Few stocks have captured the AI infrastructure narrative like Marvell Technology (NASDAQ:MRVL | MRVL Price Prediction). After NVIDIA CEO Jensen Huang publicly called Marvell “the next trillion-dollar company,” the question shifted from whether the stock could rally to when the market cap crosses 13 digits. Our model provides a clear answer on near-term price and the long-term milestone.

The 24/7 Wall St. Price Target for Marvell

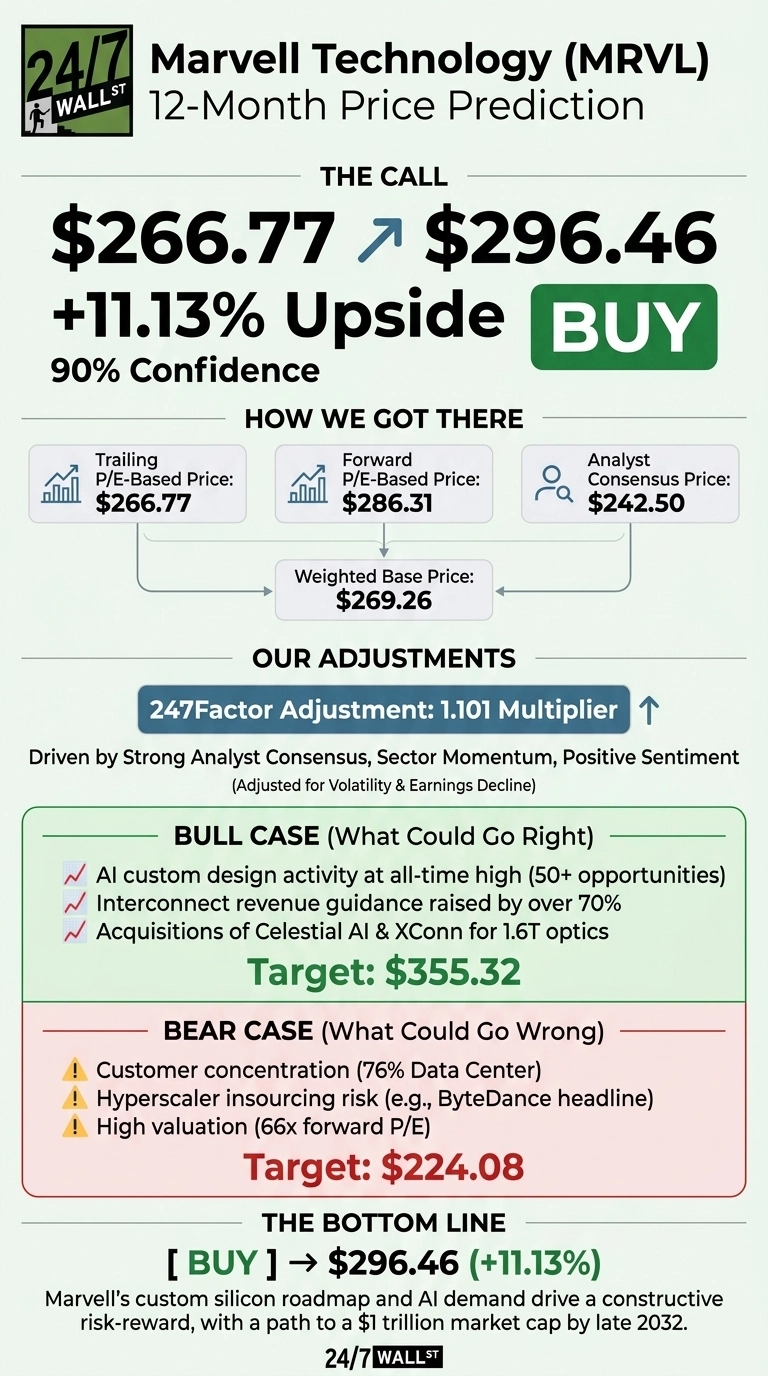

Marvell trades at $266.77 with a market cap of roughly $233.57 billion. Our 24/7 Wall St. price target points to $296.46 over the next 12 months, a buy rating with high confidence. Our model projects Marvell crosses the $1 trillion market cap line around December 31, 2032, implying a share price near $1,142.

| Metric | Value |

|---|---|

| Current Price | $266.77 |

| 24/7 Wall St. Price Target (12-mo) | $296.46 |

| Upside | 11.13% |

| Recommendation | BUY |

| Confidence Level | 90% |

| $1 Trillion Date Projection | December 31, 2032 |

From $79 to $266 in 12 Months

Marvell is one of the most explosive semiconductor stories of the cycle. Shares are up 234.49% over the past year and 214.29% year to date, with the stock tripling off the January 2026 low of $79.01. It sits 26% below the 52-week high of $329.88 after a 14.11% one-week pullback from $310.58.

Q1 FY2027 revenue hit $2.418 billion, up 27.6% year over year, with data center revenue of $1.83 billion, or 76% of the mix. CEO Matt Murphy guided Q2 to $2.7 billion at the midpoint, representing 35% year-over-year growth, and noted the company is “significantly raising Marvell’s revenue outlook for both fiscal 2027 and fiscal 2028.” S&P 500 inclusion took effect June 22, 2026, adding passive flows to the AI bid.

Why Bulls See a Breakout Ahead

The bull case centers on custom silicon. Murphy said AI custom design activity is at an all-time high, with more than 50 opportunities across over 10 customers. Custom chip revenue could exceed $10 billion by fiscal 2029, and interconnect guidance was raised by over 70%. Recent acquisitions of Celestial AI and XConn add photonic fabric and chiplet IP for 1.6T optics.

Wall Street is catching up. KeyBanc raised its target to $385, BofA went to $365, and Stifel moved to $350. KeyBanc flagged a bull case at $450. Cantor Fitzgerald analyst C.J. Muse raised the firm’s price target on Marvell to $300 from $220 and keeps a Neutral rating on the shares.

If revenue scales to $16.5 billion by 2028 as some models project, our bull-case 1-year price of $355.32 looks conservative.

The Risks Worth Watching

Forward P/E is 66x and trailing P/E is 92x, leaving no room for execution slippage. Data center represents 76% of sales with a 10% drop on June 9 tied to ByteDance ASIC headlines, showing how fast sentiment can shift on vertical integration fears.

GAAP net income fell 80.6% year over year in Q1, though this reflects a $331.8 million contingent consideration charge tied to the Celestial AI deal rather than ongoing operations. Our bear-case 1-year price is $224.08, a 16% drawdown.

Our Take on Marvell at $266

Our 24/7 Wall St. price target of $296.46 implies 11.13% upside with 90% confidence, and the $1 trillion milestone looks reachable by late 2032 if custom silicon ramps as guided.

The bull thesis strengthens if Q2 confirms the 35% growth trajectory and bookings stay at record pace. The thesis weakens if hyperscaler insourcing announcements escalate or forward P/E expands beyond 75x without matching upward revisions. On balance, the risk-reward setup leans constructive.

Marvell Price Projection 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $296 |

| 2027 | $340 |

| 2028 | $360 |

| 2029 | $375 |

| 2030 | $388 |

These projections assume Marvell executes on its custom XPU roadmap and optical interconnect leadership. Upside comes from broader hyperscaler design wins; downside centers on customer insourcing or AI capex slowdown.

Contact [email protected] for any questions or corrections.