A spousal IRA is a powerhouse move that lets a working partner fund a retirement account for a spouse with little or no earned income, effectively doubling the household’s annual contribution from a single paycheck. While this strategy has been around for decades, it is often overlooked because most retirement discussions focus solely on the individual. Kiplinger’s May 2026 guidance highlights this as a critical win for couples filing jointly who want to maximize their tax-advantaged savings.

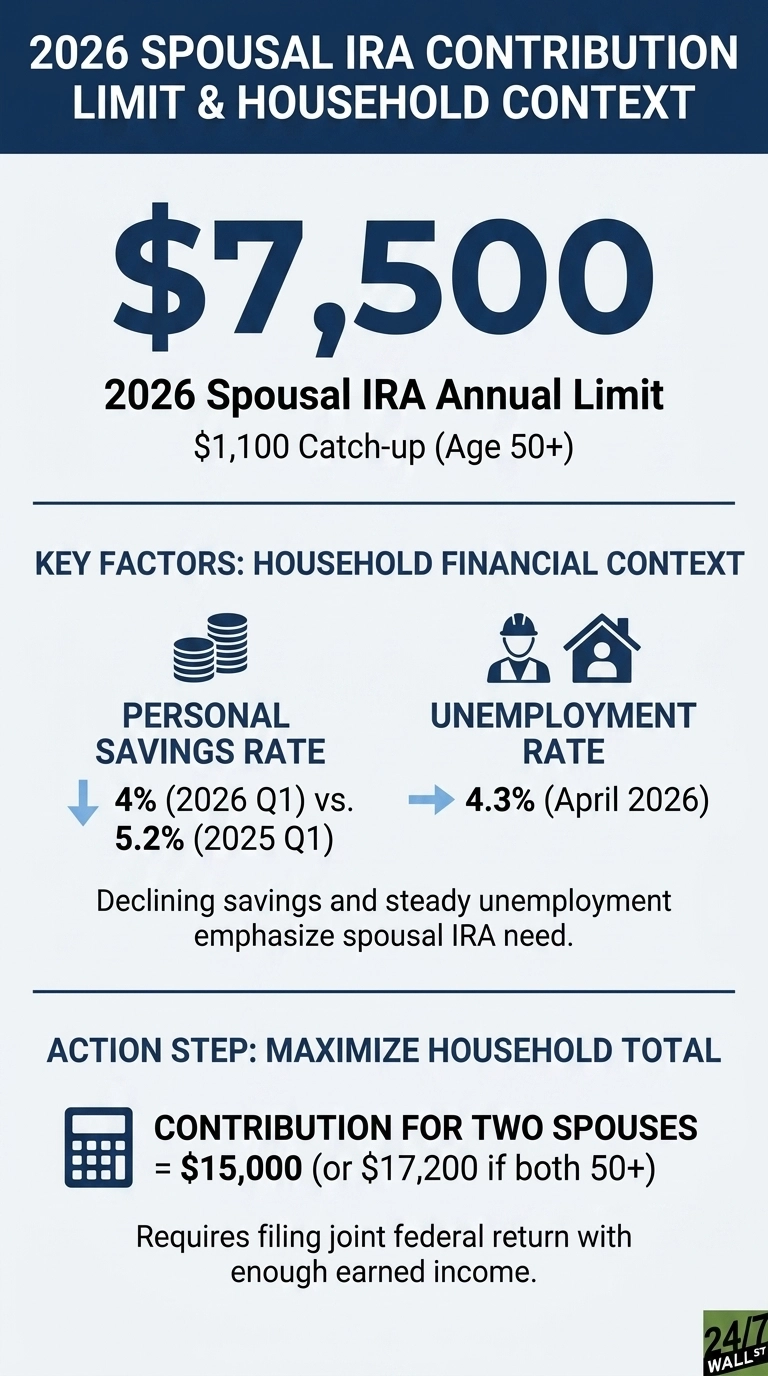

The mechanics are straightforward but effective. As long as you file a joint return and at least one of you has taxable compensation, both of you can hit the full annual limit in your own traditional or Roth accounts. For 2026, that limit sits at $7,500 per person, plus a $1,100 catch-up for those 50 and older. This means a couple can stash away $15,000 total, or a massive $17,200 if both are over 50. To make it happen, the household just needs enough earned income to cover the combined contributions.

Why the Higher Limit Matters in 2026

The jump in contribution limits comes just as household savings are feeling the heat. While per capita disposable income climbed to $68,617, the personal savings rate took a hit, sliding to 4% in the first quarter of 2026 from 5.2% just a year prior. Consumption is currently devouring a massive slice of the income pie, leaving families with a razor-thin margin to fund their retirement goals.

The economic pressure is real, as the Consumer Price Index hit 332.4 in April, a steady climb from 320.62 in May 2025, serving as a loud reminder of how quickly purchasing power vanishes when cash sits on the sidelines. Consumer sentiment is equally grim, with the University of Michigan index hitting 48.2 in May, deep in pessimistic territory and nowhere near the neutral 80 mark.

Even with the Federal Funds Rate at 3.75%, households are struggling to prioritize savings. While those lower short-term rates might take the edge off cash yields within an IRA, they generally provide the fuel that supports equity and bond valuations, which most spousal IRAs rely on for long-term growth. The challenge for 2026 is finding the discipline to capture that growth while the cost of living keeps pushing back.

How Couples Actually Double the Contribution

The qualifying conditions are narrow and worth stating plainly:

- The couple must file a joint federal return for the year of the contribution.

- The earning spouse must have taxable compensation, defined as wages, salary, tips, or self-employment income, at least equal to the combined IRA contributions.

- The non-working spouse owns the spousal IRA outright. The account is in that spouse’s name, not jointly held.

A household earning a single $80,000 salary, for example, can move $15,000 into two separate IRAs in 2026, one for each spouse. If both are 50 or older, that figure rises to $17,200. With unemployment steady at 4.3% as of April, the underlying premise of the strategy, one steady earner and one spouse out of the labor force, applies to a meaningful share of married households.

Traditional Versus Roth Choice

The spousal IRA can be either traditional or Roth, and the choice carries different tax mechanics. Traditional contributions may be deductible depending on whether the working spouse is covered by a workplace plan and on the couple’s modified adjusted gross income. Roth contributions phase out for joint filers with MAGI between $242,000 and $252,000 in 2026. Above that ceiling, the Roth route closes, though non-deductible traditional contributions remain available regardless of income.

One practical wrinkle: contributions for tax year 2026 can be made up to the April 2027 filing deadline, which lets couples wait for final W-2 figures before deciding how much to allocate and whether to use a Roth or traditional account. Asset protection is a secondary consideration. Holding retirement assets in both names can shield a portion of household savings in scenarios involving long-term care spend-down rules, which vary by state.

Single-Income Households and the Spousal IRA

For couples operating on one paycheck, the spousal IRA is among the provisions in the tax code that allow a non-earning partner to participate in retirement savings. The $7,500 limit for 2026, paired with the $1,100 catch-up, raises the ceiling on what a single income can shelter. Eligibility is broad, so adoption tends to hinge on whether households are aware of the option.

Contact [email protected] for any questions or corrections.