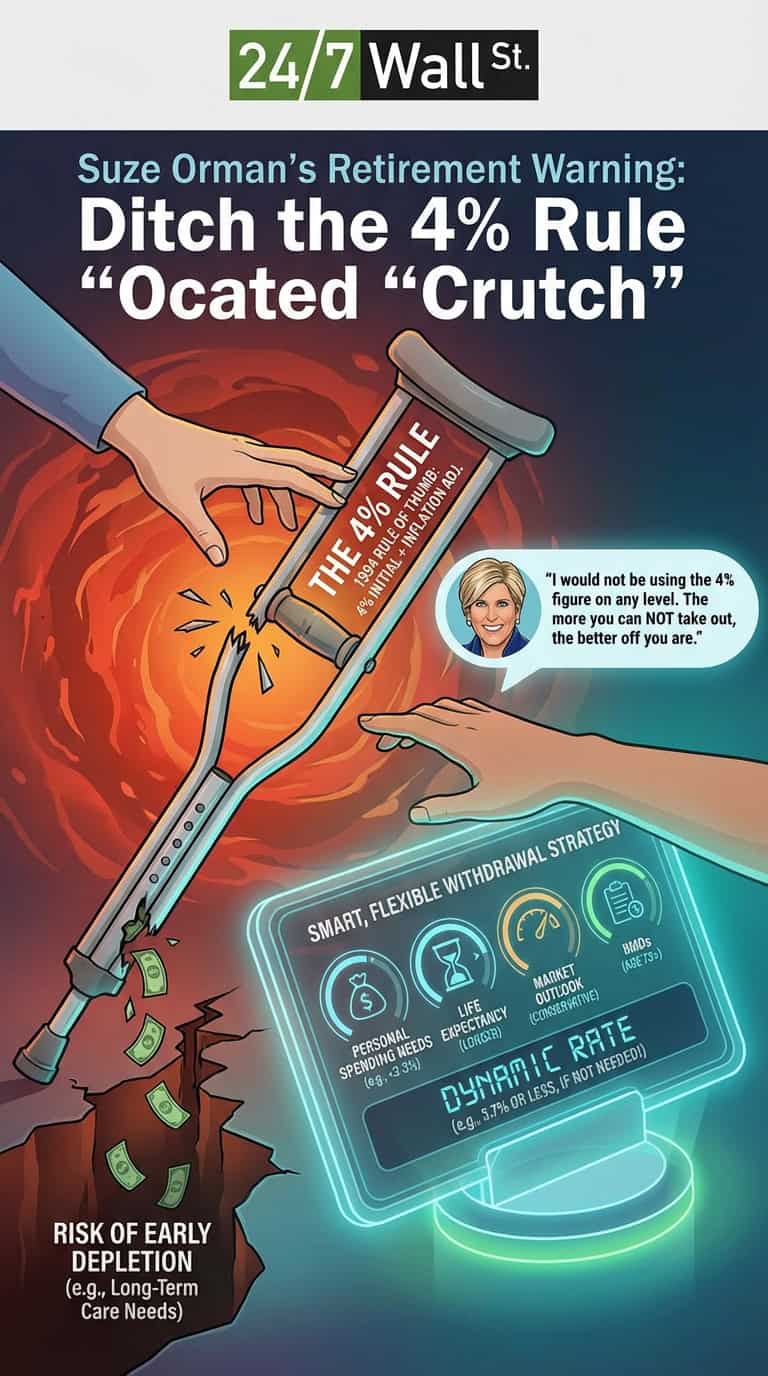

When it comes to retirement, some longstanding rules of thumb have become deeply embedded in how Americans plan for their financial future. Finance expert Suze Orman has a pointed warning about one of the most popular. She has urged retirees to stop following the 4% rule entirely, saying “I would not be using the 4% figure on any level.”

So what is the 4% rule, why is Orman pushing back against it so forcefully, and should you take her advice? Here is what you need to know.

What is the 4% rule?

The 4% rule is a straightforward guideline designed to help retirees choose a safe annual withdrawal rate. Under the rule, a retiree can withdraw an inflation-adjusted 4% of their investments each year and expect that money to last through a 30-year retirement. Using a $1 million nest egg as an example, that translates to $40,000 in year one, with the dollar amount adjusted upward each year to keep pace with inflation.

In October 1994, financial planner William Bengen published his findings in the Journal of Financial Planning, and what is now known as the 4% rule was born. Bengen tested every rolling 30-year period in U.S. market history and found the strategy never failed. His goal was to give retirees a concrete, historically grounded benchmark so they could plan withdrawals without the fear of running dry too early.

What’s Orman’s problem with the 4% rule?

Orman’s core objection is that a fixed withdrawal percentage encourages retirees to take money out whether they need it or not. “It doesn’t work anymore. I think it’s very dangerous,” she said in a 2024 interview, recommending that retirees scale back to 3%, or even less.

“Maybe you were taking out 4% and 4% even though you didn’t need it,” she said. The risk is concrete: a retiree who takes unnecessary distributions for years may one day need expensive long-term care but find the account has been drained by withdrawals that were never necessary in the first place.

“The more you cannot take out of a retirement account, the better you are,” she explained, pointing to the uncertain economic landscape retirees face today. Her reasoning covers three intersecting pressures: markets are unpredictable, inflation chips away at purchasing power, and people are living longer than ever. Together, those forces create a difficult environment for retirees who anchor their spending to any single fixed number.

It is worth noting that Orman has also offered some context around timing. She has written that starting withdrawals at around age 70 changes the calculus: “If you don’t start withdrawals until around age 70, 4% can work just fine. And if you have all your living costs covered by guaranteed income, more than 4% may be viable.” Her sharpest criticism targets early retirees who begin drawing down at 60 or 65 and lock into a rate without flexibility built in.

The 2026 retirement reality check

The macroeconomic backdrop has shifted considerably since Bengen first ran his numbers on 1926-to-1994 market data. The right safe starting withdrawal rate depends on equity valuations, bond yields, prospects for inflation, and a retiree’s own life expectancy and asset allocation. Morningstar’s 2025 retirement income research puts the baseline safe starting withdrawal rate at 3.9% for retirees seeking consistent inflation-adjusted spending, assuming a 90% probability of having funds remaining at the end of a 30-year retirement period. That figure is up slightly from 3.7% in 2024, and applies to portfolios with between 30% and 50% in equities.

Bengen himself later updated his findings to suggest a higher figure. He now cites 4.7% as the “Universal Safemax,” the historical maximum safe withdrawal rate for all retirees. The gap between Morningstar’s 3.9% and Bengen’s 4.7% reflects a fundamental methodological difference: Bengen’s number is backward-looking, drawn from actual historical returns, while Morningstar’s research embeds forward-looking capital market assumptions that can be more conservative when equity valuations are elevated.

Orman’s playbook: the 3-to-5-year cash reserve

Beyond questioning the withdrawal percentage, Orman advocates for a defense strategy built around cash. The framework centers on maintaining three to five years of baseline living expenses in liquid, high-yield savings instruments or short-term vehicles. During a market downturn, retirees draw from this cash reserve rather than liquidating equity positions at depressed prices.

The approach directly addresses sequence-of-returns risk. That is the danger that poor market returns in the first years of retirement can permanently impair a portfolio’s recovery, even if markets rebound strongly afterward. If retirement coincides with a sustained market downturn, retirees forced to sell at low prices lock in losses that a later rally cannot fully undo. A substantial cash buffer breaks that chain by eliminating the need to sell equities when they are down.

Dynamic spending: smarter alternatives to a rigid rule

Rather than locking into a fixed annual percentage, modern retirement research increasingly favors flexible frameworks that adjust spending based on portfolio performance and personal circumstances.

The Guardrails Strategy: This approach sets both a spending ceiling and a floor. Retirees begin at a higher initial withdrawal target and agree in advance to trim spending if the portfolio falls below a predetermined threshold, or to take more if it grows well. Morningstar’s research estimates that the guardrails method supports a starting safe withdrawal rate of 5.2% for a portfolio of 40% equity and 60% bonds. With the most flexible configurations, including strategies that incorporate Social Security delays and annuities, starting rates can reach as high as 5.7%.

The Social Security bridge: This method draws more heavily from retirement accounts in the early years, using portfolio withdrawals as a temporary income bridge. The payoff comes later. By delaying Social Security claims until age 70, retirees lock in higher monthly payments that are guaranteed, inflation-adjusted, and backed by the federal government, which reduces the long-term burden on the investment portfolio considerably.

Is Orman right?

On the central point, Orman has it right. Withdrawing 4% by default when you don’t need the money is a shortsighted approach, and preserving retirement savings almost always serves retirees better than spending them down on a schedule set decades ago by someone else’s research.

There are also structural problems with the 4% rule that go beyond Orman’s concern about unnecessary withdrawals. According to the CDC, life expectancy for the U.S. population reached 79.0 years in 2024, an all-time high. Orman’s recommendation is to assume you will live until at least age 95. If you are in excellent health and have a family history of long-lived parents and grandparents, she advises building a withdrawal strategy around your money lasting until you are 100. A rule calibrated to a 30-year retirement may fall short if you live into your late 90s.

Morningstar’s current research puts the baseline safe withdrawal rate at 3.9% for new retirees planning a 30-year horizon. A more conservative starting point gives retirees a larger margin for unexpected expenses, healthcare costs, and market volatility. That cushion is particularly valuable for those without substantial pension income or other guaranteed cash flows to fall back on.

The right withdrawal rate is personal. It depends on your total portfolio size, risk tolerance, estimated life expectancy, and whether you are subject to Required Minimum Distributions. Under current law, the RMD age is 73 for those born between 1951 and 1959, or 75 for those born in 1960 or later (the age-75 threshold takes effect in 2033 under the SECURE 2.0 Act). These mandatory withdrawals from tax-advantaged accounts can complicate a carefully planned drawdown strategy, making it even more important to have a plan tailored to your specific situation rather than one anchored to a generic rule.

Working with a qualified financial advisor to determine the right withdrawal rate for your circumstances is likely the most valuable step you can take. Orman’s advice to abandon the 4% rule as a one-size-fits-all answer and instead build a withdrawal plan grounded in your actual financial picture is sound guidance worth taking seriously.

Editor’s note: This article was updated to add Suze Orman’s clarification that a 4% withdrawal starting at age 70 “can work just fine,” providing context that her sharpest criticism targets early retirees. The guardrails section was expanded to reflect that Morningstar’s most flexible retirement spending strategies can support starting withdrawal rates as high as 5.7%. The note on RMD ages was updated to specify that the age-75 threshold takes effect in 2033 under SECURE 2.0.

Contact [email protected] for any questions or corrections.