Both Suze Orman and Dave Ramsey are well-known personalities who aim to provide financial advice to millions of listeners. Both have, unsurprisingly, addressed the important issue of when to claim Social Security. However, they have very different takes on this issue.

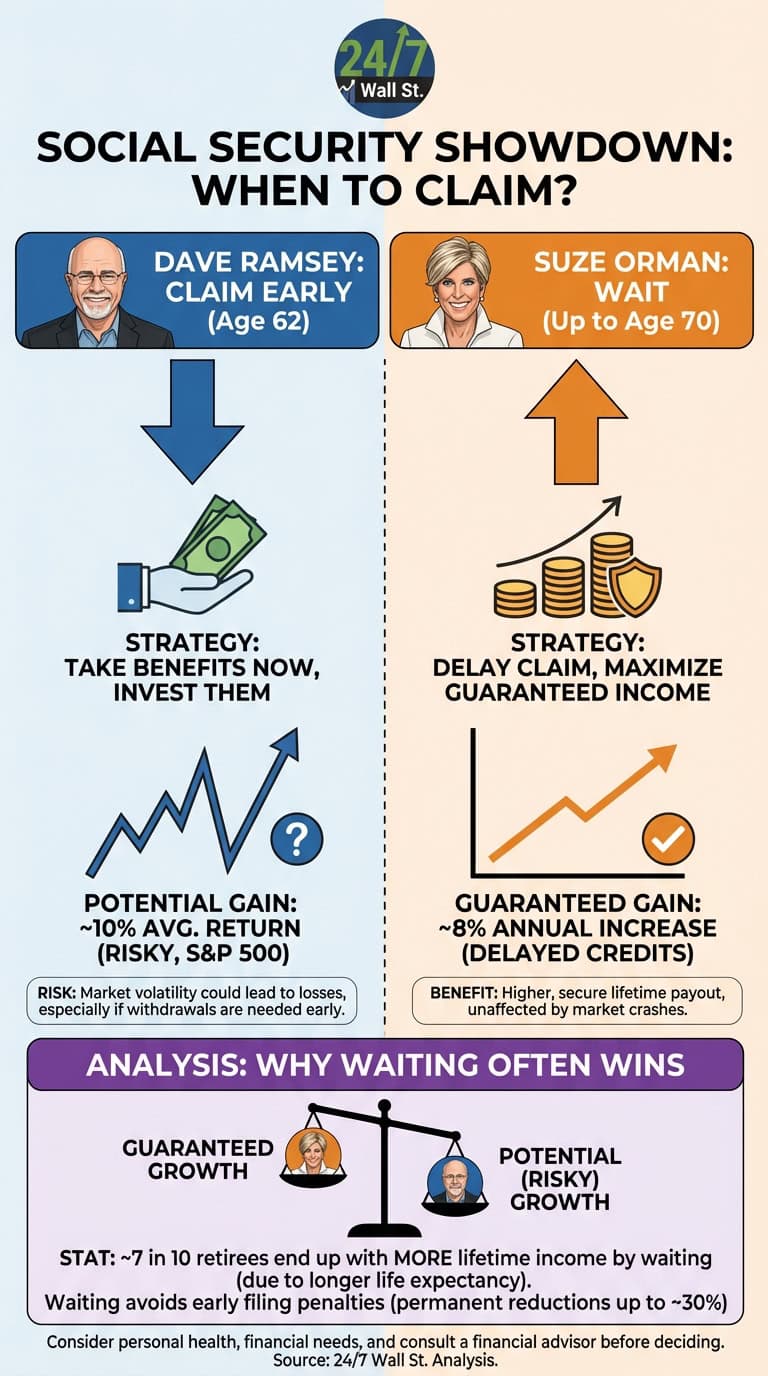

Specifically, Dave Ramsey has said people should take Social Security at 62, which is as early as they are allowed to claim it. He wants people to take the benefits early and invest the money they collect from Social Security to grow their wealth. That’s because he believes investing the money could leave you better off than delaying your benefits claim, even though a delay does boost your benefit by allowing you to avoid early filing penalties and earn delayed retirement credits.

Suze Orman has a different philosophy. She believes you should wait as long as you can to claim Social Security, so you avoid the penalties imposed on early filers and max out your delayed retirement credits. So, the big question comes down to: Who is correct?

Does Suze Orman or Dave Ramsey recommend the right Social Security claiming approach?

Ramsey’s advice might seem to make good sense because you can, in theory, earn a 10% annual return on your invested funds by putting the money into an S&P 500 index fund.

By contrast, an early Social Security claim reduces your benefits by 5/9 of 1% per month for each of the first 36 months you claim benefits ahead of full retirement age, and by 5/12 of 1% for any prior month. This results in a reduction in benefits of 6.7% for each of the first three years of a claim before full retirement age and an additional 5% per year cut for claims made more than 36 months ahead of FRA. And, a delayed Social Security claim increases benefits by 2/3 of 1% per month or 8% annually.

Earning 10% is better than avoiding a 5% or 6.7% loss, and better than earning an 8% annual gain.

The issue is, though, that the 10% average annual return from the S&P 500 is over the long haul. The investment could easily lose money for a year, or even for a few years. If you are in your 60s and you claim Social Security at 62 to try to invest the money and the S&P then has a few really bad years, you’ll be left in a bad spot because not only did you not increase your Social Security benefits by investing, but you may have to start making withdrawals to support yourself and could lock in losses if you have to start withdrawing the invested funds at a bad time.

Giving up a guaranteed increase in Social Security benefits in exchange for the possibility of doing better by investing just doesn’t make sense for most people. And that’s not even taking into account how many people claim early because they have grand plans to invest the money, but then find that life gets in the way and they end up spending it instead.

Orman has the right approach to your Social Security claim

Orman’s approach is different. She advises waiting so you can increase this source of guaranteed lifetime income, and she’s right to make that suggestion.

While delaying Social Security can sometimes be challenging if it means you need to live on your savings for longer or wait to retire, a delay has a guaranteed payoff. What’s more, most people do more than just break even if they wait to claim benefits — they end up with more lifetime Social Security income.

That’s because most people now live longer than they did when the system of early filing penalties and delayed retirement credits was created. These benefits and credits were intended to equalize lifetime benefits no matter when you claimed them, but now studies have shown that around 7 in 10 retirees end up better off if they wait.

If you don’t want to gamble your security as a senior on the hope that you’ll be able to successfully invest your Social Security, listening to Orman can pay off. Wait to claim your benefits if you can. You could also consider talking with a financial advisor to get personalized advice on the claiming age that makes sense for your individual situation, since factors like your retirement goals and your nest egg could affect when the optimum time is to begin your benefits.

Contact [email protected] for any questions or corrections.