Marvell Technology (NASDAQ:MRVL | MRVL Price Prediction) has been one of the strongest performers in the 2026 AI infrastructure trade, rising from $84.88 at year-end to $276.70. The question now is whether the run has more left.

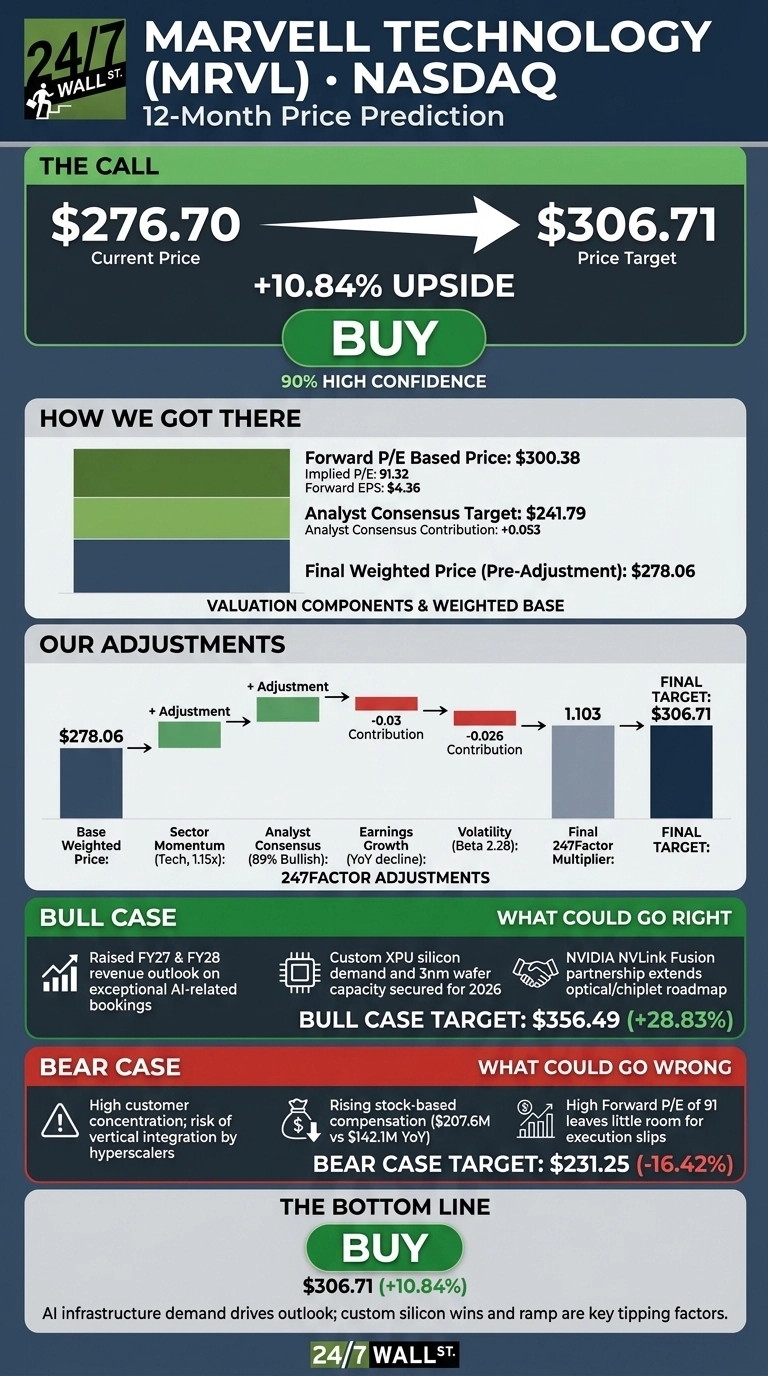

Based on our proprietary model, the 24/7 Wall St. price target for Marvell is $306.71, implying 10.84% upside over the next twelve months. Our recommendation is buy, with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $276.70 |

| 24/7 Wall St. Price Target | $306.71 |

| Upside | 10.84% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $85 to $276 in Six Months

Marvell has gained 225.99% year to date and 268.9% over the past year, with a 40.94% move in the last month alone.

The catalyst was the Q1 FY2027 earnings report on May 27, 2026, when revenue of $2.417 billion grew 27.6% YoY and non-GAAP EPS hit $0.80. Data center revenue of $1.832 billion now represents 76% of the business.

CEO Matt Murphy raised the FY27 and FY28 outlook on what he called “exceptional AI-related bookings.” Shares pulled back 4.43% last week as profit-taking debates dominated Reddit threads.

Why Bulls See a Breakout to $356

Our bull case projects Marvell at $356.49 within a year, a 28.83% total return. The driver is custom XPU silicon. Murphy stated AI “now represents the majority of our data center revenue,” and the company has secured three-nanometer wafer and advanced packaging capacity for follow-on production in calendar 2026.

Q2 FY27 guidance calls for revenue of $2.70 billion, roughly 35% YoY growth, with EPS of $0.93. Recent acquisitions of Celestial AI and XConn Technologies, plus a partnership adding NVIDIA NVLink Fusion to the custom platform, extend the optical and chiplet roadmap. Free cash flow hit a record $483.1M, up 126.8% YoY.

The Risks Worth Watching

The bear case targets $231.25, a -16.42% drawdown. The forward P/E of 91 leaves little room for execution slips, and analyst consensus target sits at just $241.79, well below our model. Customer concentration is real, with hyperscalers driving the bulk of data center revenue and the risk that they vertically integrate silicon.

Insider activity has skewed toward selling across 114 recent transactions. Stock-based comp rose to $207.6M from $142.1M. That said, the GAAP net income drop reflects a one-time contingent consideration charge tied to acquisitions rather than an operational miss, and operating cash flow still hit a record $638.8M.

Marvell Price Prediction 2026 to 2030

The 24/7 Wall St. price target reflects a buy at our stated confidence level. The tipping factor is the FY27 and FY28 outlook raise, which signals booked demand.

The setup strengthens if the Q2 earnings report confirms data center revenue sustains strong YoY growth. I’d stay on the sidelines if hyperscaler capex commentary turns cautious or if a major custom XPU customer signals a second source. For now, the setup favors the bulls.

Looking further ahead, here is where our model projects Marvell could trade, assuming continued AI infrastructure spend and gradual multiple compression as growth normalizes.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $306.71 |

| 2030 | $400.58 |

These projections assume Marvell continues winning custom silicon sockets and ramping 1.6T optical interconnects. Significant upside or downside could come from hyperscaler capex shifts or trade restrictions on Chinese demand.

Contact [email protected] for any questions or corrections.