A new federal incentive is about to change retirement savings for millions of lower and middle-income Americans. On April 30, 2026, President Trump signed an executive order directing the Treasury to launch TrumpIRA.gov by January 1, 2027, a federally administered platform that points workers to low-cost private-sector IRAs. Paired with the Federal Saver’s Match from SECURE 2.0, eligible savers who contribute to one of these accounts will receive a $1,000 government match deposited directly by the Treasury. For the roughly half of American workers without a 401(k), this is the most concrete federal savings incentive in a generation.

The Match Is the Headline

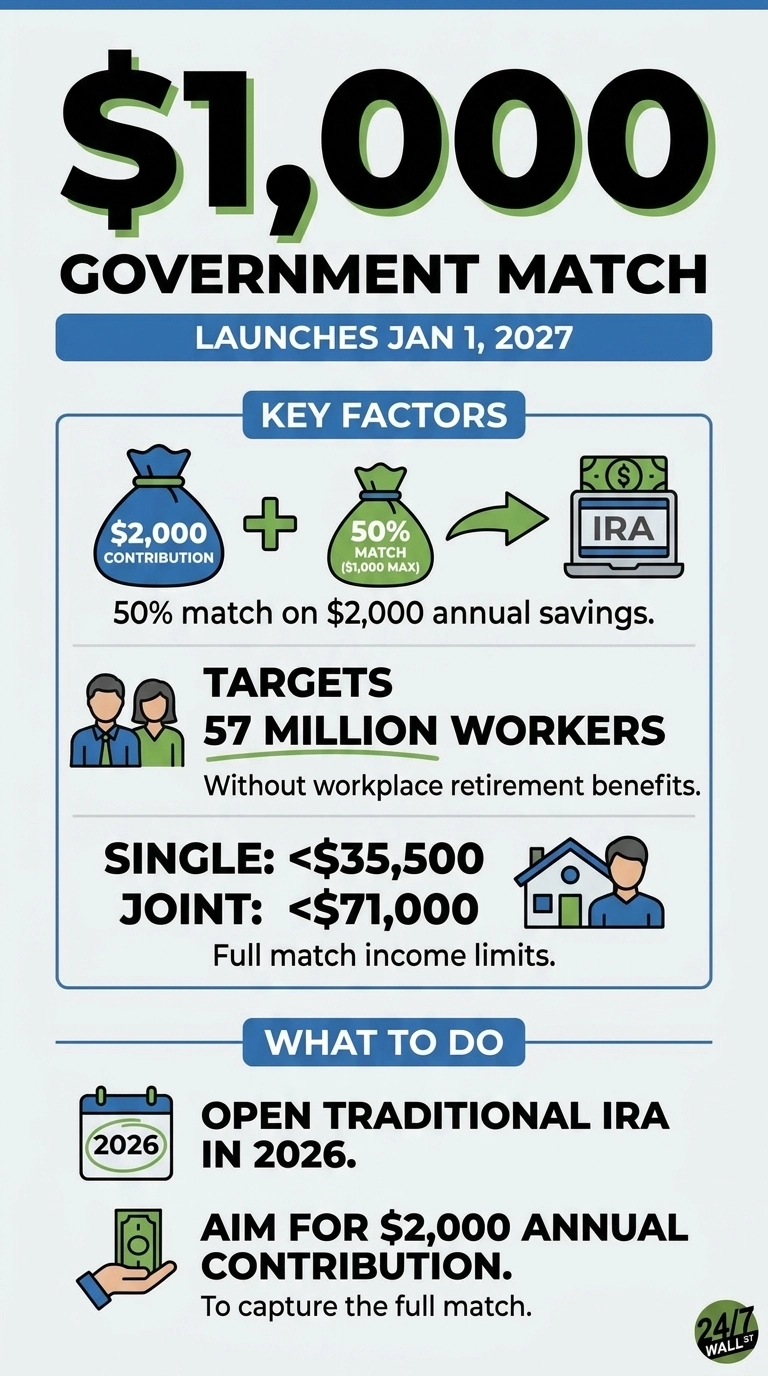

The mechanics are straightforward: the Saver’s Match pays a 50% match on up to $2,000 in annual IRA contributions, capped at $1,000 per eligible saver per year. Treasury deposits the money directly into the saver’s IRA, where it compounds for decades.

To qualify for the full match, a single filer must earn less than $35,500 in modified adjusted gross income, with the cap at $71,000 for joint filers. Phase-outs reduce the match above those thresholds. Contributions must go into a traditional IRA (or qualifying workplace plan), and the saver must be at least 18, not a full-time student, and not claimed as a dependent.

An employer 401(k) match has long been the easiest free money in personal finance, and roughly half the workforce has never had access to one. The Saver’s Match is the federal government stepping in to play the absent-employer role for lower-income workers.

Who Qualifies

The executive order targets independent contractors, part-time workers, the self-employed, and people at small businesses without retirement plans. A Pew Charitable Trusts analysis found that nearly 57 million American workers, almost half the private sector workforce, do not receive retirement benefits at their workplace. The Bureau of Labor Statistics reported that about 74% of U.S. workers had access to a workplace retirement plan in March 2025, with only 56% actually participating.

That participation gap is the policy target. Auto IRA programs in 17 states have shown that workers will save when enrollment is easy, but those programs lack an employer match. The federal match fills the gap in the incentive.

How the New Account Works

TrumpIRA.gov operates as a routing platform layered on top of the existing IRA framework. Rather than holding funds directly, the executive order defines it as a federally administered informational platform designed to highlight high-quality, low-cost options in the private sector. It functions as a vetted directory that directs savers toward traditional and Roth accounts managed by private custodians. The administration’s goal is to give users access to the same caliber of low-fee, index-style choices that federal employees enjoy through the Thrift Savings Plan. Once the account is set up, the matching Treasury deposit is triggered automatically after the tax return is filed and eligibility is confirmed.

Why Acting Now Beats Waiting

For an eligible saver, the practical sequence is straightforward:

- Open a traditional IRA in 2026. A self-employed or part-time worker can establish an account today with any major custodian. While the federal Saver’s Match officially applies to contributions made for the 2027 tax year and beyond, building the foundational account now eliminates operational friction later.

- Aim for $2,000 in annual contributions to capture the maximum match. Putting in anything less leaves free government money on the table. By contributing $2,000 and securing the $1,000 match, a saver locks in an effective 50% first-year return before any market growth or compounding interest even takes effect.

- Check income thresholds annually, as the match gradually phases out up to a hard ceiling of $35,500 for singles and $71,000 for joint filers, meaning a raise, a new side gig, or a shift in a spouse’s earnings can alter eligibility from one year to the next.

- For perspective, the average IRA balance across all age groups at the end of 2025 climbed to $137,100, according to Fidelity’s analysis of 18.9 million accounts. A worker who maxes out the Saver’s Match for a decade secures $10,000 in pure government funding before factoring in their own personal savings or investment gains. That falls short of a full nest egg, but for someone starting from zero without a workplace plan, it is the difference between a real portfolio and no portfolio at all.

The program targets a specific segment of the retirement coverage gap, giving workers left out of the 401(k) system a federal match worth pursuing. The first contributions eligible for the match will be made in 2027, but the accounts to receive them can be opened today.

Contact [email protected] for any questions or corrections.