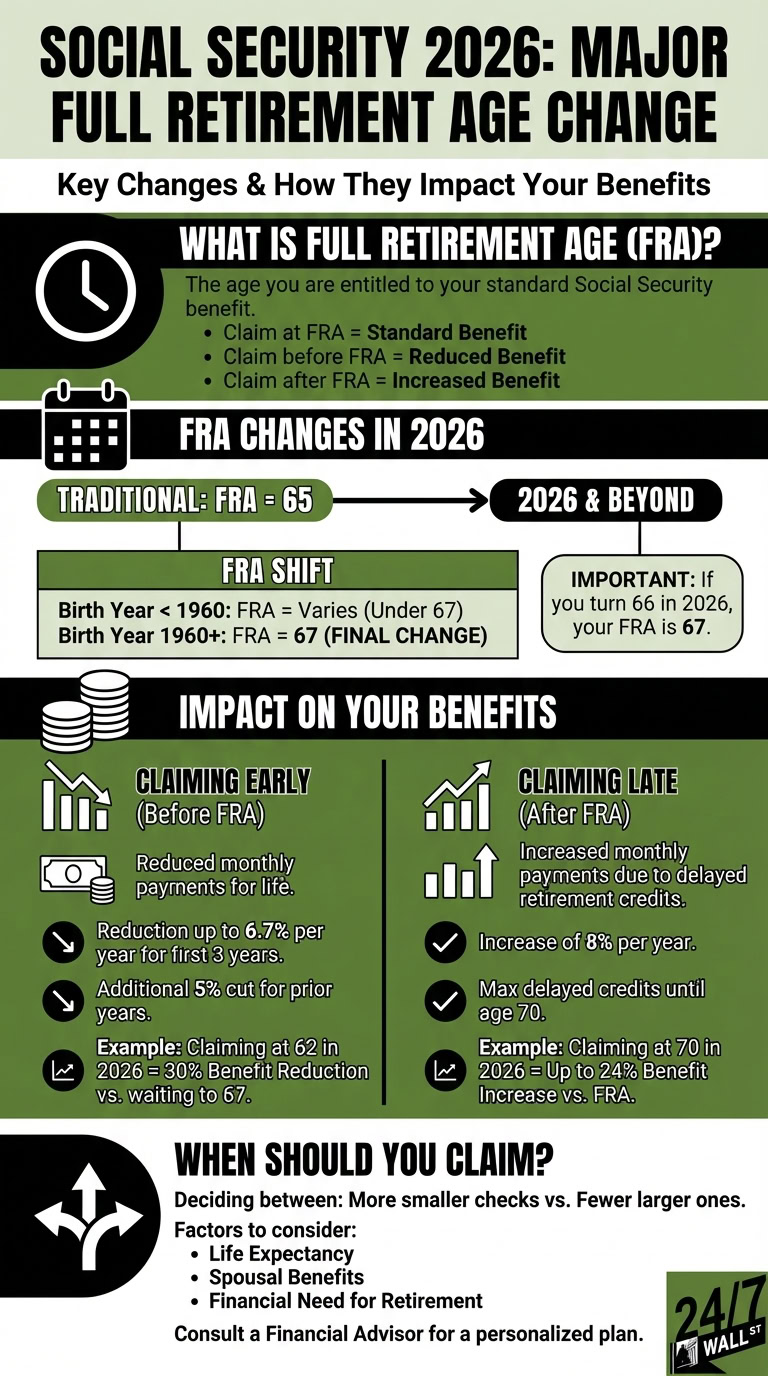

Big changes are coming to Social Security in 2026, and for anyone nearing retirement, one stands out above the rest: full retirement age is shifting for the final time under current law. If you turn 66 this year, your birth year is 1960, which means your full retirement age (FRA) is 67, not 66. That two-year gap determines when you can collect your standard benefit and permanently shapes how much money arrives in your account every month for the rest of your life.

The mechanics of FRA matter because claiming even a single month early locks in a permanent benefit reduction, while waiting even one month past FRA adds to your check through delayed retirement credits. Here is what the 2026 change means in practice and how it should weigh on your claiming decision.

Full retirement age reaches 67 in 2026

Full retirement age is the precise point at which you qualify for your standard Social Security benefit, also called your primary insurance amount. Claim at exactly that age and you receive 100% of what you have earned. Claim a month earlier and you accept a permanent reduction. Wait a month longer and your benefit grows.

For decades, FRA was 65 for every worker. In 1983, with the trust fund facing mounting financial pressure, Congress passed bipartisan reforms that gradually raised FRA over more than 40 years. That phase-in is now complete. Anyone born in 1960 or later has an FRA of 67, the final scheduled step under current law. If you had not yet reached FRA by the end of 2025, you are in this new cohort and will wait longer to collect your full monthly check than workers who retired even a few years before you.

Those 1983 reforms bought the program decades of solvency, but they did not permanently close Social Security’s structural deficit, and the outlook has continued to worsen. The 2026 Social Security Trustees Report, released June 9, 2026, projects that the Old-Age and Survivors Insurance (OASI) trust fund will be depleted in the fourth quarter of 2032, one quarter earlier than the prior year’s estimate. Once reserves run out, incoming payroll tax revenue would cover only about 78% of scheduled benefits, triggering an automatic across-the-board cut. The accelerated timeline reflects three main factors: a revised fertility rate assumption (down from 1.90 to 1.75 children per woman), lower projected immigration that shrinks anticipated payroll tax revenue, and the One Big Beautiful Bill Act enacted in 2025, which reduced income taxation of Social Security benefits and thereby cut a key revenue stream to the trust fund. The program’s 75-year actuarial deficit widened to 4.42% of taxable payroll, up from 3.82% in last year’s report, and the ratio of workers supporting each beneficiary has already fallen from more than 5-to-1 in 1960 to roughly 2.9-to-1 today. Some legislative proposals in response to this shortfall suggest raising FRA further in the future, potentially to 69 or even 70, though no such change is currently law.

Should you claim Social Security at your full retirement age?

The decision of when to start benefits comes down to a fundamental trade-off: more smaller checks or fewer larger ones. You can claim as early as 62, but doing so locks in a permanent reduction for life. The formula is precise: benefits are reduced by 5/9 of 1% for each of the first 36 months before FRA, then by 5/12 of 1% for every additional month. For someone with an FRA of 67 who claims at 62, the full five-year gap produces a 30% reduction, applied to every check you receive for the rest of your life.

To put real 2026 numbers behind that math: after the 2.8% cost-of-living adjustment, the maximum monthly benefit for a worker retiring at exactly 62 is $2,969. Wait until your FRA of 67 and that maximum rises to $4,207 per month. Delay all the way to 70 and it climbs to $5,181. These figures assume maximum taxable earnings (capped at $184,500 in 2026) across 35 years, so most workers will see lower amounts, but the proportional gaps hold regardless of your earnings history.

If you claim early at 62 and keep working, the earnings test applies. In 2026, you can earn up to $24,480 before Social Security withholds anything. Beyond that threshold, the SSA holds back $1 in benefits for every $2 earned. Critically, only wages and net self-employment income count against the limit; pensions, investment income, rental income, and retirement account distributions are excluded entirely. In the year you reach FRA, the limit rises to $65,160, and the withholding rate drops to $1 for every $3 over the threshold, applied only to earnings in months before your birthday. Once you hit FRA, the earnings test disappears and there is no cap on what you can earn. Amounts withheld before FRA are not permanently lost either. At FRA, Social Security recalculates your benefit upward to credit you for the months that were withheld.

The earnings test has drawn renewed attention in Congress. A bipartisan push has emerged to eliminate the provision altogether. Senator Rick Scott introduced the Senior Citizens’ Freedom to Work Act in March 2026, with a House companion bill following in April. Supporters argue that the rule discourages older workers from staying in the workforce at precisely the moment when their payroll tax contributions are most needed to shore up the trust fund’s finances.

Delaying past FRA runs in the other direction. Delayed retirement credits add 2/3 of 1% for each month you wait beyond your FRA, totaling 8% per year. With an FRA of 67, waiting until 70 produces a benefit that is 24% higher than your standard amount. Credits stop accruing at 70, so there is no financial gain from delaying further.

One detail that catches many people off guard: Social Security and Medicare run on separate timetables. Medicare eligibility begins at 65 regardless of your Social Security FRA. Waiting until 67 to enroll in Medicare simply because you plan to defer your Social Security claim can trigger costly lifetime enrollment penalties. Enroll in Medicare at 65 even if you intend to delay your retirement benefit.

The right claiming age turns on your health, expected longevity, household spousal and survivor benefit considerations, and whether you need the income to fund day-to-day expenses in retirement. A financial advisor can model these variables and help you build a claiming strategy that fits your specific situation.

Editor’s note: This version adds the worker-to-beneficiary ratio decline (to 2.9-to-1 today, per the Bipartisan Policy Center’s analysis of the 2026 Trustees Report), the revised fertility-rate assumption (from 1.90 to 1.75 children per woman) driving the accelerated OASI depletion timeline, the 2026 taxable wage base of $184,500, the clarification that only wages and self-employment income count against the earnings test (not pensions or investment income), and context on the bipartisan Senior Citizens’ Freedom to Work Act introduced in Congress in 2026 to eliminate the earnings test.

Contact [email protected] for any questions or corrections.