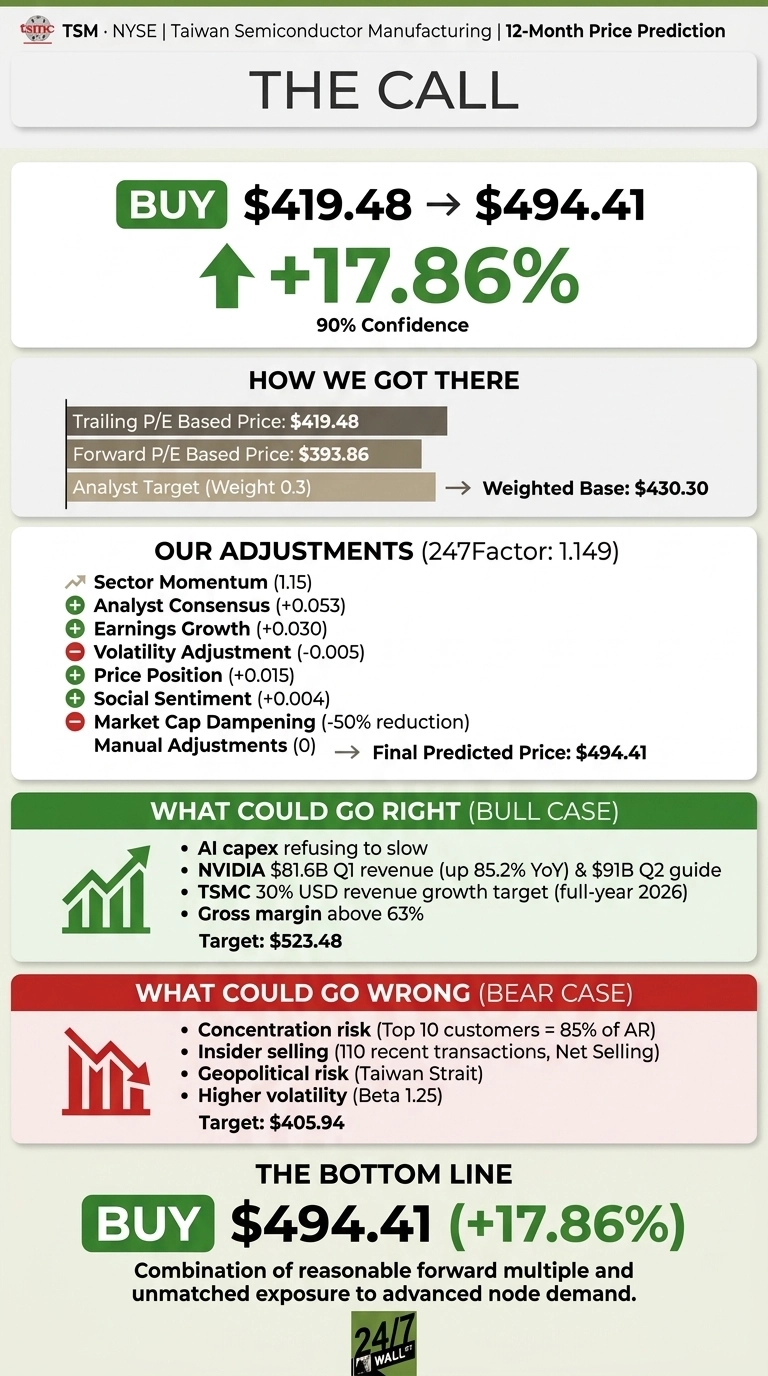

Taiwan Semiconductor Manufacturing (NYSE:TSM | TSM Price Prediction) trades at $419.48 heading into the July 16, 2026 earnings release, down 4.97% over the past month despite June 2026 revenue jumping 67.9% year over year.

Our 24/7 Wall St. price target for TSMC is $494.41, implying 17.86% upside over the next 12 months. The recommendation is buy with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $419.48 |

| 24/7 Wall St. Price Target | $494.41 |

| Upside | 17.86% |

| Recommendation | BUY |

| Confidence | 90% |

The Setup Heading Into Q2 Earnings

TSMC has rallied 78.95% over the past year and 38.73% year to date, powered by AI infrastructure demand from customers like NVIDIA. The stock sits 4% below its 52-week high of $479. The pullback comes as investors take profits ahead of the Q2 earnings report, with consensus at EPS of $3.89 and revenue near NT$1.26 trillion.

Monthly filings show the momentum. First-half 2026 revenue reached NT$2,404.48 billion, up 35.6% YoY. Q4 2025 delivered gross margin of 62.3% and operating margin of 54%, both exceeding guidance. Advanced nodes at 7nm and below now account for 77% of wafer revenue, with 3nm alone contributing 28%.

Why Bulls See $525 or Higher

The bull case rests on AI capex refusing to slow. NVIDIA reported $81.6 billion in Q1 FY2027 revenue, up 85.2% YoY and guided to $91 billion in Q2. Jensen Huang called AI factory buildout “the largest infrastructure expansion in human history.”

Bank of America Securities maintained its Buy rating citing cloud AI demand into 2026 while Susquehanna raised the firm’s price target on TSMC to $600 from $575 and keeps a Positive rating on the shares. If TSMC hits 30% USD revenue growth target for full-year 2026 and holds gross margin above 63%, the bull scenario points to $523.48.

What Could Go Wrong

Concentration risk is the primary concern. Top 10 customers represent 85% of accounts receivable, so any hyperscaler pullback would hit hard. Insider selling activity across 110 recent transactions is a contrarian flag, though routine at foreign filers. Geopolitical risk around Taiwan remains the tail scenario the model cannot fully price. The bear case lands at $405.94, a 3.23% drawdown.

How TSMC Stacks Up Against NVIDIA and Intel

NVIDIA (NASDAQ:NVDA) is the demand engine behind TSMC’s advanced node story. NVIDIA trades at P/E of 43x with 71.07% gross margin. TSMC captures the manufacturing economics without customer concentration, at a much lower 27x forward multiple. That gap makes our $494 target look conservative given the shared demand curve.

Intel (NASDAQ:INTC) is the closest foundry competitor. Intel carries market cap of $517.6 billion with negative trailing earnings and gross margin of 34.77%. TSMC’s operating margin sits at 58.1%, nearly 60 percentage points ahead. The peer set validates the TSMC price target.

| Company | Forward P/E | Gross Margin |

|---|---|---|

| TSMC | 27x | 62.3% |

| NVIDIA | 43x | 71.1% |

| Intel | N/M | 34.8% |

TSMC Price Prediction 2026-2030

Our 24/7 Wall St. price target of $494.41 is a buy call at 90% confidence. The key factor is the combination of a reasonable forward multiple and unmatched exposure to advanced node demand.

The bull thesis strengthens if Q2 earnings confirm gross margin above 63% and management reiterates the 30% USD revenue growth target. The thesis weakens if Taiwan Strait headlines escalate or hyperscaler capex signals soften. For a broader look at AI infrastructure winners beyond chipmakers, see 7 Stocks Powering the AI Boom (That Aren’t Chipmakers).

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $447.99 |

| 2027 | $494.41 |

| 2028 | $565 |

| 2029 | $630 |

| 2030 | $702.38 |

These projections assume TSMC executes on 2024-2029 revenue CAGR target near 25% and holds gross margin above 56% through the cycle. Upside or downside will come from AI capex trajectory and cross-strait geopolitics.

Contact [email protected] for any questions or corrections.