Two of the market’s most talked-about AI plays sit on very different footings this summer. Palantir (NASDAQ:PLTR | PLTR Price Prediction) has cooled after a torrid run, while AMD (NASDAQ:AMD) has ripped higher on accelerating Data Center demand.

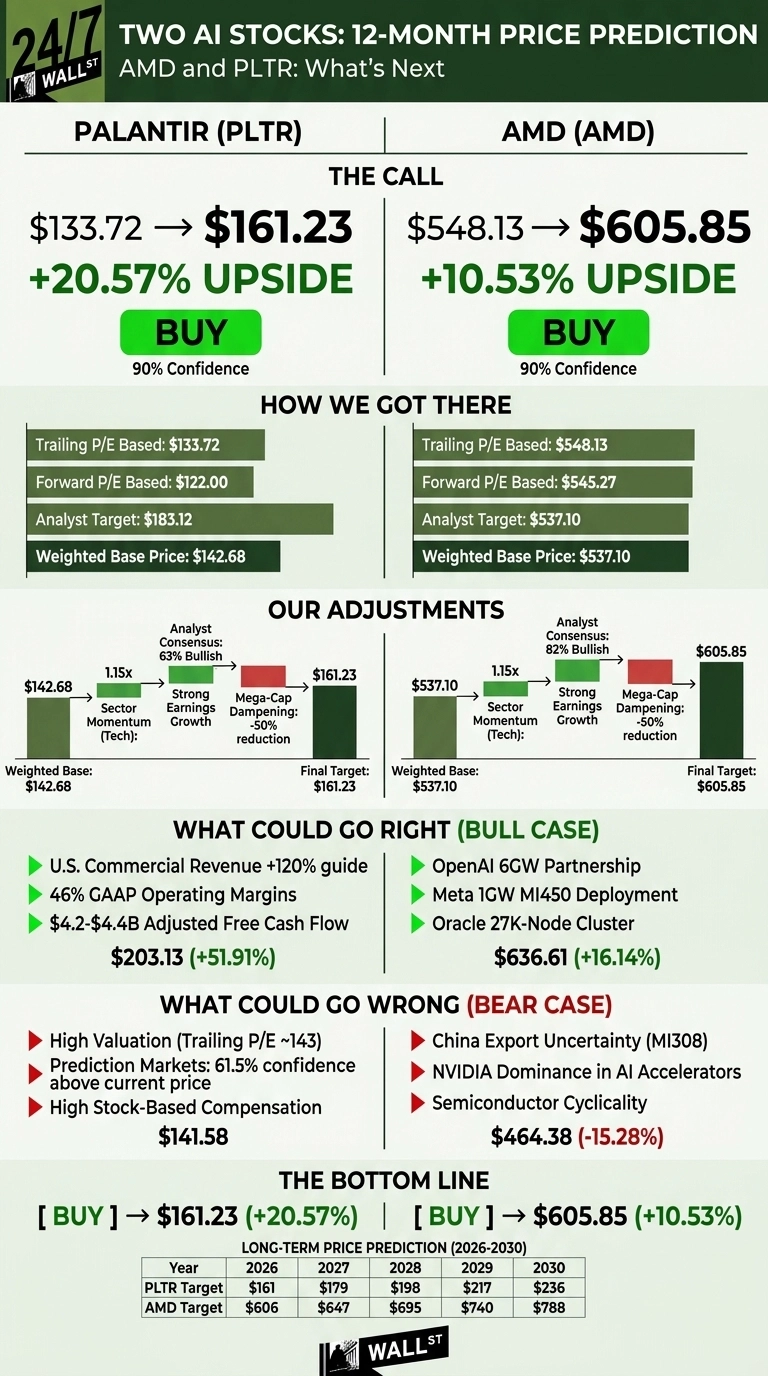

Our proprietary model has a buy on both, but the upside profiles differ meaningfully. Our 24/7 Wall St. price target for PLTR is $161.23, implying 20.57% upside from $133.72. For AMD, the 24/7 Wall St. price target is $605.85, or 10.53% above $548.13. Confidence on both at 90%.

| Metric | PLTR | AMD |

|---|---|---|

| Current Price | $133.72 | $548.13 |

| 24/7 Wall St. Price Target | $161.23 | $605.85 |

| Upside | 20.57% | 10.53% |

| Recommendation | BUY | BUY |

| Confidence | 90% | 90% |

How Palantir and AMD Got Here in 2026

Palantir is down 24.77% year to date and 10.35% over one year, well off its 52-week high of $207.52. Q1 2026 revenue hit $1.63 billion, up 84.7% YoY, with adjusted EPS of $0.33 beating estimates for the eighth straight quarter. CEO Alex Karp raised full-year guidance to 71% growth and touted a Rule of 40 score of 145%.

AMD is the opposite: up 155.94% YTD and 274.82% over one year. Q1 2026 revenue reached $10.25 billion (+37.85%), with Data Center contributing $5.78 billion (+57%). Q2 guidance calls for roughly $11.2 billion.

The Bull Case for Both AI Names

PLTR bulls point to the $3.22 billion U.S. Commercial revenue guide (+120%), 46% GAAP operating margins, and $4.2 to $4.4 billion in projected adjusted free cash flow. Our bull-case one-year target is $203.13, a 51.91% return.

AMD bulls cite hard commitments: OpenAI’s 6GW deployment, Meta’s 1GW MI450 rollout, and Oracle’s 27,000-node cluster. Our AMD bull case reaches $636.61, or 16.14%.

What Could Go Wrong

For Palantir, valuation is the elephant. A trailing P/E near 143 leaves no cushion, and Polymarket traders assign only 61.5% odds to closing above the current level this week. Our bear case sits at $141.58. Bulls counter that high stock-based compensation ($201.6 million in Q1) reflects growth-stage hiring.

AMD’s downside is dominated by China export uncertainty on MI308 and NVIDIA’s grip on the AI accelerator market. Our AMD bear case is $464.38, a 15.28% loss. Wall Street is bullish on the stock. Rosenblatt raised the firm’s price target on AMD to $665 from $490 and keeps a Buy rating on the shares while UBS analyst Timothy Arcuri raised the price target to $700 from $670 and keeps a Buy rating.

How PLTR and AMD Stack Up Against NVIDIA and Snowflake

NVIDIA (NASDAQ:NVDA) is the natural yardstick for AMD. NVIDIA posted Q1 FY27 revenue of $81.6 billion (+85.2%), and trades at a P/E of roughly 43. AMD’s 185 trailing multiple makes our AMD target look aggressive on absolute valuation but reasonable given AMD’s earnings ramp is still early.

Snowflake (NYSE:SNOW) is the closer read on PLTR. Snowflake grew Q1 FY27 revenue 33.5% to $1.39 billion with a 126% net retention rate, yet trades at a market cap under $100 billion versus Palantir’s roughly $311 billion. Palantir’s premium is earned by faster growth and 46% margins, making our $161.23 target appropriate.

Our Verdict on PLTR and AMD

Our 24/7 Wall St. price target model is constructive on both: $161.23 on PLTR (Buy, 90% confidence) and $605.85 on AMD (Buy, 90% confidence).

The PLTR thesis strengthens if U.S. Commercial keeps compounding above 120%. The AMD thesis weakens if MI450 customer forecasts slip or China restrictions tighten.

| Year | PLTR Target | AMD Target |

|---|---|---|

| 2026 | $161 | $606 |

| 2027 | $179 | $647 |

| 2028 | $198 | $695 |

| 2029 | $217 | $740 |

| 2030 | $236 | $788 |

These projections assume both companies execute on current AI-driven growth trajectories. Meaningful upside or downside could come from a China export-control resolution for AMD or sustained triple-digit U.S. Commercial growth at Palantir.

Contact [email protected] for any questions or corrections.