As retirement nears and the start of 2026 right around the corner, reallocating a 401(k) becomes critical to balance growth, income, and risk, ensuring savings last through decades of life after work. In their 50s, many investors, like a recent Redditor on the r/PersonalFinance subreddit, seek to shift from aggressive saving to a strategy that protects their nest egg while supporting a sustainable 4% withdrawal rate.

The Redditor, aged 55, asked for safe options to adjust their 401(k) as they approach retirement, expressing a desire to reduce risk while maintaining growth to fund distributions. He was unsure whether to leave funds untouched, explore annuities, or reallocate.

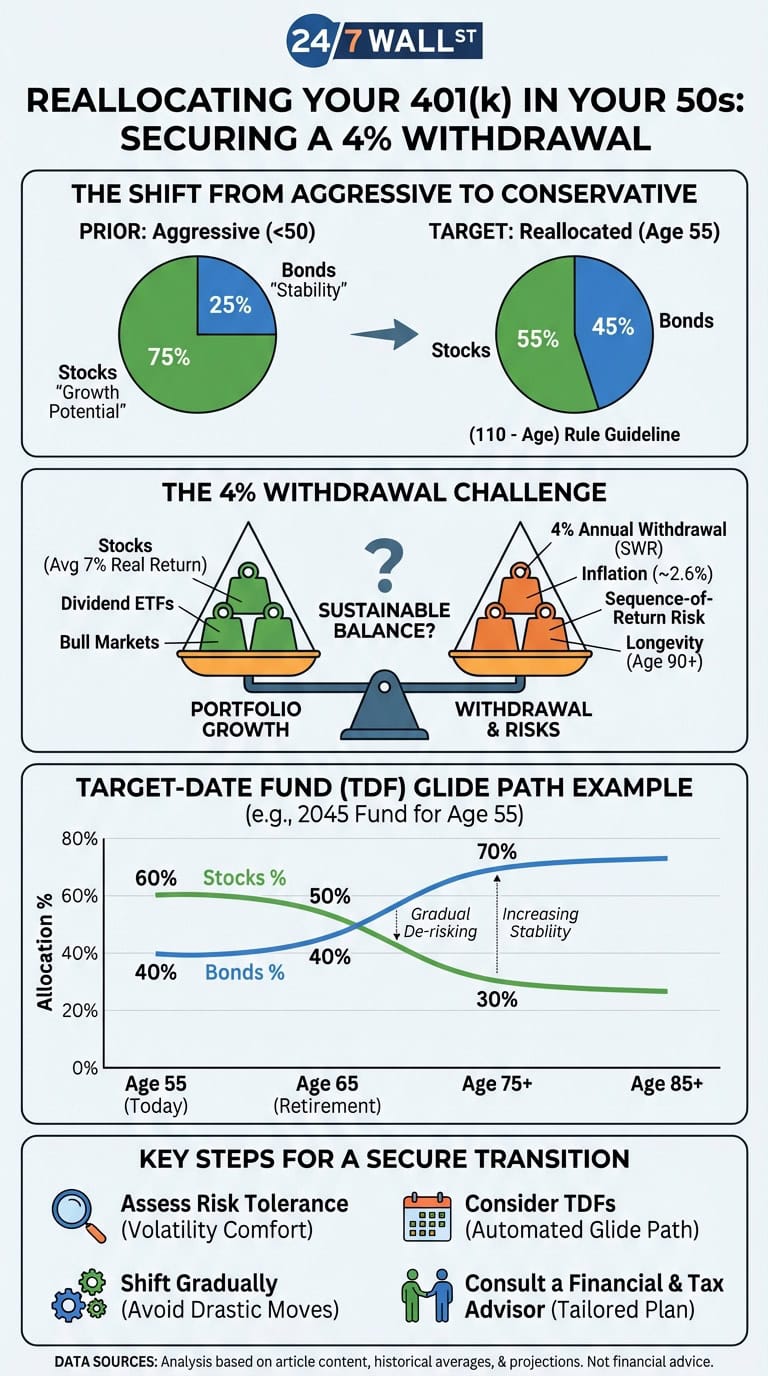

I’m not a financial planner or tax professional, so these are just my opinions, but I’ll give some tips on how, in your 50s, you should focus on risk assessment, conservative investments, and professional guidance to secure a comfortable retirement.

Assessing Risk Tolerance and Financial Needs

At 55, risk tolerance typically declines as retirement looms, but the need for growth persists to outpace inflation, projected by the Federal Reserve to run at 2.6% annually in 2026.

Start by evaluating your comfort with market volatility. Can you stomach a 20% portfolio drop, as we saw in 2022’s bear market, or do you prefer stability? Consider your 401(k)’s size, other assets (e.g., home equity, IRAs), and expenses. If a 4% withdrawal rate covers living costs — for example, $40,000 per year from a $1 million portfolio — a conservative approach is viable. Otherwise, you will still need to take some risks.

Review your current holdings, often stocks, mutual funds, or exchange-traded funds (ETFs), to ensure they align with your goals. For instance, a retiree needing $75,000 annually may require a larger stock allocation to grow their portfolio and to balance risk with longevity.

Shifting to Conservative Investments

Reallocating a 401(k) when you turn 55 should be gradual to avoid locking in losses or missing growth. A common guideline is to subtract your age from 110, suggesting a 55-year-old allocate 55% to stocks and 45% to bonds. Stocks, which have averaged 7% real returns since 1928, drive growth, while bonds, yielding about 4% today, provide stability.

For example, shifting from a 70/30 stock-bond mix to 50/50 reduces volatility while still preserving upside potential. Dividend-focused ETFs yielding 2% to 3% can supplement income and help mitigate sequence-of-return risk if markets dip early in retirement. Sequence-of-return risk just means money withdrawn during a bear market is more costly than if you withdrew it during a bull market.

Avoid drastic moves, like switching entirely to fixed income investments, which may not keep pace with inflation over a 30-year retirement, especially with lifespans increasing. The U.S. Centers for Disease Control says 20% of 65-year-olds reach age 90.

Target-Date Funds: A Hands-Off Solution

For those preferring simplicity, target-date funds (TDFs) automatically adjust allocations, becoming more conservative as retirement nears. A 2045 TDF, suitable for a 55-year-old planning to retire at 65, might hold 60% stocks and 40% bonds, shifting to 30/70 by 2045. Funds like the Fidelity Freedom 2045 (MUTF:FFFGX) offer low fees (0.75%) and diversification, reducing the need for active management.

TDFs suit the Redditor’s desire for a “set it and forget it” approach, though they should verify that the fund’s glide path aligns with their risk tolerance and withdrawal plans. Alternatives like balanced funds provide similar benefits, but allow for customization.

Ensuring a 4% Withdrawal Sufficiency

The 4% safe withdrawal rate (SWR) rule of thumb assumes a portfolio can sustain 4% annual withdrawals, adjusted for inflation, for 30 years. At 55, early retirement demands scrutiny. Can 4% cover expenses, or will inflation erode purchasing power? If insufficient, maintaining 50% to 60% in stocks for five to 10 years can boost growth while leveraging bull markets.

Conversely, if 4% is sufficient, prioritizing bonds and TDFs minimizes risk. Non-401(k) assets, like paid-off homes or savings, enhance your flexibility. Annuities, mentioned by the Redditor, guarantee income, but often have high fees (1% to 2% annually), making them less appealing unless longevity is a concern.

Key Takeaways

At 55, reallocating a 401(k) involves balancing risk and growth to support a 4% SWR. Assessing risk tolerance, gradually shifting to a 55/45 stock-bond mix, and considering target-date funds align with the Redditor’s goals of reducing risk while ensuring growth.

Your best bet is to consult with a financial advisor and tax professional to tailor allocations, evaluate expenses, and navigate market uncertainties. This will help pave the way for a secure retirement.

Contact [email protected] for any questions or corrections.