SanDisk’s ascent on the NASDAQ this year raises a key question: does the AI memory supercycle still have room to run, or has the easy money already been made?

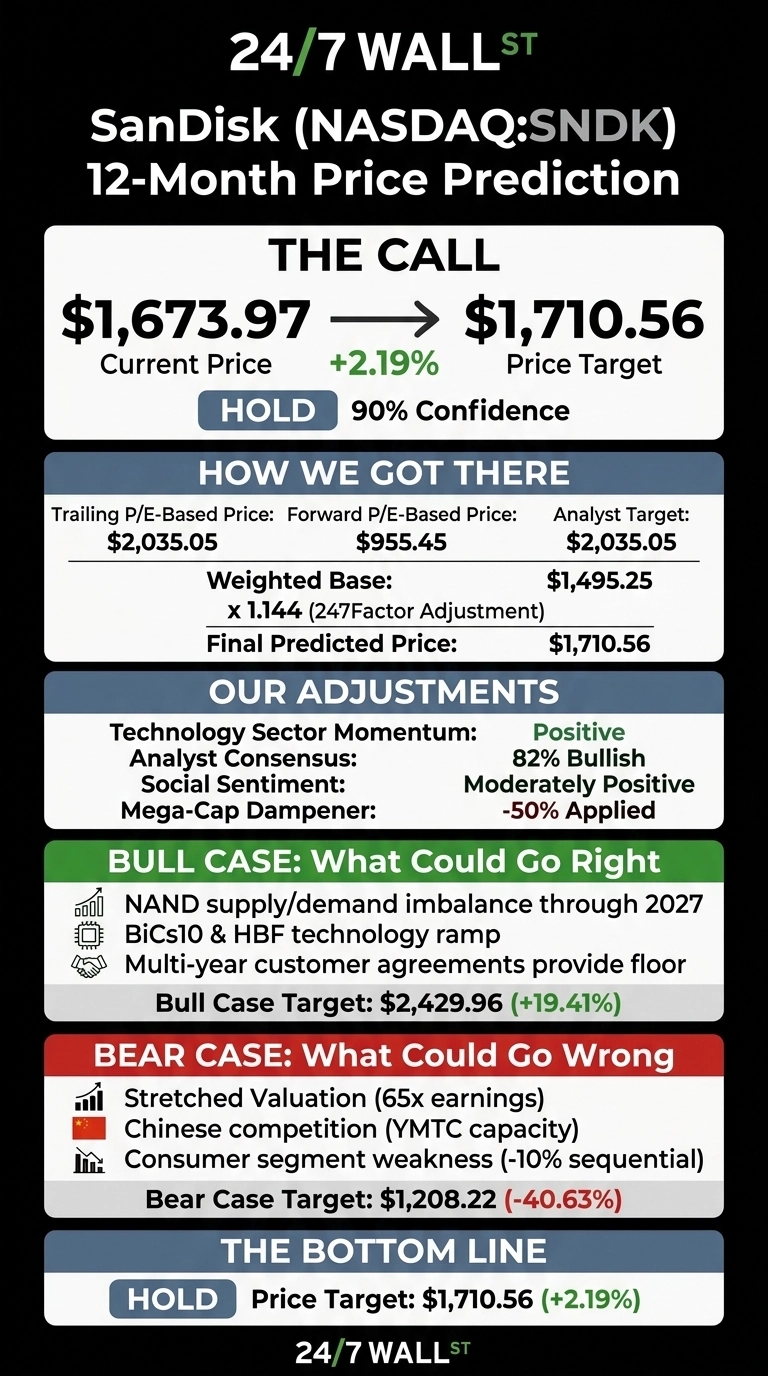

My 24/7 Wall St. price target for SanDisk (NASDAQ:SNDK | SNDK Price Prediction) is $1,710.56 over the next 12 months, against a current price of $1,673.97. That represents roughly 2% upside, meaning the model calls this stock fairly valued. My recommendation is hold with 90% confidence.

| Metric | Value |

|---|---|

| Current Price | $1,673.97 |

| 24/7 Wall St. Price Target | $1,710.56 |

| Upside | 2.19% |

| Recommendation | HOLD |

| Confidence Level | 90% |

From $40 to $2,000 in Under a Year

SNDK is up 605.19% since the December 31 close of $237.38, and 3,531.96% over one year. Recent momentum has softened, with the stock down 15.46% over the past month and 14% below the 52-week high of $2,354.39.

Fundamentals justify much of the re-rating. Q3 FY2026 revenue hit $5.95 billion, up 251.03% year over year, with Non-GAAP EPS of $23.41 against $14.66 consensus. Datacenter revenue surged 645% year over year to $1.467 billion.

Q4 guidance calls for $7.75 billion to $8.25 billion in revenue and Non-GAAP EPS of $30 to $33. Bernstein raised its target to $3,000 and Bank of America to $2,500, though an 8% pullback on July 13 tied to SK Hynix IPO concerns offset some gains.

The Case for $2,400 Plus

The bull case rests on supply dynamics. Bank of America argues the NAND supply/demand imbalance will continue through 2027, and Bernstein’s Mark Newman estimates new multi-year customer agreements provide a floor of 29 cents per gigabyte.

Five NBM agreements have been signed. If Q4 lands at guidance’s top and BiCS10 ramps into 2027, the bull trajectory points to $2,429.96, a 19.41% return. China Renaissance’s $3,169 target sits well above that.

What Could Break the Thesis

The bear case starts with valuation. SNDK trades at 65 times earnings, with forward-P/E math implying fair value nearer $955. Chinese competition from YMTC, a $29 billion SK Hynix listing that could siphon capital, and Consumer segment weakness down 10% sequentially all matter.

Insider selling has been steady, with the CLO selling 600 shares on July 1. Bulls counter that these sales occurred under a Rule 10b5-1 plan and Consumer weakness reflects a deliberate mix shift, not lost demand. The bear-case model lands at $1,208.22, or 40.63% downside.

How SanDisk Stacks Up Against Micron and Seagate

Micron Technology (NASDAQ:MU) is the cleanest comparable, with overlapping NAND exposure and similar AI-driven margin dynamics. Micron posted fiscal Q3 revenue of $41.46 billion (+345.7% YoY) and Non-GAAP EPS of $25.11, with GAAP gross margin at 84.6%. That is a bigger, more diversified memory business trading at a lower multiple, making SanDisk’s premium look aggressive on scale but reasonable on pure-play NAND leverage.

Seagate Technology (NASDAQ:STX) offers the storage counterpoint. Seagate’s fiscal Q3 revenue rose 44.1% to $3.11 billion with Non-GAAP EPS of $4.10, riding HAMR-based Mozaic drives into hyperscaler racks. Seagate proves AI storage demand is broad-based, supporting SanDisk’s floor but capping how much of the AI storage wallet SNDK can capture.

Against these peers, my 24/7 Wall St. price target of $1,710.56 looks reasonable.

SanDisk Price Prediction 2026-2030

My 24/7 Wall St. price target is $1,710.56 with a hold rating and 90% confidence. I’d be a buyer if Q4 lands at guidance’s top and NBM agreements expand past five. I’d stay on the sidelines if China’s YMTC accelerates capacity or Consumer stays negative. For now, risk-reward is balanced.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $1,710.56 |

| 2027 | $1,650.00 |

| 2028 | $1,600.00 |

| 2029 | $1,590.00 |

| 2030 | $1,583.68 |

These projections assume SanDisk executes its datacenter mix shift and NAND pricing holds through 2027. Significant upside or downside could result from a China-led supply shock or accelerated HBF adoption for AI inference.

Contact [email protected] for any questions or corrections.