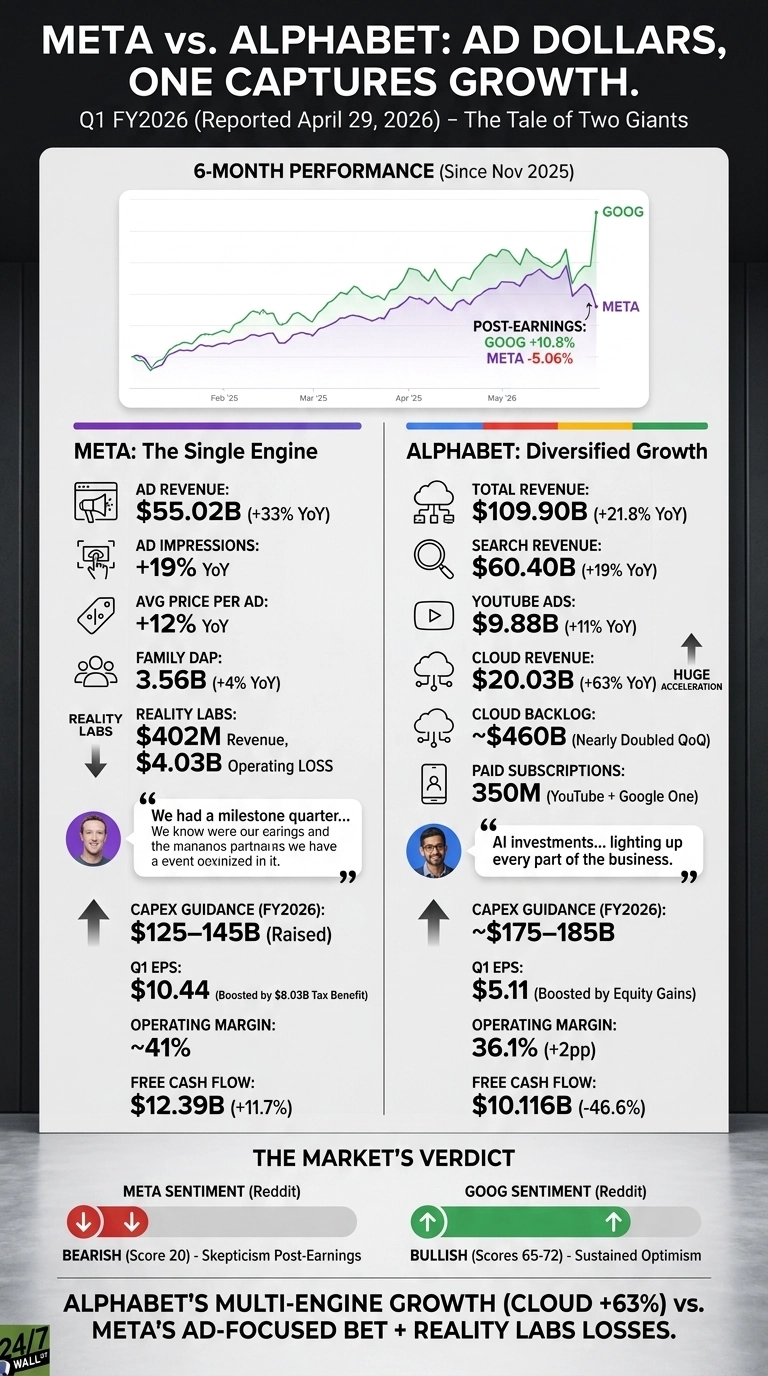

Meta’s ad machine looked extraordinary. Advertising revenue hit $55.02 billion, up 33%, with ad impressions +19% and price per ad +12%. Mark Zuckerberg called it “a milestone quarter” tied to the first model from Meta Superintelligence Labs. Reality Labs, however, posted a $4.03 billion operating loss on just $402 million of revenue. That math still stings.

Alphabet showed a wider hand. Search grew 19% to $60.40 billion, YouTube ads added 11%, and Google Cloud surged 63% to $20.03 billion with backlog nearly doubling to over $460 billion. Sundar Pichai said “AI investments and full stack approach are lighting up every part of the business.”

| Driver | Meta | Alphabet |

| Revenue | $56.31B (+33.1%) | $109.90B (+21.8%) |

| Operating Margin | ~41% | 36.1% |

| 2026 CapEx Guide | $125-145B | ~$175-185B |

One Bet, or Many?

Meta is doubling down on a single engine. The CapEx range got raised by $10 billion, citing higher component pricing and data center costs. Free cash flow still grew, but only 11.74% to $12.39 billion. The EPS headline of $10.44 was inflated by a $8.03 billion tax benefit worth $3.13 per share.

Alphabet is monetizing AI through paying customers. 350 million paid subscriptions across YouTube and Google One, Gemini Enterprise paid users +40% QoQ, and Gemini APIs now process 16 billion tokens per minute, up 60%. Waymo crossed 500,000 autonomous rides per week. The cost? CapEx more than doubled to $35.67 billion and free cash flow fell 46.6%.

The Market Is Already Voting

Since the reports, GOOG is up 10.8% while META is down 5.06%. Reddit sentiment mirrors that gap, with wallstreetbets turning bearish on Meta (score 20) post-earnings while GOOG sustained bullish scores of 65 to 72. I will be watching whether Meta’s Q2 guide of $58 to $61 billion can quiet doubts about Reality Labs cash burn.

Why I Lean Toward Alphabet Right Now

For my own read, Alphabet looks like the better balance. A P/E near 16 for a business growing Cloud at 63% with a $460 billion backlog feels mispriced.

Meta still offers the cleaner pure-ad-leverage profile for investors who believe Superintelligence Labs ships product. Meta’s setup looks more compelling once Reality Labs losses narrow or CapEx clarity improves. For now, Alphabet is capturing the growth its rival is paying for.

Contact [email protected] for any questions or corrections.