You’ve probably heard that waiting to claim Social Security is always the smarter move. Delay long enough and you’ll eventually collect a fatter monthly check. The logic is sound as far as it goes, but it leaves out a lot. Whether waiting is actually the right call depends heavily on personal circumstances, and for many retirees, the opportunity cost of waiting is higher than the extra dollars they’ll eventually pocket.

There is no one-size-fits-all answer when it comes to the timing of Social Security benefits. The sooner you recognize that, the better positioned you’ll be to make a decision that genuinely fits your life.

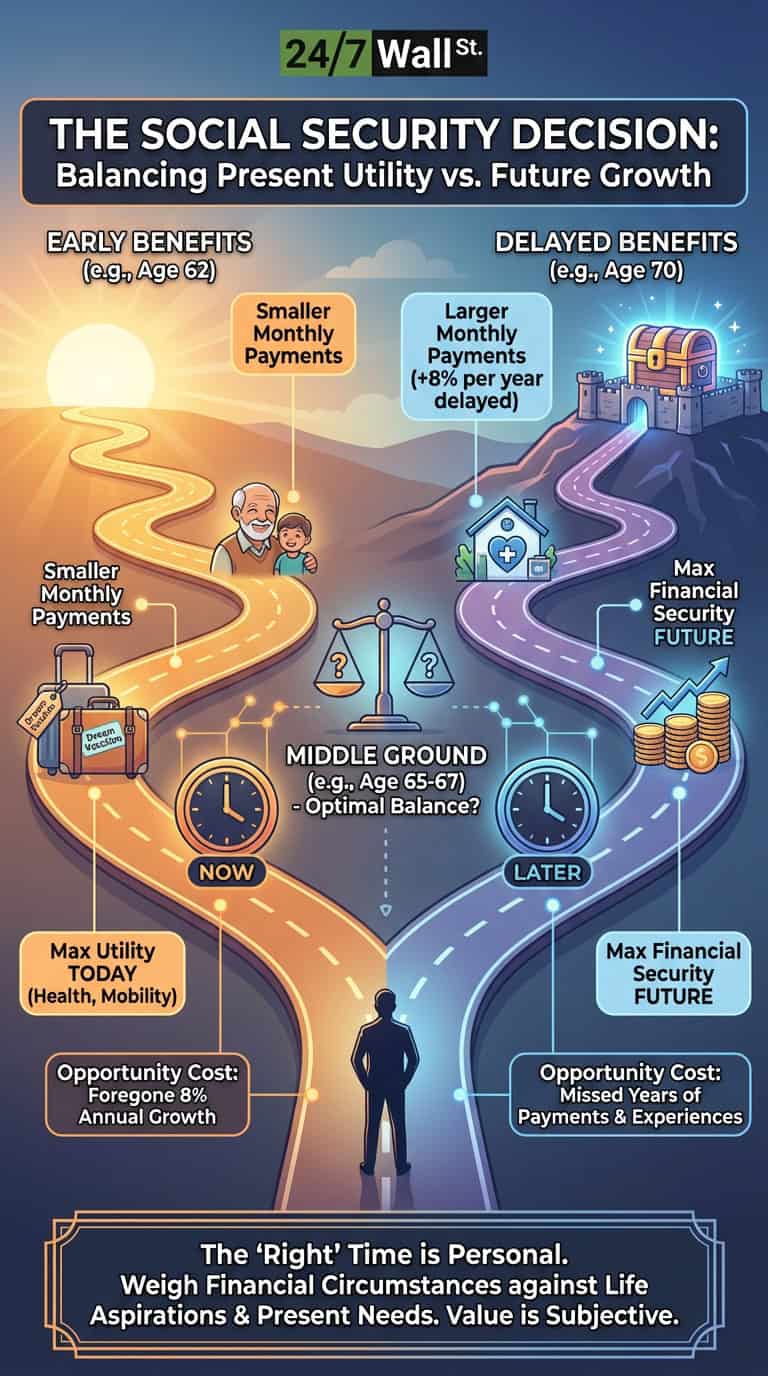

The real cost of delaying Social Security benefits

The mechanics are straightforward. According to the Social Security Administration, every year you delay claiming past your full retirement age adds 8% to your monthly benefit, up to age 70. For anyone born in 1960 or later, full retirement age is 67. That 8% annual bump is an appealing guaranteed return, especially compared to the volatility of equity markets. But comparing the two as if they were interchangeable ignores a critical factor: money available today has value that money available in five or eight years does not.

The break-even math puts this in concrete terms. If you’re weighing claiming at 62 versus waiting until your full retirement age of 67, the cumulative totals don’t converge until roughly age 78 and 8 months, according to AARP. Push the comparison out to age 70 versus 62 and the break-even pushes to around age 80 to 81. Waiting from 62 to 70 does produce a monthly check that is about 77% larger, but you’ll need to live well into your 80s for the lifetime totals to favor the delay. Health, family history, and personal spending patterns all shape how realistic that scenario actually is for any given person.

The trust fund question is now part of the calculation

A growing number of Americans are factoring the program’s solvency into their claiming decision. A 2025 AARP poll found that more people are claiming early specifically because of concerns about Social Security’s financial future. Those concerns are not unfounded. The 2026 Trustees Report, released in June 2026, projects the OASI Trust Fund will be depleted in the fourth quarter of 2032. At that point, only about 78% of scheduled benefits would be payable from ongoing payroll tax revenue, unless Congress acts to close the gap. That is a meaningful shift from earlier projections, and it adds a layer of uncertainty to the argument for delaying benefits.

To be clear, Social Security is not going away. But if you are currently in your early 60s, the trust fund’s trajectory is a legitimate variable in your timing decision. Claiming earlier locks in benefits before any potential legislative adjustment to the program. Research published by the National Bureau of Economic Research found that only about 10% of eligible Americans actually wait until age 70 to claim, suggesting that most people arrive at a similar conclusion on their own.

Are the opportunity costs too high to justify waiting?

The broader opportunity cost argument goes beyond numbers. Time and mobility are not infinite, and the utility of money at 63 is generally higher than the utility of money at 72. Spending on travel, family experiences, or other active pursuits is often easier earlier in retirement than later. A slightly smaller monthly check that arrives when you can fully use it may deliver more real-world value than a larger one that arrives after your health or circumstances have changed.

For those who genuinely do not need the income right away, delaying makes sense. Cost-of-living adjustments also compound on a larger starting benefit when you delay, which provides a measure of inflation protection over a long retirement. Married couples carry an additional consideration: when the higher-earning spouse delays, they also raise the survivor benefit their partner would receive. That dynamic makes delaying especially valuable as a form of longevity insurance within a household.

For everyone else, the calculus is more personal. A financial adviser can run the numbers for your specific benefit estimate, but the numbers alone will not tell you whether a dream trip with the grandkids at age 64 is worth more to you than a larger deposit at 72. That is not a math problem. It is a question of values and priorities.

The big questions to ask yourself

Start with your health and family history. If longevity runs in your family and your current health is strong, the break-even math starts to favor waiting. If neither of those is true, claiming earlier may leave you with more total lifetime income and more time to enjoy it. Then consider your financial picture. If you have enough in savings or other income to cover your expenses in your early 60s without Social Security, delaying is a more viable option. If cash flow is tight, the decision may already be made for you.

A middle path also exists. Claiming at 65 rather than 62 reduces the permanent reduction to your benefit while still delivering income years before the age-70 maximum. It is a reasonable compromise for those who want a balanced approach between present income needs and long-term benefit size. The average monthly retirement check was about $2,081 as of April 2026, a figure that underscores just how central Social Security is to most retirees’ budgets.

There is no rush to decide, unless you have already reached 70, at which point further delay no longer adds to your benefit. The best framework is to weigh your financial constraints, health outlook, family situation, and what you actually want to do with the years ahead. Sometimes a dollar available today is worth more than two dollars available a decade from now, especially when the road ahead is shorter and the scenery may have changed.

Editor’s note: This article was updated to incorporate the 2026 SSA Trustees Report projection that the OASI Trust Fund will be depleted in Q4 2032 with 78% of benefits payable, concrete break-even age figures from AARP (roughly age 78-8 months for a 62-vs-67 comparison and about 80-81 for 62-vs-70), a 2025 AARP poll finding on early-claiming trends, NBER research showing only about 10% of eligible Americans wait until age 70, the average monthly retirement benefit of approximately $2,081 as of April 2026, and added context on survivor-benefit considerations for married couples.

Contact [email protected] for any questions or corrections.