Coca-Cola (NYSE:KO | KO Price Prediction) is the defensive name every retirement account seems to want to own right now, rallying 20.26% year to date on consistent earnings beats and a flight to quality inside consumer staples. Yet the multiple has run ahead of the fundamentals, and there is a better regulated alternative hiding in plain sight.

Coca-Cola Is Steady

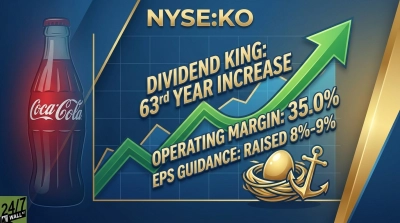

Shares closed at $82.96, sitting right against a 52-week high of $84.54. That leaves Coca-Cola trading at roughly 26 times forward earnings with a dividend yield of only 2.53%, well beneath the 4.49% yield on a 10-year Treasury. For that premium multiple, holders are underwriting management guidance of 4% to 5% organic revenue growth and 8% to 9% comparable EPS growth in 2026, a story further complicated by a 4% headwind from divestitures, unresolved IRS tax litigation, and a $960 million BODYARMOR impairment in Q4 2025.

The 63-year dividend streak is impressive. So is the fact that the stock is priced like the next decade will look exactly like the last one. When a defensive name yields less than cash and trades at a growth multiple, the margin of safety is gone.

Why Duke Energy Is The Better Retirement Trade

Duke Energy (NYSE:DUK) trades at 19 times earnings with a 3.3% dividend yield, up a comparatively modest 9.63% year to date. This is the setup a seasoned income investor wants: a regulated cash machine the crowd has not chased yet. Three specific reasons to redirect the defensive allocation here.

1. Contracted growth locked in through 2030. Duke’s $103 billion five-year capital plan is the largest regulated capital plan in the industry, driving 9.6% earnings base growth through 2030. Management guides to 5% to 7% EPS growth through 2030 and expects to earn in the top half of that range beginning in 2028. That growth flows through rate base expansion, not global case volumes or currency swings.

2. The AI data center tailwind is already contracted. Duke has secured 7.6 GW of economic development projects under Electric Service Agreements. Its Sun-belt regulated footprint across the Carolinas, Florida, Indiana, Ohio, and Kentucky sits in the heart of the U.S. data center corridor. CEO Harry Sideris explicitly credits “contracted demand from AI and advanced manufacturing” as a structural driver of the 2026 outlook, and management is doing this while keeping rates below the national average and rate changes below inflation.

3. Four straight beats and a widening dividend. Duke has delivered four consecutive quarters of EPS beats. Q1 2026 adjusted EPS came in at $1.93 versus a $1.80 estimate, a 7.51% beat, on revenue of $9.18 billion that grew 11.3% year over year. The annualized dividend has climbed from $3.24 in 2015 to $4.24 in 2025, and the 2026 quarterly payout was raised to $1.065. Sell-side price targets sit at $138.56, above the current $125.97 quote, while Coca-Cola trades near its consensus target of $85.97.

Retirement investors have been trained to reach for Coca-Cola every time the market gets nervous. This cycle, the crowd has already made that trade, and the multiple shows it. For income-focused investors comparing the two, Duke Energy offers the more compelling risk/reward on current metrics.

Contact [email protected] for any questions or corrections.