SanDisk (NASDAQ:SNDK | SNDK Price Prediction) and Micron Technology (NASDAQ:MU) both just delivered the kind of quarters that memory investors dream about.

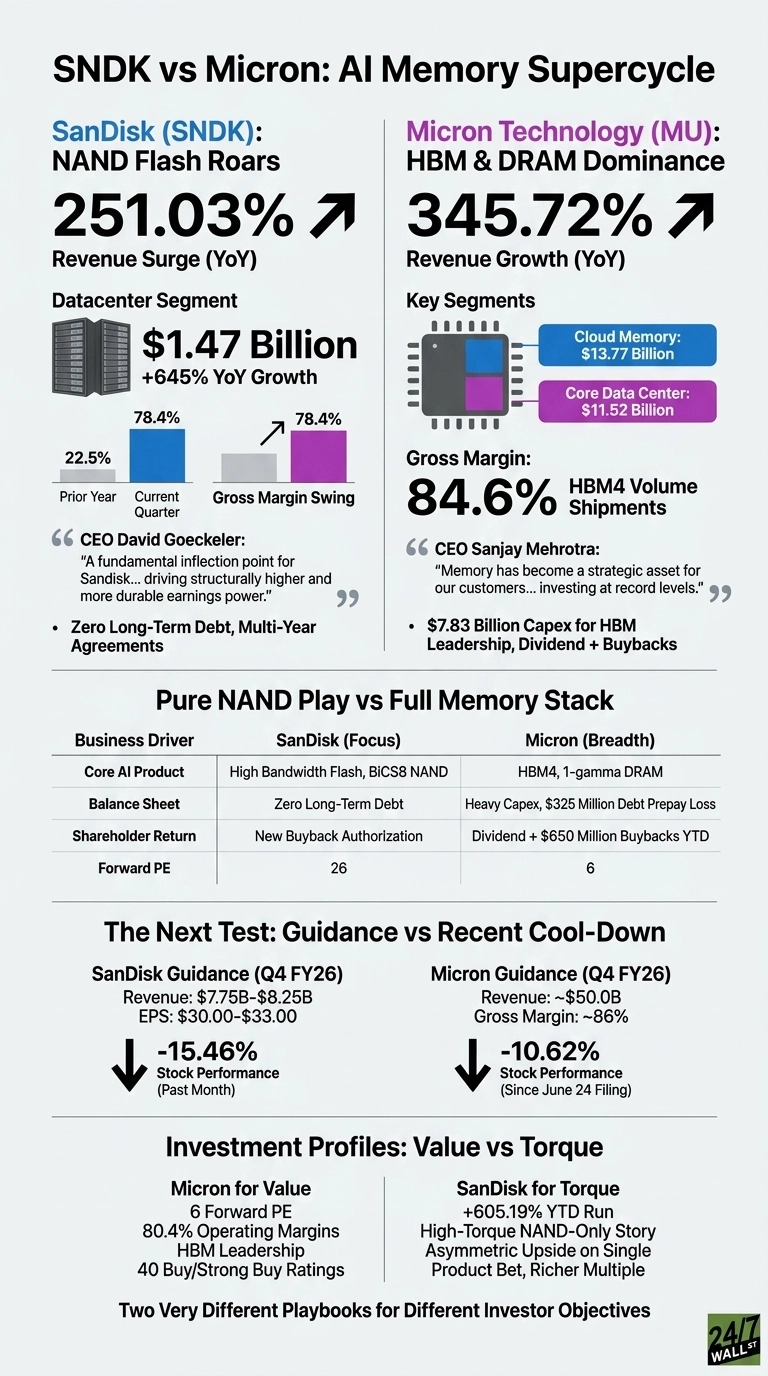

SanDisk posted a 251.03% revenue surge on NAND flash strength, while Micron rode HBM and DRAM to 345.72% growth. Two very different memory playbooks. One shared tailwind: AI infrastructure spending that refuses to slow down.

NAND Flash Roars for SanDisk. HBM Rewrites Micron’s Story.

SanDisk’s Datacenter segment did the heavy lifting, generating $1.47 billion at a jaw-dropping +645% year over year. Gross margin swung from 22.5% to 78.4% in a single year, which tells you pricing power has completely inverted.

CEO David Goeckeler framed it as “a fundamental inflection point for Sandisk”, pointing to five signed multi-year customer agreements and engagement with five hyperscalers. That is real backlog with contractual visibility.

Micron played a bigger board. Cloud Memory hit $13.77 billion, Core Data Center added $11.52 billion, and gross margin expanded to 84.6%. HBM4 is already shipping in high volume to the lead AI accelerator customer.

Sanjay Mehrotra said “memory has become a strategic asset for our customers”. The $7.83 billion quarterly capex bill is the price of holding that HBM crown.

Pure NAND Play Versus the Full Memory Stack

| Business Driver | SanDisk | Micron |

| Core AI Product | High Bandwidth Flash, BiCS8 NAND | HBM4, 1-gamma DRAM |

| Balance Sheet | Zero long-term debt | Heavy capex, $325 million debt prepay loss |

| Shareholder Return | New buyback authorization | Dividend plus $650 million buybacks YTD |

| Forward PE | 26 | 6 |

SanDisk is betting the farm on flash for AI inference workloads, where High Bandwidth Flash could cheapen memory-intensive model serving.

Micron is playing every position on the field: HBM for training, DDR5 for servers, LPDDR5X for phones, QLC SSDs up to 245TB, and even robotaxi automotive DRAM. Breadth is Micron’s moat. Focus is SanDisk’s.

The Next Test Is Whether Guidance Sticks

SanDisk guided Q4 revenue to $7.75 billion to $8.25 billion and EPS to $30 to $33. Micron pointed to $50 billion and roughly 86% gross margin. Yet both stocks have cooled after their earnings reports. SanDisk is down 15.46% over the past month, and Micron slipped 10.62% since its June 24 filing. That looks like digestion after a strong run.

I will be watching whether SanDisk can convert hyperscaler engagements into visible ramp guidance beyond Q4, and whether Micron’s HBM4E schedule for calendar 2027 holds against fierce Korean competition.

If you want a sense of how far the memory rerating could travel, our team’s Next Nvidia Playbook lays out the framework I keep returning to.

Micron for Value, SanDisk for Torque

On the numbers, Micron screens as the cleaner risk-reward. A 6 forward PE on a company with 80.4% operating margins and HBM leadership is difficult to argue with, and the 40 combined buy and strong-buy ratings back that up.

SanDisk is the higher-torque play. Its 605.19% year-to-date run reflects a NAND-only story that could still deliver if High Bandwidth Flash lands, but it trades at a much richer forward multiple.

Micron offers durability and cash return, while SanDisk offers asymmetric upside on a single product bet. The two profiles suit different investor objectives.

Contact [email protected] for any questions or corrections.