Tesla has spent the first half of 2026 pulling back from December highs. Our proprietary model answers the key question: where does the risk-reward stand from here?

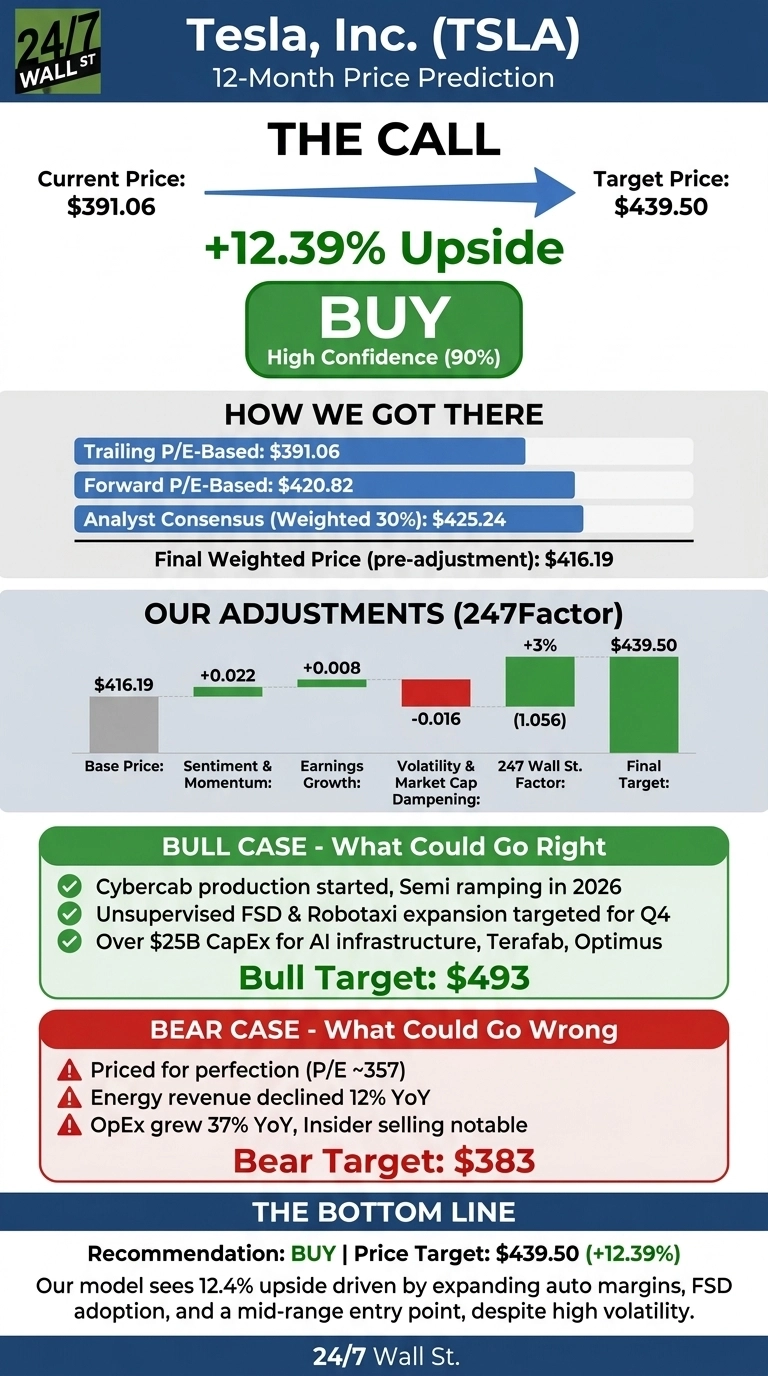

Tesla (NASDAQ: TSLA | TSLA Price Prediction) trades at $391.06 as of July 16, 2026. Our 24/7 Wall St. price target for Tesla is $439.50, implying 12.39% upside over the next 12 months. The recommendation is buy, with high (90%) model confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $391.06 |

| 24/7 Wall St. Price Target | $439.50 |

| Upside | 12.39% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Pullback From December Highs

Tesla is down 3.81% over the past week and 13.04% year to date, but still up 21.57% over 12 months. The stock sits 15% below its 52-week high of $498.83.

Fundamentals tell a constructive story: Q1 2026 revenue rose 15.78% year over year to $22.39 billion, non-GAAP EPS of $0.41 topped expectations, and automotive gross margin expanded to 21.1% from 16.2%. Free cash flow jumped 117% to $1.44 billion, and FSD paid subscribers hit 1.28 million, up 51%.

The Case for $493 and Higher

Our bull scenario points to $492.94, a 26.05% total return. Catalysts include Cybercab production has just started, Semi ramps this year, and CFO Vaibhav Taneja’s guidance to “over $25 billion of CapEx” in 2026 for six factories, AI infrastructure, and Terafab.

Elon Musk described unsupervised FSD reaching customer cars “probably in the fourth quarter” and Optimus as “the biggest product ever”. Robotaxi is live in Austin, Dallas, and Houston with zero reported incidents. Polymarket traders assign an 81.5% probability to Tesla beating its next earnings report.

What Could Push Shares to $383

Our bear case lands at $383.32, a 1.98% decline. Tesla is priced for perfection at a trailing P/E of 357, and energy storage revenue fell 12% YoY in Q1, with regulatory credits sliding to $380 million. Operating expenses grew 37% YoY as AI R&D and Musk’s CEO stock-based comp hit the P&L.

Bulls counter that OpEx growth is investment: operating income still jumped 135.84%, and Taneja acknowledged Tesla is “in a very big capital investment phase” that supports future revenue. Insider selling has been notable, with 30 recent insider transactions skewed toward sales.

How Tesla Stacks Up Against Rivian and Ford

Rivian (NASDAQ: RIVN) is the closest pure-play EV comparable. Rivian’s $24.67 billion market cap, Q1 2026 revenue of $1.38 billion, and adjusted loss of $0.54 per share show how far Tesla leads on scale and profitability.

Rivian guides to a $1.8 to $2.1 billion EBITDA loss in 2026, making Tesla’s premium multiple defensible.

Ford (NYSE: F) offers a valuation counterpoint. Ford’s Q1 2026 EPS of $0.66 on $43.25 billion in revenue dwarfs Tesla in absolute earnings, yet Ford’s market cap is $55.5 billion.

Ford also pays a 5.4% dividend yield. That contrast frames Tesla as an autonomy and robotics play rather than a traditional automaker. Our 24/7 Wall St. price target is reasonable in that context.

Tesla Price Prediction 2026-2030

Tesla’s 24/7 Wall St. price target of $439.50 and buy rating at 90% confidence rest on expanding auto margins, FSD subscription growth, and a mid-range entry point. The bull thesis strengthens if Cybercab and Robotaxi hit 2026 milestones. The risk case builds if OpEx growth outpaces revenue into 2027.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $439.50 |

| 2027 | $478.00 |

| 2028 | $515.00 |

| 2029 | $550.00 |

| 2030 | $584.82 |

Our five-year base case projects Tesla at $584.82 by July 2031, a 49.55% total return. These projections assume Tesla executes on autonomy, energy, and Optimus. Meaningful upside or downside could result from unsupervised FSD approval timing in China and Europe.

Contact [email protected] for any questions or corrections.