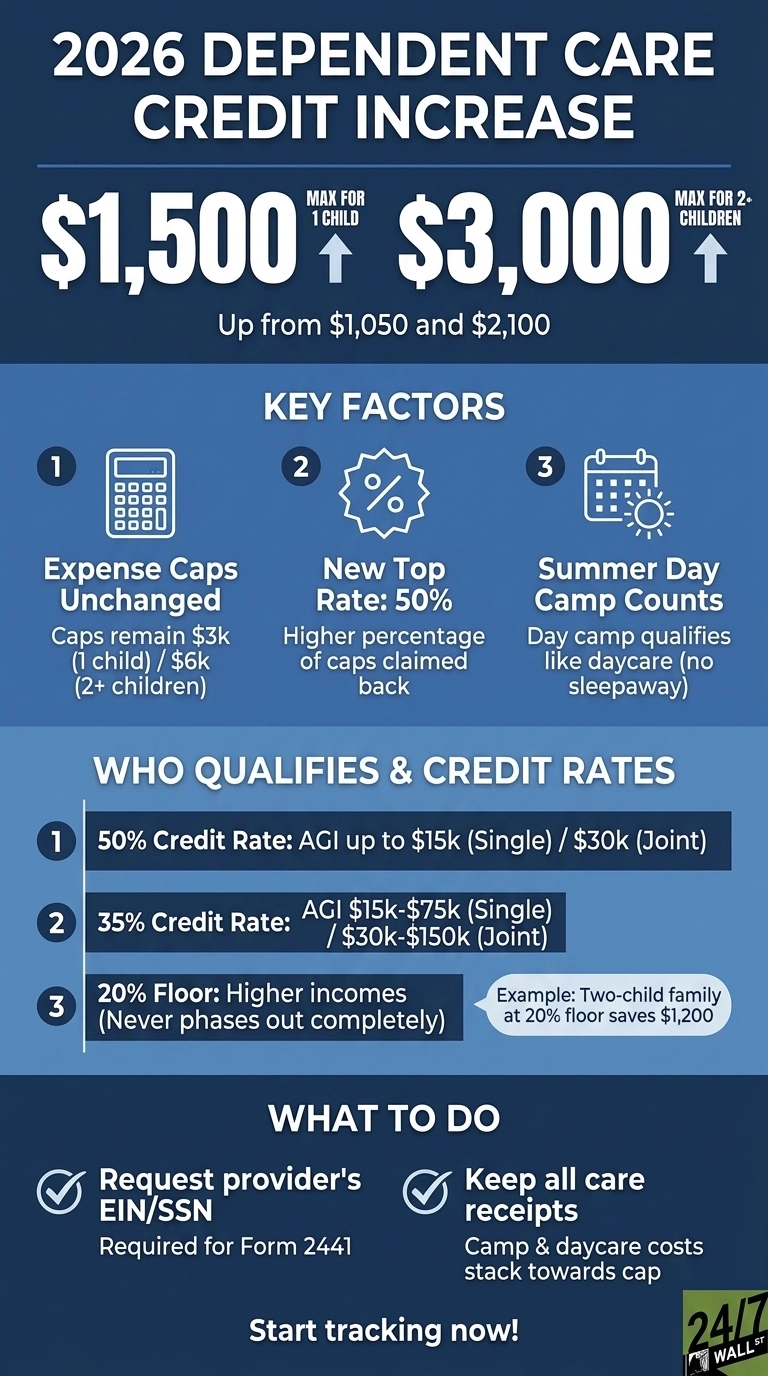

Working parents are getting a major tax upgrade as the federal Child and Dependent Care Credit climbs for 2026. The maximum payout has jumped to $1,500 for a single child and to $3,000 for two or more, providing a welcome bump from the old caps. Leaving this cash on the table is easy if you don’t know the mechanics, making it vital to spot common IRS trapdoors before filing.

Where the bigger numbers come from

The expense caps remain unchanged at $3,000 for eligible care costs for one child and $6,000 for two or more children. What shifted is the percentage of expenses you can claim back. Under the One Big Beautiful Bill Act, the top credit rate rises to 50% beginning in tax year 2026. Apply 50% to the existing caps, and you get the new maximums of $1,500 and $3,000.

Who qualifies

The top rate of the credit applies strictly to lower-income earners. The credit steps down as income rises, but it never fully phases out. The 2026 structure:

- Credit ranges from a high of 50% down to a floor of 20% for higher incomes

- The 2025 credit was worth 20% to 35% of eligible care expenses

A household earning well into six figures keeps a 20% credit on up to $6,000 of care expenses, worth $1,200 off the federal tax bill for a two-child family. Both spouses on a joint return must have earned income, care must enable work or job searching, and the child must be under 13 (or a spouse or dependent physically or mentally unable to care for themselves).

What expenses count

The IRS covers care that enables you to work, while kindergarten tuition does not count, but licensed daycare centers, in-home nannies and babysitters, before-school and after-school programs, and care by a relative (not your spouse or dependent) do. In addition, payroll taxes on household employees count too, so this is another consideration.

Summer day camp: the overlooked option

Parents most often forget summer day camp, as the IRS treats a day camp like daycare if it covers care during working hours and the child is under 13. Sports camps, art camps, coding camps, and the local YMCA all qualify. Traditionally, specialty programs need not be educational, but there is at least one exception. As it stands today, overnight camp is excluded, and sleepaway camps do not qualify.

This gets missed because parents think about the credit in February, long after camp invoices are filed away. A family paying $400 weekly for an eight-week summer day camp easily clears the $3,000 expense cap for one child by Labor Day. At the 35% rate most middle-income filers hit, that yields $1,050 back. At the new top rate, it is the full $1,500.

How to capture it

Three moves separate parents who claim the credit from those who miss it:

- Request every provider’s Employer Identification Number or Social Security number at the time of payment. Without that ID on Form 2441, the credit is disallowed.

- Keep a single folder for all care receipts across the year. Daycare, after-school, and camp expenses add up to the same $3,000 or $6,000 cap.

- Coordinate with a dependent care FSA if your employer offers one. Money through the FSA cannot also be claimed for the credit, but the FSA contribution limit rose to $7,500 under OBBBA, so higher earners often benefit by using the FSA first and the credit on remaining expenses.

The credit applies only to parents who track spending and file the form. Summer day camp is the easiest place to start.

Contact [email protected] for any questions or corrections.