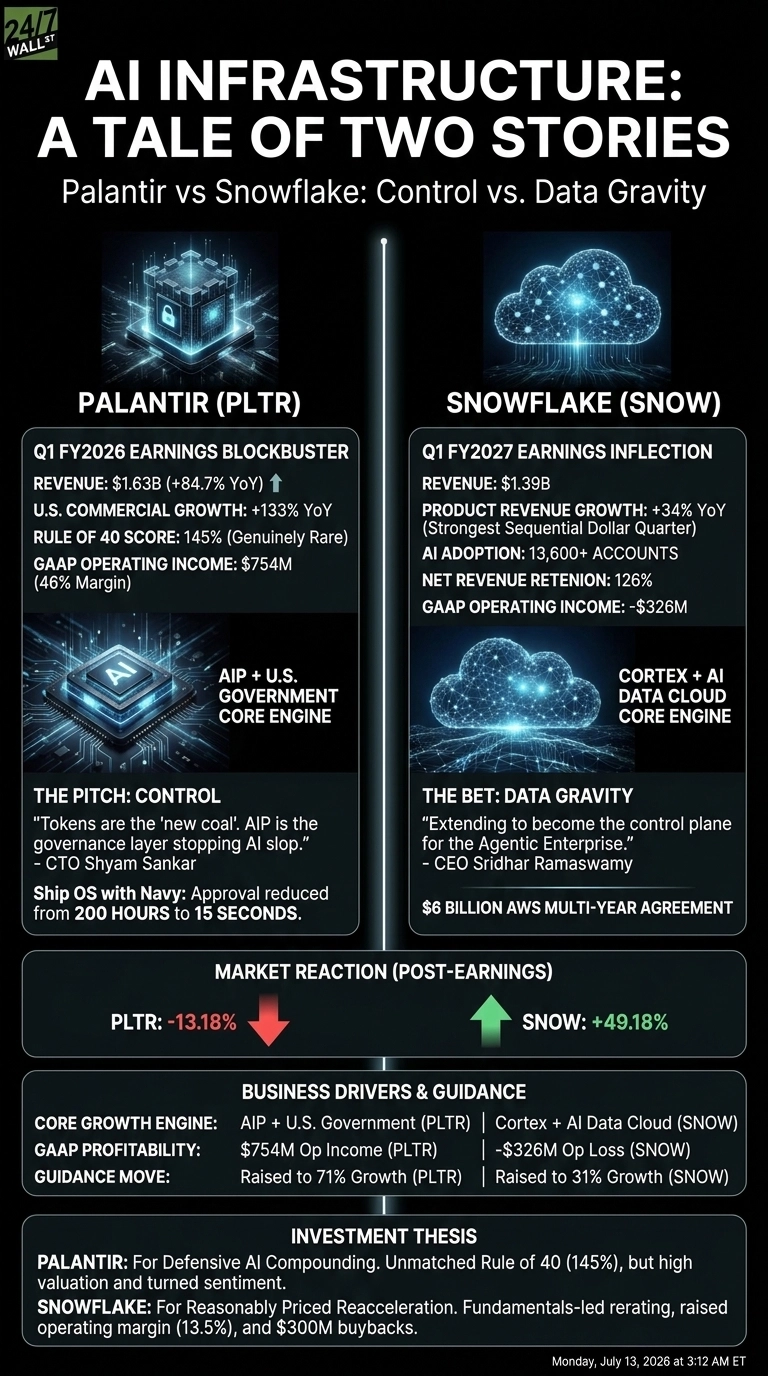

Palantir (NASDAQ:PLTR | PLTR Price Prediction) and Snowflake (NYSE:SNOW) both delivered blockbuster earnings reports this spring, and the results tell two very different AI stories.

Palantir reported 85% revenue growth anchored by defense and enterprise AIP wins. Snowflake countered with its strongest sequential dollar quarter ever, powered by Cortex adoption. One is scaling profits fast. The other is scaling consumption faster.

Government Muscle Lifts Palantir. Cortex Lifts Snowflake.

Palantir’s Q1 FY2026 landed with $1.63 billion in revenue and an adjusted EPS of $0.33, both comfortably ahead of the Street. U.S. commercial revenue jumped 133% to $595 million as AIP kept displacing legacy stacks. CEO Alex Karp told investors, “Palantir’s Rule of 40 score has soared to 145%.” That is a genuinely rare number in enterprise software.

Snowflake’s Q1 FY2027 came in at $1.39 billion in revenue, with product revenue up 34% year over year and non-GAAP EPS of $0.39. Sridhar Ramaswamy framed the quarter as an inflection: “With Cortex Code and Snowflake Intelligence, we are extending from the trusted foundation for enterprise data and context to become the control plane for the Agentic Enterprise.” Roughly 13,600 accounts now touch Snowflake AI features.

| Business Driver | Palantir | Snowflake |

| Core Growth Engine | AIP + U.S. Government | Cortex + AI Data Cloud |

| GAAP Profitability | $754M operating income | -$326M operating loss |

| Guidance Move | Raised to 71% growth | Raised to 31% growth |

An Ontology Bet Versus a Data Gravity Bet

Palantir’s pitch is control. CTO Shyam Sankar called tokens “the new coal” and positioned AIP as the governance layer that stops what Karp bluntly calls AI slop. The Ship OS work with the Navy reportedly cut a manufacturing bill of materials approval from 200 hours to 15 seconds. That is the kind of receipt defense buyers reward with sticky contracts.

Snowflake’s bet is gravity. Data sits in the warehouse, so agents and models come to it. Ramaswamy has leaned into partnerships to reinforce that, including a $6 billion multi-year AWS agreement, a deepened OpenAI collaboration, and the pending Natoma acquisition for AI agent connectivity. Net revenue retention of 126% suggests existing customers keep spending more as workloads expand.

The market has noticed the split. Since its report, Palantir shares are down 13.18%, while Snowflake has climbed 49.18%. Valuation gravity is real, even for winners.

The Next Test Is Whether the Multiples Hold

For Palantir, I want to see whether U.S. commercial can keep printing triple-digit growth against a harder compare, and whether stock-based compensation of $201.6 million eases as headcount scales.

For Snowflake, the questions are GAAP losses, consumption variability, and whether Cortex Code and Intelligence convert to durable committed spend rather than experimental credits.

Why I Lean Toward Snowflake Right Now

Personally, I like Snowflake more here. The valuation reset over the past two years has been brutal, but the reacceleration to 34% product growth, a raised operating margin outlook of 13.5%, and $300 million in buybacks feel like a fundamentals-led rerating.

Palantir is an extraordinary business, and Karp is right that few peers can match a 145% Rule of 40. But shares still trade near a a large market cap, and Reddit sentiment has already turned, with one widely upvoted post calling it a “dying horse” just three weeks after earnings.

For readers focused on defensive AI compounding, Palantir screens well. For those tracking reasonably priced reacceleration, Snowflake is the more compelling story right now.

Contact [email protected] for any questions or corrections.