Generating $3,500 per month in retirement income works out to roughly $42,000 annually, enough to cover the payment on a typical middle-to-upper-range U.S. home in today’s market. At current interest rates, a $3,500 monthly housing payment could support roughly a $475,000 to $550,000 home purchase using a 30-year fixed mortgage with 20% down, depending on local property taxes and insurance costs.

For retirees, though, the challenge is not simply producing the income. It is producing it on a schedule that matches real life. Mortgage payments, utility bills, insurance premiums, and grocery expenses arrive every month, not every quarter. Traditional dividend portfolios often distribute income unevenly throughout the year, forcing retirees to manage their own cash-flow timing. Monthly dividend investments simplify that process by aligning portfolio income more closely with how bills actually arrive.

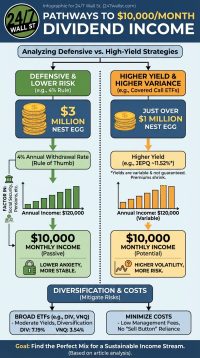

Three Ways to Get There

The capital required to produce $42,000 depends entirely on the blended yield. The math is unforgiving and worth seeing at three tiers:

- Conservative tier near 3.5%: $42,000 divided by 0.035 equals $1,200,000 in capital. This is broad-market dividend-growth territory, where principal usually appreciates and the income stream tends to rise with inflation.

- Moderate tier near 6%: $42,000 divided by 0.06 equals $700,000. High-yield equity, preferred shares, and traditional REITs live here. Dividend growth slows and upside is capped relative to the index.

- Aggressive tier near 10%: $42,000 divided by 0.10 equals $420,000. Covered-call ETFs, BDCs, and mortgage REITs occupy this band. Distributions are high today, but principal erosion is a real risk and many strategies cap participation in bull markets.

A Five-Fund Monthly Portfolio Around $600,000

Blending the moderate and aggressive tiers to a roughly 7% average yield puts the capital requirement near $600,000. One way to assemble it from five monthly payers, each running a distinct strategy:

- JPMorgan Equity Premium Income ETF (NYSEARCA:JEPI): A $150,000 position targets about $12,000 a year from a covered-call overlay on S&P 500 names. The expense ratio is 0.35%.

- JPMorgan Nasdaq Equity Premium Income ETF (NASDAQ:JEPQ): A $100,000 sleeve generates roughly $9,500 a year. JEPQ writes calls on Nasdaq-100 constituents, with top holdings including NVIDIA at 7.9% and Apple at 6.4% of net assets.

- NEOS S&P 500 High Income ETF (NYSEARCA:SPYI): A $100,000 position targets about $11,000 through an options-overlay structure designed for tax-efficient monthly distributions on the S&P 500.

- Realty Income (NYSE:O | O Price Prediction): A $75,000 stake in this net-lease REIT pays roughly $4,200 a year at a 5.6% yield. The latest monthly declaration came in at about $0.27 per share, continuing a 16-year record of uninterrupted monthly payments.

- STAG Industrial (NYSE:STAG): A $125,000 allocation in this industrial REIT yields about 4.5%, contributing roughly $5,600 a year and adding warehouse and logistics exposure that the equity ETFs do not provide.

That mix lands close to the $42,000 target while diversifying across S&P covered calls, Nasdaq covered calls, an enhanced S&P income strategy, a net-lease REIT, and an industrial REIT.

The Tax Reality Behind These Distributions

Covered-call ETF distributions are mostly taxed as ordinary income rather than qualified dividends. REIT distributions are likewise ordinary income, though the Section 199A pass-through deduction historically allowed retirees to deduct 20% of qualified REIT dividends. Verify the current treatment with a CPA, because legislative changes under the One Big Beautiful Bill reshaped several deduction rules effective 2026. For a single retiree in the 22% bracket (taxable income above $50,400), holding these funds in an IRA rather than a taxable account is the single largest after-tax lever available.

Where CBOE Fits the Picture

Cboe Global Markets (CBOE) pays quarterly rather than monthly, placing it outside the portfolio’s direct income sleeve. Its connection to the strategy is more structural than distributive: many covered-call ETFs generate income by selling options on indices such as the S&P 500 and Nasdaq-100, markets that Cboe operates and monetizes through trading activity and derivatives infrastructure.

The stock itself functions more as a growth-and-quality counterweight within a broader income portfolio. While its dividend yield remains relatively modest at around 0.8%, the company has recently delivered strong operational momentum, including sharply higher earnings growth and substantial share-price appreciation over the past year. In effect, Cboe represents the “toll road” underlying part of the options-income ecosystem, benefiting from the growing popularity of covered-call and derivatives-based income strategies without relying on ultra-high distributions itself.

Investor’s To Do List:

- Calculate your actual monthly expenses rather than anchoring to your former salary. Many retirees discover their replacement target is well under $3,500 once payroll taxes, retirement contributions, and commuting are gone.

- Compare the 10-year total return of a 3.5% dividend-growth fund against a 10% covered-call ETF. Lower current yield with growing distributions frequently outperforms a high static yield over a 20-year retirement.

- Rebalance the five sleeves once a year. Covered-call funds and REITs drift at different speeds, and letting one strategy dominate the portfolio defeats the diversification the five-fund structure is built to provide.