When your early retirement goal is finally within sight, that is not the time to take your foot up off the pedal. In fact, there is still a lot of work to do. Especially when you have significant assets that are expected to sustain you through your Golden Years, it is important to have a plan in place that will see you through periods of extreme volatility.

A Redditor on the r/fatFIRE subreddit finds himself in this exact situation and wants to know how to best plan for what comes next.

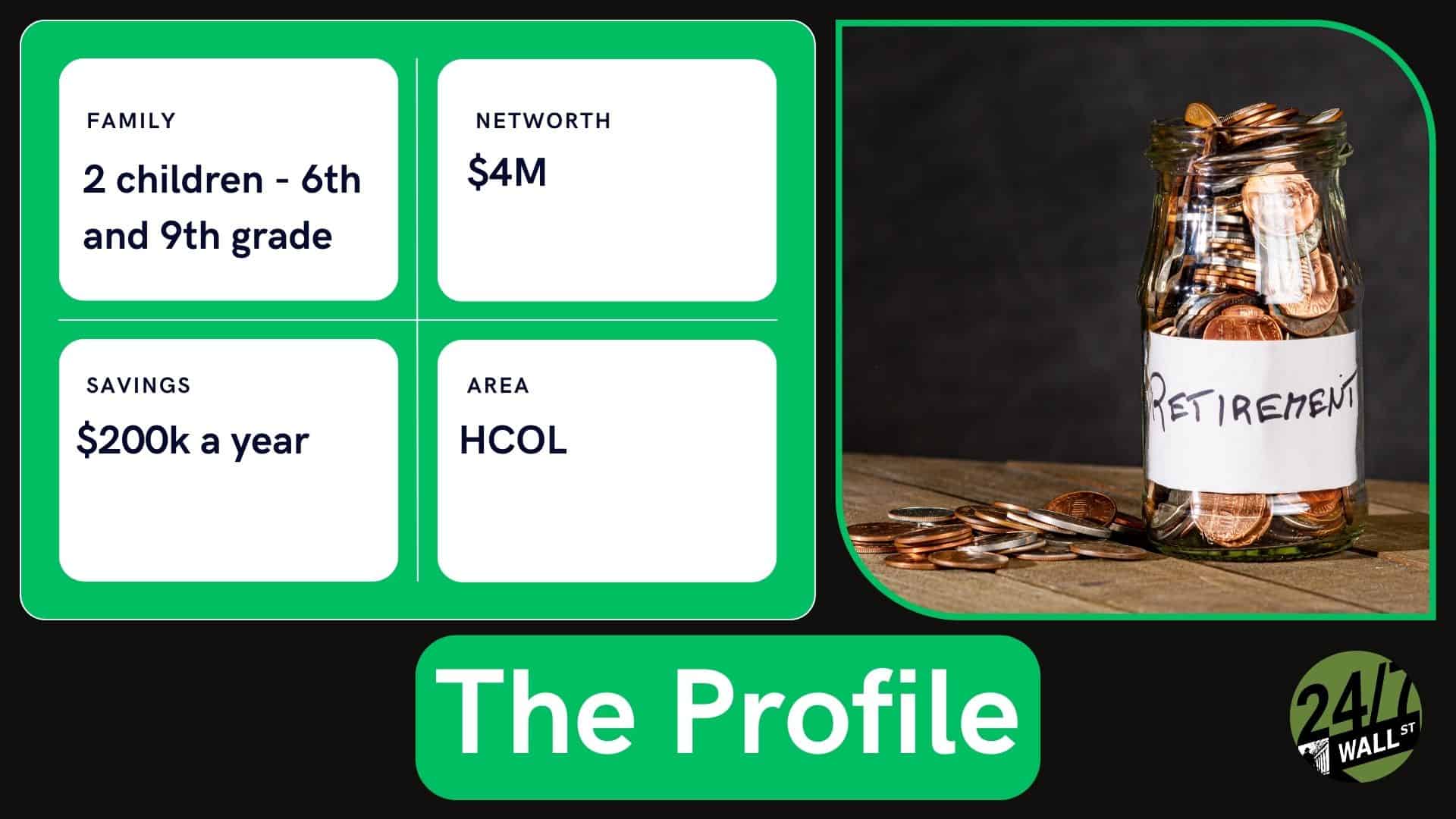

At 50 years old, he has a $4 million net worth in a brokerage account and is looking to retire in seven years when his youngest child goes to college. The goal is to hit his $6 million fatFIRE number early, at which time he expects his annual expenses to be about $200,000 a year. With college fully paid for and current household income of $700,000 a year, the Redditor wants to know what kind of cash he should make available now versus a few years closer to retirement.

Because every situation is different, there is no one-size-fits-all plan to follow. Yet there are some broad strategies you can follow as you approach retirement. Of course, I’m not a financial advisor, and this is just my opinion, so note that no one answer works every time.

24/7 Wall St. Key Points:

- Planning to retire early and comfortably is the goal of many and having a plan for achieving it is essential.

- Having the right mindset for waking up retired one day is a critical piece of the puzzle, but so is being prepared for all the financial havoc that may happen during retirement.

- Also: Take this quiz to see if you’re on track to retire (Sponsored)

Being in your right mind

A surprisingly important step is ensuring you have the right mindset for retirement. After decades of work and raising a family, suddenly being out of a job and having an empty nest will seem jarring.

Using your time before these events occur to put yourself in the proper framework. For instance, take time off from work to explore new interests. is essential. It will be important to find something that will hold your attention in retirement. The one thing you don’t want to do is wake up bored. Outside interests and friends will be an important component of your retirement plan.

Planning for a worst-case scenario

Arguably one of the biggest risks to successfully transitioning to early retirement is the “sequence of returns risk,” or SORR. It refers to an event or series of events occurring soon after retiring that dramatically hurts your returns.

Because your retirement account is at its peak value, a market crash, a return of hyperinflation, or some geopolitical catastrophe could crush the value of your available funds. The sudden appearance of SORR at the outset can adversely ruin your plans.

One way to mitigate the risk is to create a so-called “crisis fund.” This is similar to an emergency fund most people are familiar with. In this case, it is a one-time use fund covering at least one, but preferably two years of expenses.

You are establishing an insurance policy against a catastrophic event and it will only be tapped if a SORR event happens. That way you don’t have to tap into your retirement funds at the worst possible moment, which would affect your ability to ride out several decades of retirement.

A coordinated plan of attack

Using more conventional methods of financial planning also must be considered. For example, funds in a 401(k) plan that come with required minimum distributions (RMDs) might be converted over to a Roth IRA or Roth 401(k) plan that don’t have RMDs and minimize taxes over your projected lifespan.

Begin diversifying your portfolio now with an eye on mitigating capital gains while understanding the accounts you currently have and when withdrawals from them should be or need to be made.

While you could take a DIY approach to this, a better solution is to speak with a financial advisor and tax professional who can create a plan based on your unique situation. Steeped in their respective subject matters, they don’t need the learning curve you would have to follow to get up to speed.

There is no specific dollar amount you should have on hand, but rather utilize a holistic approach to you pending retirement. Easing you way to your goal mindful of the risks is the best plan of attack.

Contact [email protected] for any questions or corrections.