Coca-Cola (NYSE:KO | KO Price Prediction) is having one of its best runs in years. Shares are up 22.13% year to date, Q1 organic revenue grew 10%, and Coca-Cola Zero Sugar volume jumped 13% across every segment.

Yet the stock trades near its 52-week high of $85.68 and analysts peg fair value at $86.81. Can this Dividend King push to $105 by 2028?

Why Coca-Cola Shares Aren’t Ripping Higher

Coca-Cola is a slow-growth compounder in a market obsessed with AI capex. With a beta of 0.349, the stock barely moves on macro noise. JP Morgan’s 2026 outlook warns that “traditional value sectors like energy and consumer staples may continue to struggle” as capital flows toward AI enablers.

Near-term momentum is muted. Shares gained just 1.55% over the past week and 2.64% over the past month. The pending sale of Coca-Cola Beverages Africa is expected in the second half of 2026, and Q1 Asia Pacific operating income fell 17% on unfavorable mix.

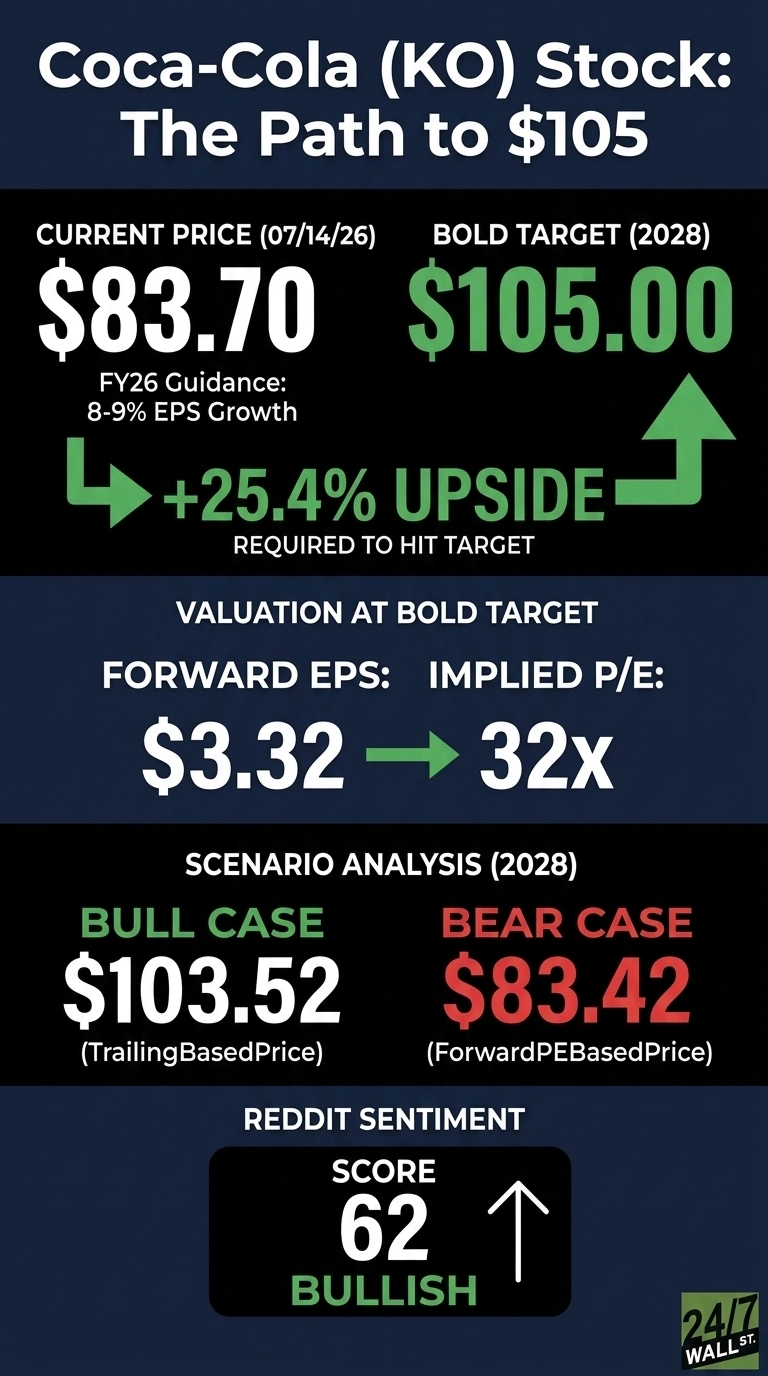

Wall Street Sees 4% Upside. Our Model Sees More

Wall Street’s consensus target of $86.81 implies single-digit upside from $83.70. Ratings break down as 7 Strong Buy, 12 Buy, 5 Hold, 0 Sell, and 1 Strong Sell, with 76% bullish sentiment.

Our 2028 base case sits at $99.95, with a bull case of $103.52 and confidence rated 0.9 (high). Wall Street is anchoring on last year’s flat performance and ignoring Q1 results: EPS beat by 5.87%, revenue grew 12.1% year over year, and management raised comparable EPS growth guidance to 8-9%.

The Path to $105 Per Share

Reaching $105 from $83.70 requires a 25.4% gain. Over two years that annualizes to roughly 12%, well within reason for a stock that has returned 73.64% over five years.

With forward EPS of $3.32, a $105 price implies a forward P/E of 32x. Our base case of $99.95 already implies 27x, so $105 needs about 5x of additional multiple expansion.

EPS growth must keep compounding. Management guided 2026 comparable EPS growth to 8-9% off a $3 base. If they hit 9% again in 2027 and 2028, forward EPS approaches $3.90 to $4.00, pulling the required multiple toward 26x.

CEO Henrique Braun said the team is “motivated by the opportunity to build on the company’s great foundation.” The primary risk is FX and the Africa divestiture creating a bigger revenue drag than expected.

Where Coca-Cola Trades Today vs Its Earnings Power

At $83.70 against forward EPS of $3.32, KO trades at roughly 25x forward earnings. That is defensible for a staple growing EPS at 8-9% with a 63rd consecutive dividend increase and $5.2B in buyback authorization remaining. Shares sit near the $85.68 high and well off the $64.04 low. Over 10 years the stock has returned 152.34%.

Is $105 Realistic?

Reaching $105 requires a 25.4% gain.

Three things need to break right: EPS compounds at the high end of guidance through 2028, the Africa divestiture doesn’t become a bigger drag than expected, and staples sentiment firms as investors rotate out of AI. A stronger dollar squeezing translated earnings derails it. We’ve outlined the blueprint for how Coca-Cola could reach $105 in 2028.

Contact [email protected] for any questions or corrections.