When it comes to claiming Social Security, opinions vary widely. Suze Orman, a well-known personal finance expert, shared her perspective on LinkedIn recently, and her warning is direct: one common claiming decision could cost retirees significantly for the rest of their lives.

Orman cautioned that a specific Social Security timing choice leads to what she calls a “costly cut.” In 2026, that warning carries extra weight. Retirees received a 2.8% Cost of Living Adjustment (COLA) this year, but much of that gain is being absorbed by a $17.90 monthly increase in Medicare Part B premiums, which now stand at $202.90 per month.

Here is what Orman had to say about the Social Security claiming decision that can carry a steep, permanent price tag.

Orman warned against making this Social Security move

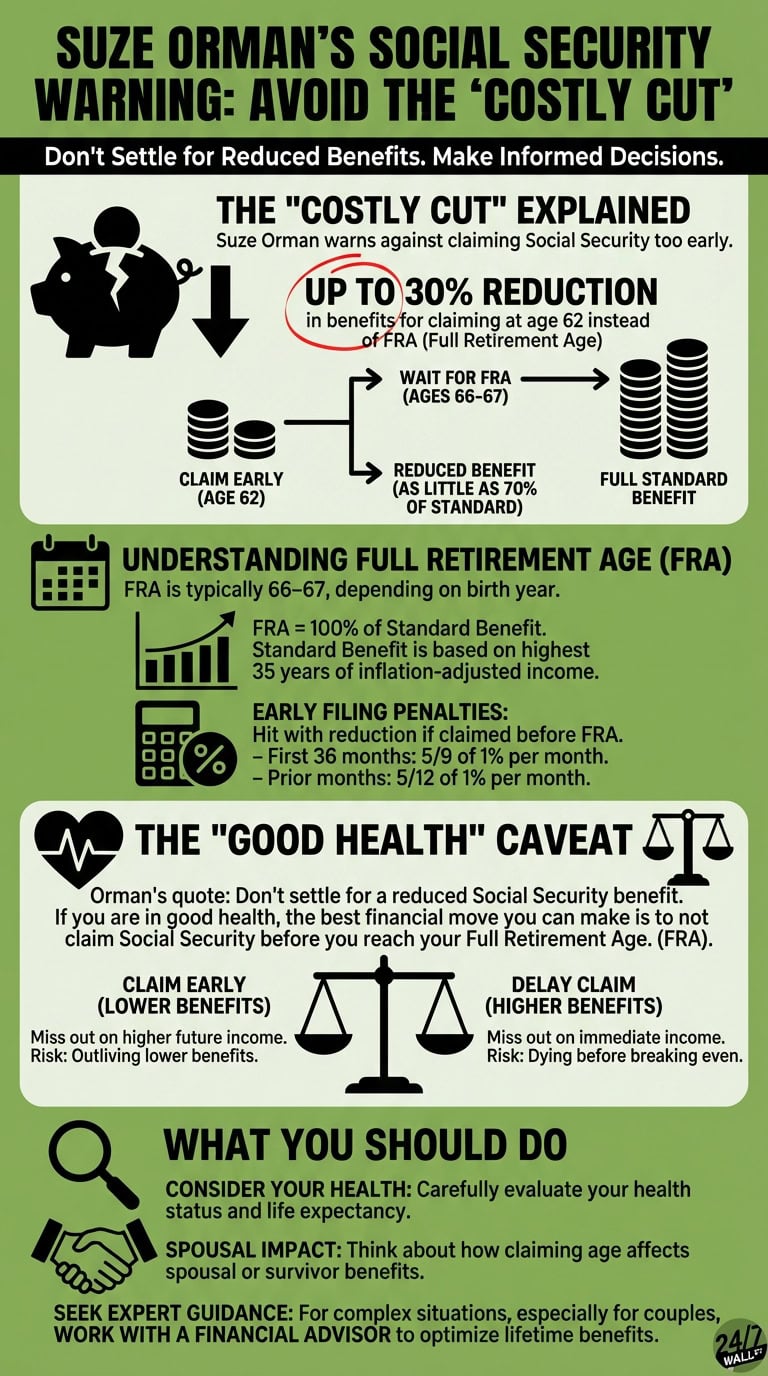

Orman’s concern centers on claiming Social Security too early. Benefits become available as young as 62, but Orman argues that claiming at that age is a costly mistake for most people.

As she explained, full retirement age (FRA) falls between 66 and 67 for most people, depending on the year they were born. Collecting at FRA means receiving 100% of the standard benefit. As of mid-2026, the average monthly Social Security retirement benefit sits at approximately $2,083, according to the SSA’s monthly statistical snapshot.

Despite that average, many retirees claim as soon as they turn 62, well before FRA. Early filing triggers permanent benefit reductions. Workers who also continue earning income while collecting early face an additional wrinkle: in 2026, the SSA withholds $1 from benefits for every $2 earned above the $24,480 annual earnings limit. Both penalties compound, and Orman’s math is correct: a worker who claims at 62 with an FRA of 67 absorbs a 30% permanent cut to their monthly check. That reduction does not go away over time.

Does this mean you should never claim early?

Orman acknowledged that claiming early is not always wrong. On her LinkedIn post, she wrote: “Don’t settle for a reduced Social Security benefit. If you are in good health, the best financial move you can make is to not claim Social Security before you reach your Full Retirement Age. (FRA).”

The “in good health” qualifier matters. Someone with a serious illness or limited life expectancy may break even or come out ahead by claiming early, since the higher lifetime volume of smaller checks can sometimes surpass the benefit of waiting. That calculus shifts further when spousal benefits and survivor income enter the picture.

Two major 2026 developments add new texture to Orman’s advice. First, the One Big Beautiful Bill Act, signed into law in July 2025, created a temporary $6,000 deduction for taxpayers age 65 and older, available through tax year 2028. The deduction phases out above $75,000 in modified adjusted gross income for single filers and $150,000 for joint filers. For retirees in the middle-income range, it can reduce the federal tax owed on Social Security benefits, which slightly improves the after-tax math of waiting. Second, if the 2027 COLA meets the Senior Citizens League’s current projection of 3.8%, waiting until FRA to claim means applying that increase to a larger base amount, producing a meaningfully bigger annual gain.

The program’s long-term finances are also worth keeping in mind. The 2026 Social Security Trustees Report, released in June 2026, projects that the OASI Trust Fund will be depleted in the fourth quarter of 2032, at which point about 78% of scheduled benefits could still be paid from ongoing tax revenue. The One Big Beautiful Bill’s tax provisions are expected to accelerate the depletion timeline, according to the SSA’s chief actuary. Congressional action before that date remains the most likely path to preserving full benefits.

The bottom line is that the right claiming age depends on health, household income, spousal circumstances, and the evolving tax landscape. For most people in good health, Orman’s core point holds: waiting until FRA locks in a substantially higher monthly check for life. Working with a financial advisor to model the specific numbers remains the most reliable way to make the decision.

Editor’s note: This article was updated to reflect the current average Social Security retirement benefit of approximately $2,083 per month as of mid-2026, the $17.90 monthly increase in Medicare Part B premiums to $202.90, the 2026 Trustees Report projection of OASI Trust Fund depletion in Q4 2032, the new $6,000 senior deduction created by the One Big Beautiful Bill Act (signed July 2025), and the Senior Citizens League’s 3.8% COLA projection for 2027.

Contact [email protected] for any questions or corrections.