Ahead of Alphabet’s Q2 2026 earnings report, Bank of America has struck a bullish tone, and our proprietary model largely agrees. Alphabet (NASDAQ:GOOG | GOOG Price Prediction) has already returned 102.77% over the past year, and the setup into next week’s report looks unusually clean.

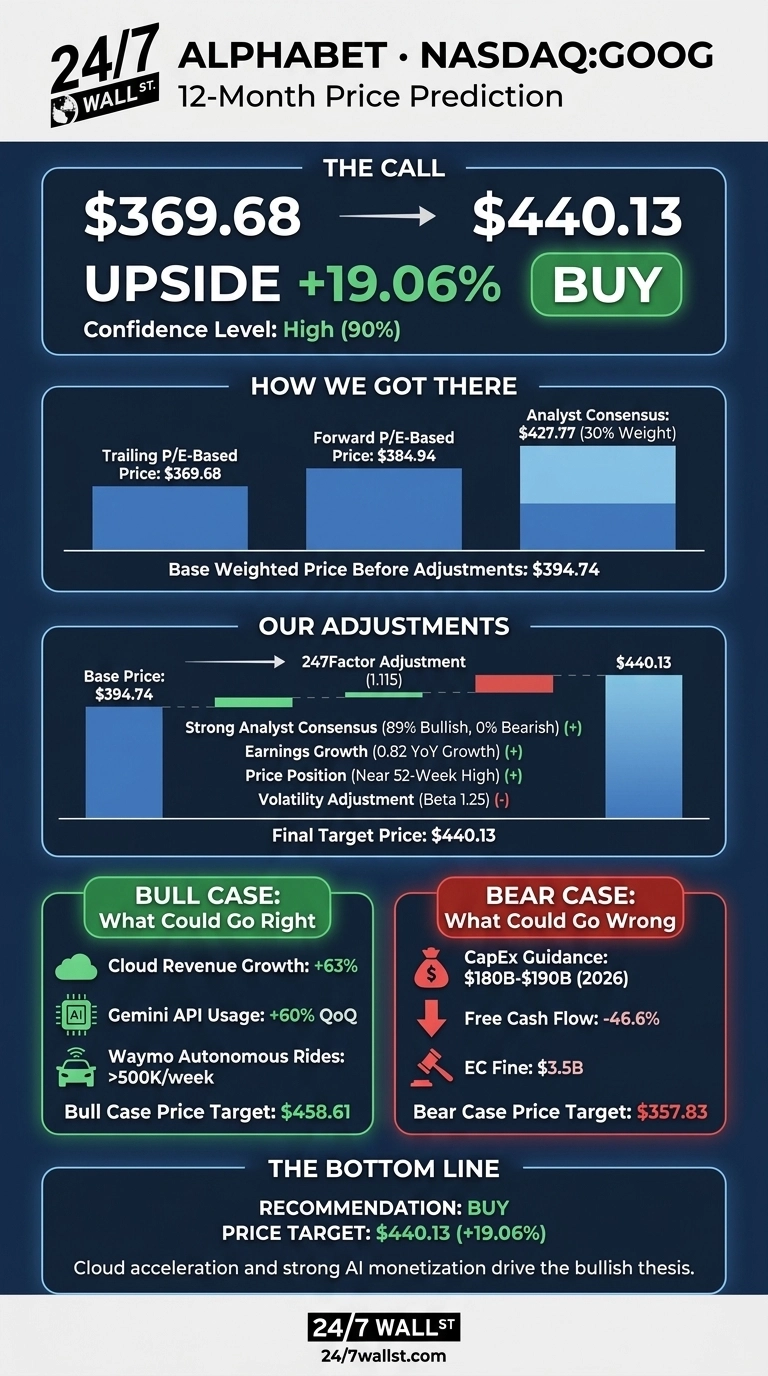

Our 24/7 Wall St. price target for Alphabet is $440.13, implying 19.06% upside from the current $369.68 quote. Our model carries a high-conviction bullish reading.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $369.68 |

| 24/7 Wall St. Price Target | $440.13 |

| Upside | 19.06% |

| Recommendation | BUY |

| Confidence Level | 90% |

The Setup Heading Into Q2 Earnings

Alphabet is a coiled spring right now. The stock is 6% below its 52-week high of $404.23, well off the 52-week low of $184.20, and up 18.13% year to date.

Q1 2026 was a blowout: revenue of $109.9 billion (+21.79%), EPS of $5.11 against a $2.6327 consensus, and Google Cloud revenue up 63% to $20.028 billion, with cloud backlog nearly doubling sequentially to $462 billion. Prediction markets currently assign a 96.6% probability that Alphabet beats again on July 22.

Why Bulls See a Breakout Past $450

The bull case rests on cloud, AI monetization, and Waymo optionality. Google Cloud operating margin already expanded from 17.8% to 32.9% year over year, and revenue from products built on GenAI models grew nearly 800%.

Gemini now processes 16 billion tokens per minute, Gemini Enterprise paid monthly active users grew 40% quarter-on-quarter, and Waymo just crossed 500,000 fully autonomous rides per week. If Q2 confirms cloud acceleration and TPU hardware revenue starts flowing in 2027, our bull case scenario points to $458.61.

What Could Go Wrong

The bear case centers on capital intensity. CapEx more than doubled to $35.674 billion in Q1, pushing free cash flow down 46.63%, and 2026 CapEx guidance was raised to $180 billion to $190 billion.

A $3.5 billion EC fine and Google Network revenue declining year over year add pressure. Bulls would counter that heavy investment reflects committed enterprise demand, evidenced by backlog nearly doubling sequentially. Our bear scenario lands at $357.83.

How Alphabet Compares to Microsoft and Meta

Microsoft (NASDAQ:MSFT) is the most direct cloud comparable. Microsoft trades at a P/E of roughly 29, with Azure growing 40% and commercial RPO surging to $627 billion. Google Cloud’s 63% growth is faster off a smaller base, and Alphabet’s lower multiple leaves room for our target to look conservative.

Meta Platforms (NASDAQ:META) is the ad-market counterpoint. Meta trades at a P/E of roughly 25, delivered 33.1% Q1 revenue growth, but guided full-year 2026 CapEx to $125 to $145 billion. Alphabet’s forward P/E of roughly 25 sits between the two, which makes our $440.13 target look reasonable.

| Company | P/E | Recent Revenue Growth |

|---|---|---|

| Alphabet | 27 | 21.8% |

| Microsoft | 29 | 18.3% |

| Meta | 25 | 33.1% |

Alphabet Price Prediction 2026-2030

The 24/7 Wall St. price target is $440.13, our recommendation is buy, and confidence is 90%. Cloud acceleration paired with a below-peer forward multiple tips the scale.

The bullish thesis strengthens if Q2 confirms sustained cloud growth at recent levels and stable ad monetization. The thesis weakens if CapEx pushes free cash flow into further contraction without commensurate backlog conversion.

The table below shows our 2026 and 2030 targets from the model; intermediate years are not published as separate point estimates.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $440 |

| 2030 | $634 |

These projections assume Alphabet continues executing on cloud, Gemini, and Waymo. Regulatory rulings or an AI CapEx overbuild could push the trajectory materially lower.

Contact [email protected] for any questions or corrections.