As a retiree, you are probably going to rely on Social Security for support, and you need to decide when you want your retirement benefit checks to start.

Suze Orman has strong opinions on that question, and her advice could make a meaningful difference to your finances. She has issued a stern warning that every near-retiree should read before claiming a monthly benefit from the Social Security Administration.

Here is what that warning says, and why it deserves your full attention.

Listen to Suze Orman’s stern warning on Social Security

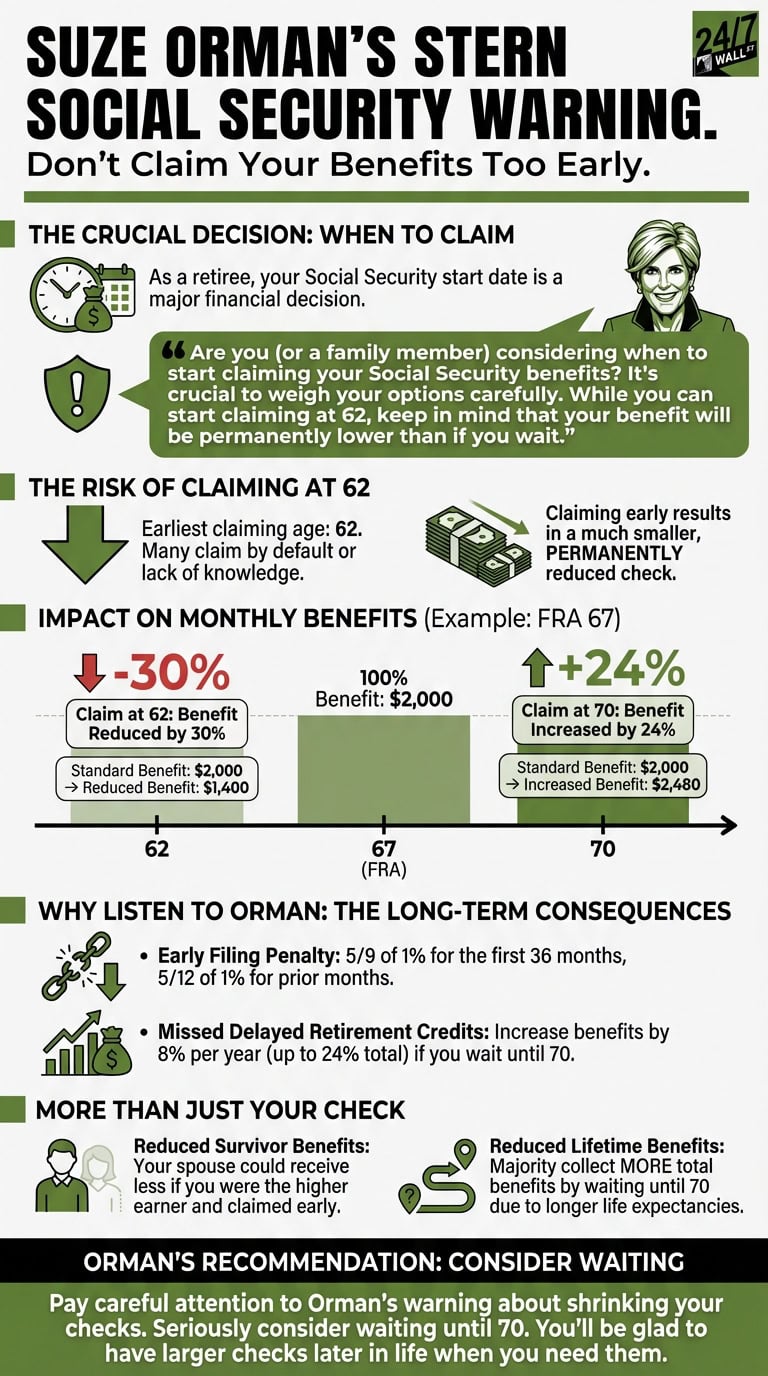

Orman posted her Social Security warning on LinkedIn, writing: “Are you (or a family member) considering when to start claiming your Social Security benefits? It’s crucial to weigh your options carefully. While you can start claiming at 62, keep in mind that your benefit will be permanently lower than if you wait.”

The warning centers on a decision that catches many people off guard. Age 62 is the earliest you can claim Social Security retirement benefits, and a large share of retirees start their checks at that point. Some do so because they feel financially ready to retire and assume they need those benefits immediately. Others simply do not realize what an early claim costs them over the long run. Because the government will send checks the moment you qualify, waiting can feel counterintuitive.

As Orman points out, claiming at 62 locks in a much smaller monthly check for life. Every worker has a designated full retirement age (FRA). For anyone born in 1960 or later, that age is 67. Claiming before FRA triggers a permanent benefit reduction, while claiming after FRA earns delayed retirement credits that grow your check for as long as you live.

Many people underestimate how large that reduction will be, and very few realize it cannot be undone. Once you lock in an early benefit, you can never recapture the monthly income you would have received by waiting.

Why you should listen to Orman about when to claim Social Security

An early claim can have serious long-term consequences. Every month you claim before FRA triggers an early-filing penalty: 5/9 of 1% per month for the first 36 months before FRA, and 5/12 of 1% per month beyond that. Those penalties compound to a 30% permanent reduction for someone with an FRA of 67 who claims at 62. In concrete dollar terms, a benefit of $2,000 at FRA shrinks to just $1,400 at 62. Real-world SSA data from December 2025 shows the same story: new claimants who started benefits at 62 received an average of $1,335 per month, while new claimants who waited until 67 received an average of $2,521.

Delayed retirement credits reward patience on the other end of the spectrum. Waiting beyond FRA adds 2/3 of 1% per month, equal to 8% per year. Someone with an FRA of 67 who holds off until age 70 would collect a benefit 24% higher than their full amount. A 2022 National Bureau of Economic Research study found that more than 90% of workers between ages 45 and 62 would maximize their lifetime Social Security income by waiting until 70 to claim. Yet early-claiming applications rose noticeably in 2025, partly driven by uncertainty about the program’s long-term finances.

The stakes are even higher for married couples. An early claim does not just shrink your own check; it also reduces the survivor benefit your spouse could collect if you were the higher earner. By claiming early, you could leave your partner with less guaranteed income for decades.

The broader context makes Orman’s warning more urgent. Social Security’s 2026 cost-of-living adjustment came in at 2.8%, adding roughly $56 to the average retiree’s monthly check and pushing the average monthly benefit to about $2,071. At the same time, Medicare Part B premiums rose to $202.90 per month for 2026, an increase of $17.90 from the prior year. Because those premiums are deducted directly from most retirees’ Social Security checks, the net raise many people actually see is considerably smaller than the headline COLA figure. Claiming at 62 locks in a permanently reduced base, and that smaller base is then subject to the same cost pressures year after year.

The program’s long-term finances add a layer of urgency. The Social Security Board of Trustees, in its June 2026 annual report, projects that the combined Old-Age, Survivors, and Disability Insurance trust funds will be depleted by 2034, at which point ongoing payroll tax revenue would cover about 83% of scheduled benefits unless Congress acts. Looked at separately, the retirement-focused OASI trust fund is now projected to run short even sooner, in late 2032, partly because provisions in recent federal tax legislation are expected to reduce trust fund income going forward. None of this means benefits would disappear, but it reinforces why maximizing the benefit you have earned matters so much.

Many retirees today outlive the life expectancies that shaped Social Security’s original design. The early-filing penalties and delayed retirement credits were intended to even out lifetime benefits for early and late claimants. Because so many people now live well into their 80s and beyond, waiting until 70 typically results in collecting far more in total over a lifetime. The break-even point, the age at which a late claimer’s cumulative benefits surpass what an early claimer collected, typically falls around age 82. That is well within reach for a healthy retiree today.

Taking Orman’s warning seriously and holding off until 70 can be one of the most consequential financial decisions you make. A larger, guaranteed monthly check later in life, when other income sources may have dwindled, provides a cushion that no other retirement asset can fully replicate.

Editor’s note: The trust fund depletion section was updated to reflect the Social Security Board of Trustees’ June 2026 annual report, which projects the combined OASDI funds will run short by 2034 with 83% of benefits payable, while the OASI-only retirement fund is now projected to deplete in late 2032, one quarter earlier than the prior year’s estimate.

Contact [email protected] for any questions or corrections.