Kiplinger’s May 2026 Tax Letter highlights a shift in retirement plan policy that has been building since last summer. After decades of being walled off, the 401(k) is on track to allow private equity, private credit, real estate, infrastructure, and digital asset funds inside employer plans. The change does not affect every saver this year, but it reshapes what a workplace retirement account can hold for the long term.

How the Door Opened

The shift traces back to Executive Order 14330, “Democratizing Access to Alternative Assets for 401(k) Investors,” signed in August 2025. The order directed the Department of Labor and the SEC to clear regulatory and litigation barriers that had kept alternatives from appearing in plan lineups. Five days later, the DOL rescinded earlier guidance warning fiduciaries against investing in private equity in defined contribution plans.

On March 30, 2026, the DOL issued a proposed safe harbor rule for fiduciaries selecting alternatives. The comment period closes June 1, 2026, with a final rule possible by year-end and implementation more likely in 2027. The legal backdrop matters: ERISA requires fiduciaries to act prudently rather than banning specific asset classes. Agency guidance, litigation fear, and the difficulty of valuing illiquid holdings are what kept them out, and those are the pieces the DOL can address without Congress.

What “Alternatives” Actually Means

For the typical saver, this shift opens the door to four major asset classes that were previously locked away. Private equity buys into companies off the public ticker, while private credit acts as the lender to those same firms. Real estate funds manage everything from commercial towers to apartment portfolios, and infrastructure funds scoop up “backbone” assets like data centers, energy pipelines, and toll roads.

Historically, these plays were reserved for the elite who could clear the SEC’s accredited investor hurdle, which generally requires a $1 million net worth or $200,000 in annual income, or the even higher qualified purchaser bar of $5 million in investments. But the landscape is shifting. A recent executive order has directed federal agencies to strip away the red tape and litigation risks that kept these options out of reach for the average worker.

By expanding 401(k) options to include private equity and real estate, the bar is effectively being lowered for anyone with a workplace plan. The Labor Department is now giving plan fiduciaries maximum flexibility to weave these alternative assets into standard retirement portfolios.

The Saver This Actually Reaches

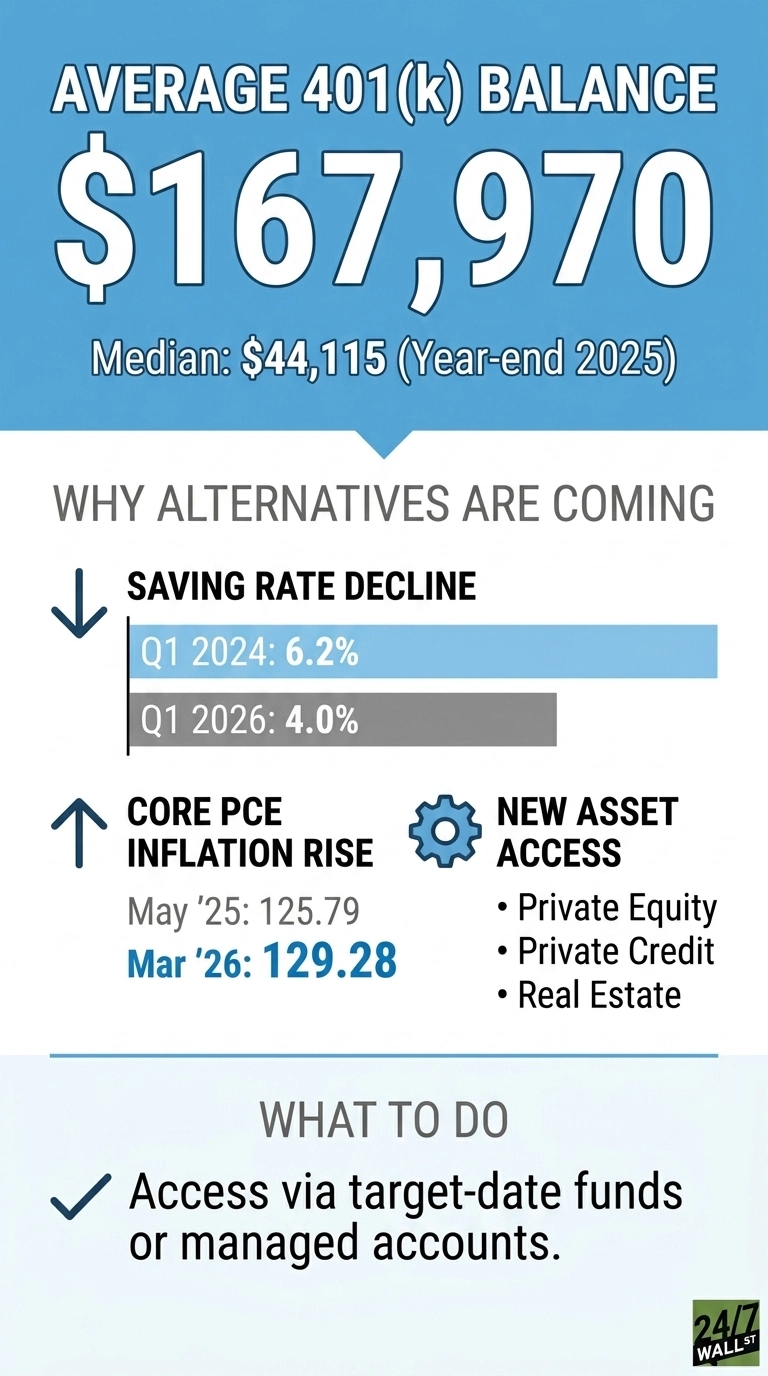

The data shows a massive divide between the average and the typical worker. While 401(k) accounts make up roughly $8.7 trillion of the $13.8 trillion held in U.S. retirement plans, the individual numbers tell two different stories. At year-end 2025, the average participant account balance stood at $167,970, but the median balance was a much lower $44,115. This gap is the classic retirement narrative: a small group of high-balance savers pulls up the average, while the typical worker operates with much less.

That divide becomes critical when discussing the shift toward alternative assets. A 1% allocation to private equity or real estate looks manageable on a $167,970 balance, but on a $44,115 balance, the math changes. For smaller accounts, the trade-offs like higher fees and long-term “lock-ups” where you can’t touch your cash hit much harder. Even as the Labor Department gives plan fiduciaries maximum discretion to add these complex assets to boost returns, the smaller the balance, the heavier the risk of getting caught in a liquidity squeeze.

The Macro Backdrop

The data show a clear squeeze on American households. While per capita disposable income climbed to $68,617, the personal saving rate plummeted to 4.0% in Q1 2026, down from 5.2% just one year prior. Even though paychecks are growing, the money is flying out the door as fast as it comes in. This financial stress is showing up in the country’s mood, with the University of Michigan consumer sentiment index hitting a pessimistic 48.2 in May 2026. That is deep in the trenches, especially considering anything near 60 is usually viewed as recessionary territory.

The yield environment is what makes this moment so interesting for investors. The 10-year Treasury is rising as the war in Iran hikes inflation expectations, while the federal funds rate remains steady at 3.75%. At the same time, the Federal Reserve’s preferred inflation gauge, Core PCE, has been on a steady upward grind, rising from 125.79 in May 2025 to 129.28 in March 2026. This combination of factors means bonds are finally offering a real yield again, but with inflation threatening to hit 4% by year-end, those yields are barely keeping pace with the rising cost of living. Diversification is no longer a suggestion; it is a survival strategy.

What It Means Inside a Plan

The mechanics of this shift matter far more than the marketing hype. Alternative funds typically carry higher expense ratios than index funds, often layered with performance fees that can eat into long-term gains. Many of these assets come with lock-up periods or gated redemptions, which sit awkwardly with the daily valuation 401(k) plans usually rely on. Because of these complexities, plan sponsors will likely introduce alternatives through target-date funds or managed accounts rather than as standalone options. The goal is to cap exposure at a single-digit percentage of a participant’s balance, relying on a prudent selection process rather than any guarantee of returns.

For a worker comparing policy to their own balance sheet, the data shows exactly what is changing without sugarcoating the risks. It does not predict which alternatives will actually perform, how high the fees will climb, or how the first market downturn will test the valuation rules for these less-liquid assets. This category is officially moving from prohibited to permitted, but the fine print will be written over the next several years as the Labor Department and plan fiduciaries exercise their new flexibility.

Contact [email protected] for any questions or corrections.