Marvell Technology has become one of the loudest AI infrastructure stories of the past twelve months, and the numbers back it up. Marvell Technology (NASDAQ:MRVL | MRVL Price Prediction) shares are up 186.61% year to date as custom XPU silicon, 800G/1.6T optics, and 51.2T Ethernet switches ride the hyperscaler capex wave.

CEO Matt Murphy told investors the company is seeing “exceptional AI-related bookings” and just raised the fiscal 2027 and 2028 outlook. The question I want to answer is simple. Can this stock hit $400 by 2027?

What’s Holding Marvell Back Right Now

Despite the parabolic YTD move, shares have cooled off. Marvell is down 8.85% in the last month and 0.82% on the week, sitting 24% below the 52-week high of $329.88.

The pullback lines up with two real concerns. First, customer concentration risk is real. Data center now accounts for 76% of revenue, and hyperscaler vertical integration is a genuine overhang.

Second, a beta of 2.197 means every macro wobble hits harder here than in a broad index. Add in net insider selling across 129 recent transactions, and the profit-taking narrative writes itself. I do not think that changes the multi-year thesis, but it explains why the tape looks tired.

Wall Street Sees 4% Upside. Our Model Says 16%

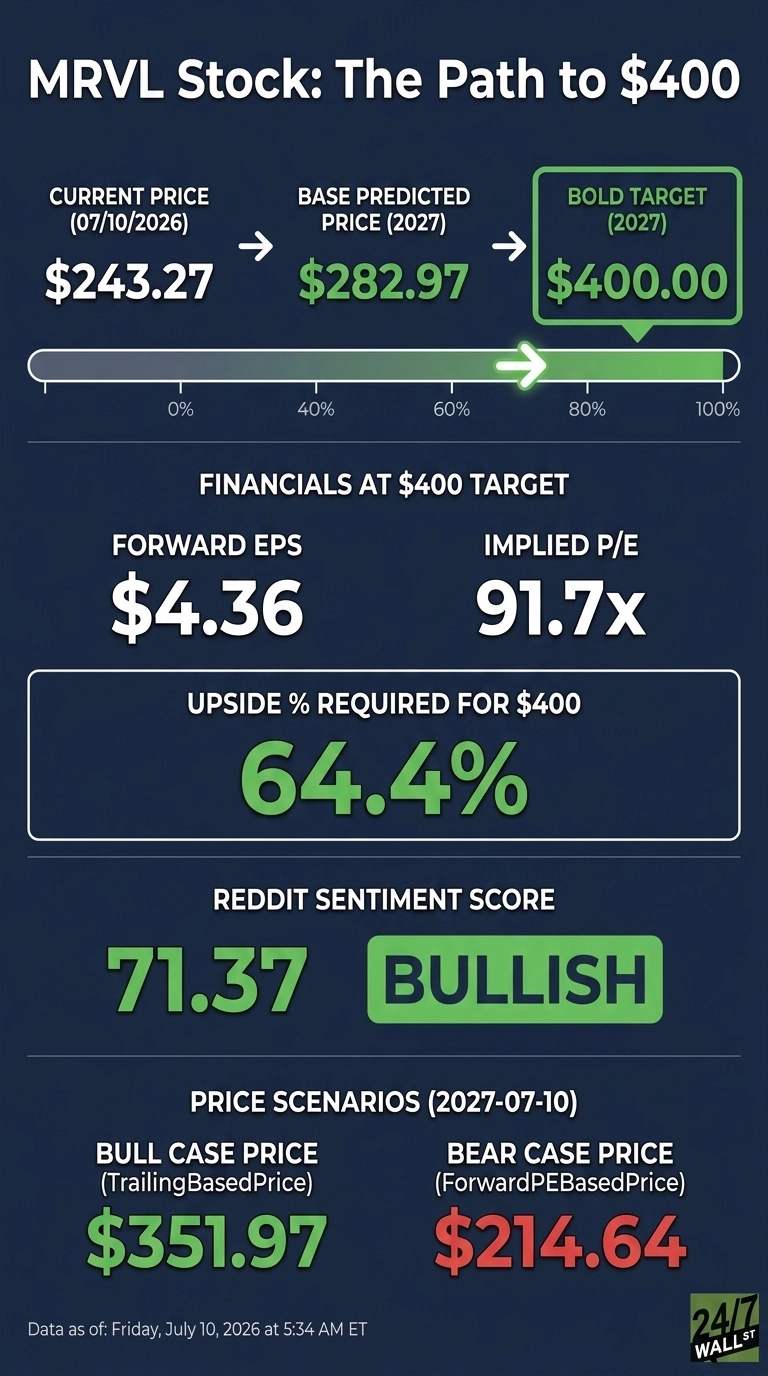

Consensus analyst target is $252.26, which is essentially where the stock trades today. The rating breakdown is heavily bullish: 7 Strong Buys, 31 Buys, 5 Holds, and 1 Strong Sell, an 86% bullish share. Our own base case is $282.97 with 90% confidence, implying 16.32% upside, and the bull case runs to $351.97.

The sell side is likely behind the curve. Analysts anchored their targets before management raised the fiscal 2028 outlook. If bookings acceleration is real, the current consensus is a lagging indicator. That is the gap I am trying to price.

The Path to $400 Per Share

Reaching $400 from today’s price of $243.27 would require a gain of 64.4%. With forward EPS of $4.36, a price of $400 implies a forward P/E of 92x. Our base case of $282.97 already implies 80x, meaning the bold target requires roughly 12x of additional multiple expansion.

Is that achievable? The forward P/E compression story only works if EPS growth outruns expectations. Q1 FY2027 revenue grew 27.6% YoY to $2.418 billion, and Q2 is guided to $2.70 billion, roughly 35% YoY. Free cash flow jumped 126.8% to $483.1 million.

Murphy said flatly, “We expect revenue growth to continue accelerating each quarter throughout fiscal 2027.” The Celestial AI and XConn deals close the interconnect gap, and the 247Factor adjustment of 1.104, driven by 1.15 sector momentum and 86% analyst bullishness, tells you the setup is aligned. The main risk is a hyperscaler pausing custom silicon orders.

Where Marvell Trades Today vs Its Earnings Power

At $243.27 against forward EPS of $4.36, Marvell trades at roughly 56x forward earnings. That is a premium multiple, priced for durable AI capex growth.

The stock sits between the 52-week low of $61.32 and high of $329.88, and the 10-year return of 2,517.21% shows what compounding at AI-adjacent margins can do. Fiscal 2026 non-GAAP EPS grew 81% to $2.84. If that operating leverage continues, today’s multiple compresses fast.

Is $400 Realistic? Here’s My Take

My read: $400 by 2027 is a stretch, but it is not a fantasy.

It requires a 64.4% gain, driven by three things going right: fiscal 2028 guidance rising again on custom XPU wins, gross margin holding near 59%, and no hyperscaler pulling in-house. What would derail it is a broader semiconductor spending pause. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Marvell could reach $400 in 2027.

Contact [email protected] for any questions or corrections.